Advertisement

- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:2517

Evaluating Guoquan Food (SEHK:2517): Is the Current Valuation Justified After Rapid Q3 Expansion and Profit Growth?

Simply Wall St

Reviewed by Simply Wall St

Guoquan Food (Shanghai) SEHK:2517 expanded its retail network by 98% in Q3 2025, adding more than 360 new instant retail stores. This surge aligns with marked gains in year-on-year revenue and core operating profit.

See our latest analysis for Guoquan Food (Shanghai).

After Guoquan Food’s rapid rollout of new stores and jump in core profit, momentum is clearly building as its share price climbed nearly 20% over the past month with a year-to-date share price return of 106%. In total, shareholders saw a 1-year total return of 51%, suggesting the recent operational strides are catching the market’s attention.

If Guoquan’s expansion has you thinking bigger, now’s the perfect time to broaden your search and discover fast growing stocks with high insider ownership

With Guoquan’s impressive expansion and surging profitability, the big question remains: does the current share price represent untapped upside, or have markets fully anticipated the company’s future growth?

Price-to-Earnings of 28.4x: Is it justified?

Guoquan Food (Shanghai) currently trades at a price-to-earnings ratio of 28.4x, noticeably higher than its industry and peer averages. With the last close at HK$3.85, investors are paying a premium for today’s earnings relative to other consumer retailing companies in Asia.

The price-to-earnings (P/E) ratio measures how much investors are willing to pay for each dollar of net profit. In fast-growing segments, a higher P/E can signal optimism for future profits. However, it may also indicate over-enthusiasm or limited upside if expectations prove too optimistic. For Guoquan, strong historical earnings growth supports some premium, but it is important to consider whether the current level is justified as the company matures.

Compared to the Asian consumer retailing industry average P/E of 16.3x, Guoquan’s shares look much more expensive. It also far exceeds the peer average of 19.2x and even the ‘fair’ P/E ratio estimated at 21.7x. Unless earnings accelerate even more than forecast, the stock’s valuation could revert closer to industry norms.

Explore the SWS fair ratio for Guoquan Food (Shanghai)

Result: Price-to-Earnings of 28.4x (OVERVALUED)

However, risks remain, such as slower than expected revenue growth or earnings disappointments, which could pressure Guoquan's premium valuation and share price trajectory.

Find out about the key risks to this Guoquan Food (Shanghai) narrative.

Another View: What Does the SWS DCF Model Say?

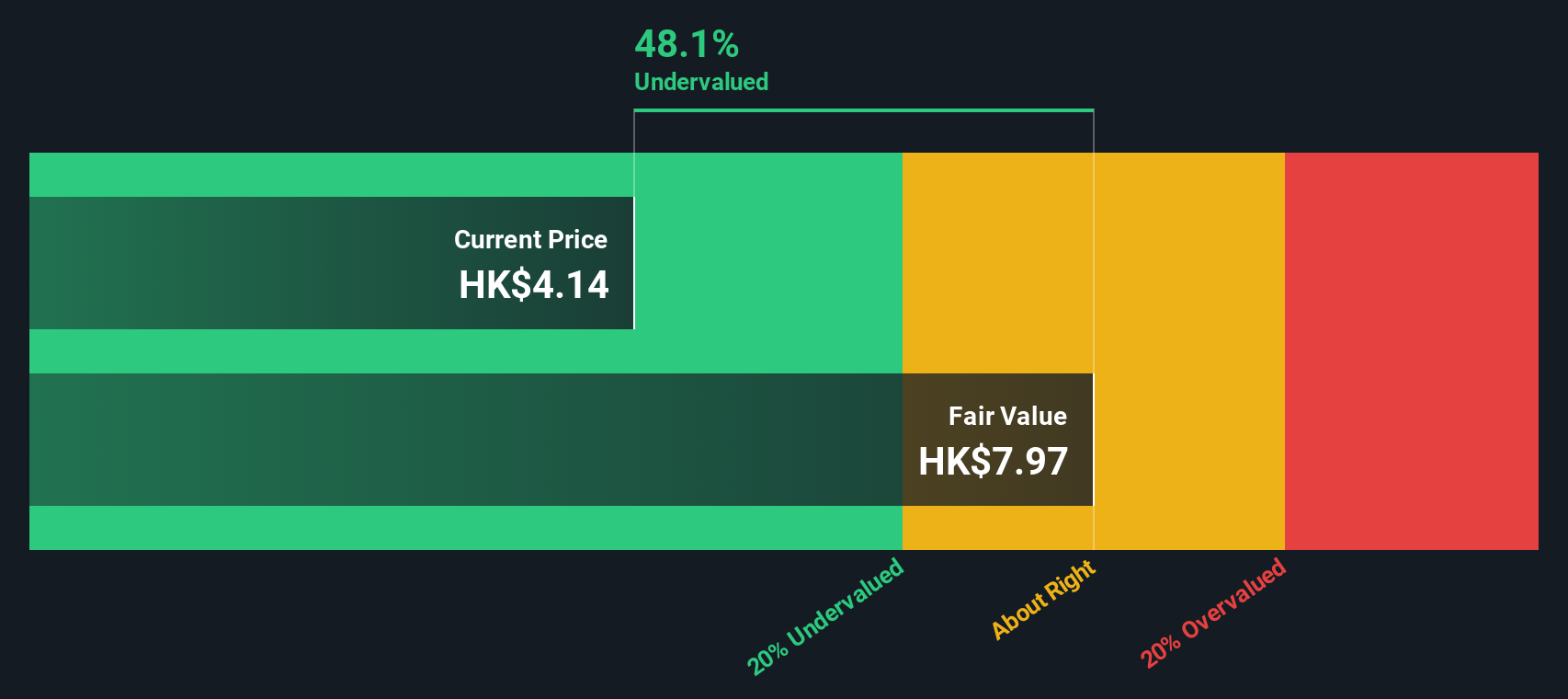

Looking beyond earnings multiples, our DCF model values Guoquan Food's shares at HK$8.02. This figure is more than double the current trading price of HK$3.85. By this method, the stock appears significantly undervalued and presents a different angle compared to price-to-earnings alone. Which view will the market believe?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Guoquan Food (Shanghai) for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 840 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Guoquan Food (Shanghai) Narrative

If you see things differently or want a hands-on approach to research, it's simple to craft your own perspective in just a few minutes. Do it your way

A great starting point for your Guoquan Food (Shanghai) research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment opportunities?

Take the next step and boost your investment portfolio by tapping into some of the market’s most promising sectors and strategies with these handpicked ideas:

- Capture long-term growth waves when you review these 840 undervalued stocks based on cash flows, which is brimming with stocks currently trading below their intrinsic value.

- Target passive income and income stability by checking out these 22 dividend stocks with yields > 3%, featuring companies that yield over 3%.

- Ride the momentum of cutting-edge technology by browsing these 27 AI penny stocks, where you'll find businesses redefining the future with artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2517

Guoquan Food (Shanghai)

Operates as a home meal products company in Mainland China.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$26.69|18.6% undervalued

BE

Community Contributor