Advertisement

- Hong Kong

- /

- Capital Markets

- /

- SEHK:1469

How Does Get Nice Financial Group's (HKG:1469) CEO Salary Compare to Peers?

Carmen Hung has been the CEO of Get Nice Financial Group Limited (HKG:1469) since 2015, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

See our latest analysis for Get Nice Financial Group

How Does Total Compensation For Carmen Hung Compare With Other Companies In The Industry?

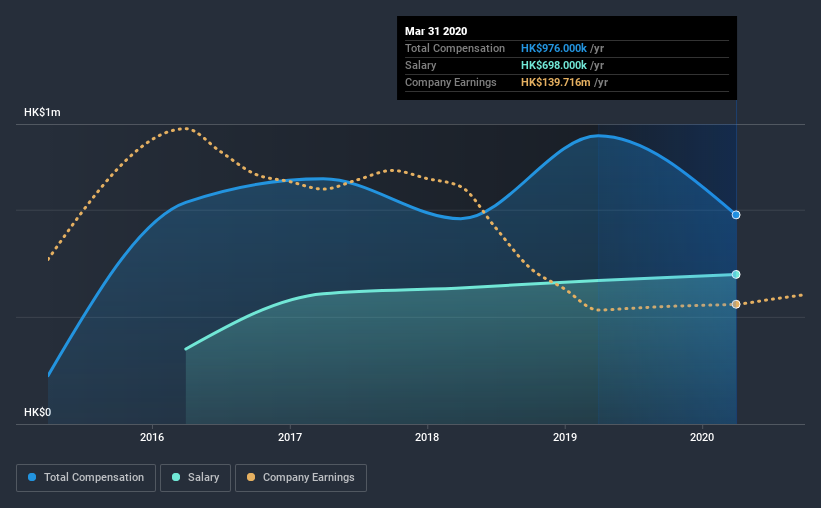

At the time of writing, our data shows that Get Nice Financial Group Limited has a market capitalization of HK$2.3b, and reported total annual CEO compensation of HK$976k for the year to March 2020. We note that's a decrease of 27% compared to last year. Notably, the salary which is HK$698.0k, represents most of the total compensation being paid.

On examining similar-sized companies in the industry with market capitalizations between HK$775m and HK$3.1b, we discovered that the median CEO total compensation of that group was HK$1.9m. In other words, Get Nice Financial Group pays its CEO lower than the industry median.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | HK$698k | HK$670k | 72% |

| Other | HK$278k | HK$675k | 28% |

| Total Compensation | HK$976k | HK$1.3m | 100% |

Talking in terms of the industry, salary represented approximately 86% of total compensation out of all the companies we analyzed, while other remuneration made up 14% of the pie. Get Nice Financial Group pays a modest slice of remuneration through salary, as compared to the broader industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Get Nice Financial Group Limited's Growth Numbers

Over the last three years, Get Nice Financial Group Limited has shrunk its earnings per share by 20% per year. It achieved revenue growth of 16% over the last year.

The reduction in EPS, over three years, is arguably concerning. But in contrast the revenue growth is strong, suggesting future potential for EPS growth. It's hard to reach a conclusion about business performance right now. This may be one to watch. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Get Nice Financial Group Limited Been A Good Investment?

Given the total shareholder loss of 38% over three years, many shareholders in Get Nice Financial Group Limited are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

As we noted earlier, Get Nice Financial Group pays its CEO lower than the norm for similar-sized companies belonging to the same industry. But shareholder returns and EPS growth over the past three years are negative, which is cause for concern. In contrast, revenues have increased more recently. Though we believe Carmen is modestly compensated, shareholders might want to see positive shareholder returns before agreeing compensation should be raised.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We identified 4 warning signs for Get Nice Financial Group (1 is a bit unpleasant!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you decide to trade Get Nice Financial Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1469

Get Nice Financial Group

An investment holding company, provides financial services in Hong Kong.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

92 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative