- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:156

Even after rising 11% this past week, Lippo China Resources (HKG:156) shareholders are still down 45% over the past five years

This week we saw the Lippo China Resources Limited (HKG:156) share price climb by 11%. But over the last half decade, the stock has not performed well. After all, the share price is down 54% in that time, significantly under-performing the market.

The recent uptick of 11% could be a positive sign of things to come, so let's take a look at historical fundamentals.

Check out our latest analysis for Lippo China Resources

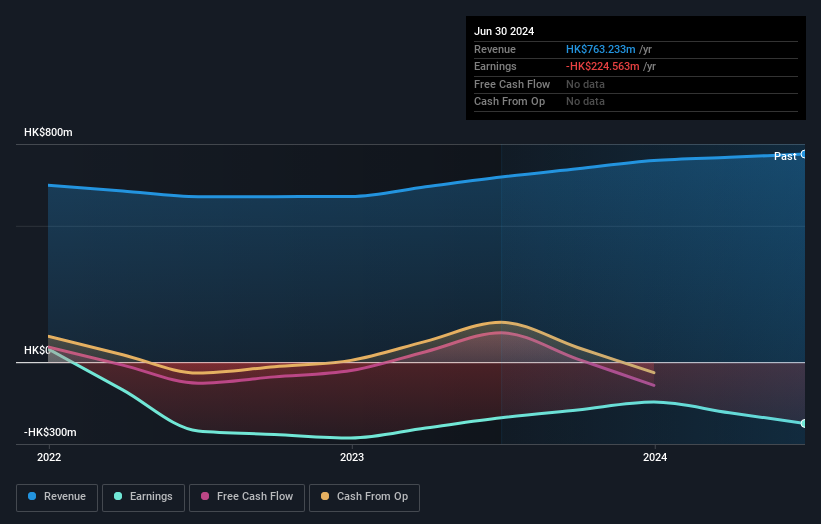

Lippo China Resources isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

In the last five years Lippo China Resources saw its revenue shrink by 18% per year. That puts it in an unattractive cohort, to put it mildly. It seems appropriate, then, that the share price slid about 9% annually during that time. We don't generally like to own companies that lose money and don't grow revenues. You might be better off spending your money on a leisure activity. You'd want to research this company pretty thoroughly before buying, it looks a bit too risky for us.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

Take a more thorough look at Lippo China Resources' financial health with this free report on its balance sheet.

What About The Total Shareholder Return (TSR)?

We'd be remiss not to mention the difference between Lippo China Resources' total shareholder return (TSR) and its share price return. Arguably the TSR is a more complete return calculation because it accounts for the value of dividends (as if they were reinvested), along with the hypothetical value of any discounted capital that have been offered to shareholders. Its history of dividend payouts mean that Lippo China Resources' TSR, which was a 45% drop over the last 5 years, was not as bad as the share price return.

A Different Perspective

Lippo China Resources shareholders are down 5.3% for the year, but the market itself is up 7.3%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. However, the loss over the last year isn't as bad as the 8% per annum loss investors have suffered over the last half decade. We would want clear information suggesting the company will grow, before taking the view that the share price will stabilize. It's always interesting to track share price performance over the longer term. But to understand Lippo China Resources better, we need to consider many other factors. Take risks, for example - Lippo China Resources has 2 warning signs (and 1 which can't be ignored) we think you should know about.

But note: Lippo China Resources may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:156

Lippo China Resources

An investment holding company, engages in food, and property investment and development businesses in Hong Kong, Mainland China, Singapore, Malaysia, and internationally.

Adequate balance sheet very low.