- Hong Kong

- /

- Oil and Gas

- /

- SEHK:1277

Exploring Undiscovered Gems in Hong Kong This October 2024

Reviewed by Simply Wall St

As global markets navigate the complexities of rising oil prices and geopolitical tensions, Hong Kong's stock market has shown resilience, with the Hang Seng Index climbing significantly in recent weeks. This environment presents a unique opportunity to explore lesser-known stocks that may offer potential growth amid broader economic shifts. Identifying promising stocks often involves looking at companies with strong fundamentals and innovative strategies that can thrive even in uncertain times.

Top 10 Undiscovered Gems With Strong Fundamentals In Hong Kong

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Lion Rock Group | 16.91% | 14.33% | 10.15% | ★★★★★★ |

| E-Commodities Holdings | 21.33% | 9.04% | 28.46% | ★★★★★★ |

| C&D Property Management Group | 1.32% | 37.15% | 41.55% | ★★★★★★ |

| ManpowerGroup Greater China | NA | 14.56% | 1.58% | ★★★★★★ |

| COSCO SHIPPING International (Hong Kong) | NA | -3.84% | 16.33% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Xin Point Holdings | 1.77% | 10.88% | 22.83% | ★★★★★☆ |

| Lvji Technology Holdings | 3.06% | 4.56% | -1.87% | ★★★★★☆ |

| Lee's Pharmaceutical Holdings | 14.22% | -1.39% | -14.93% | ★★★★★☆ |

| Pizu Group Holdings | 48.34% | -4.53% | -19.78% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

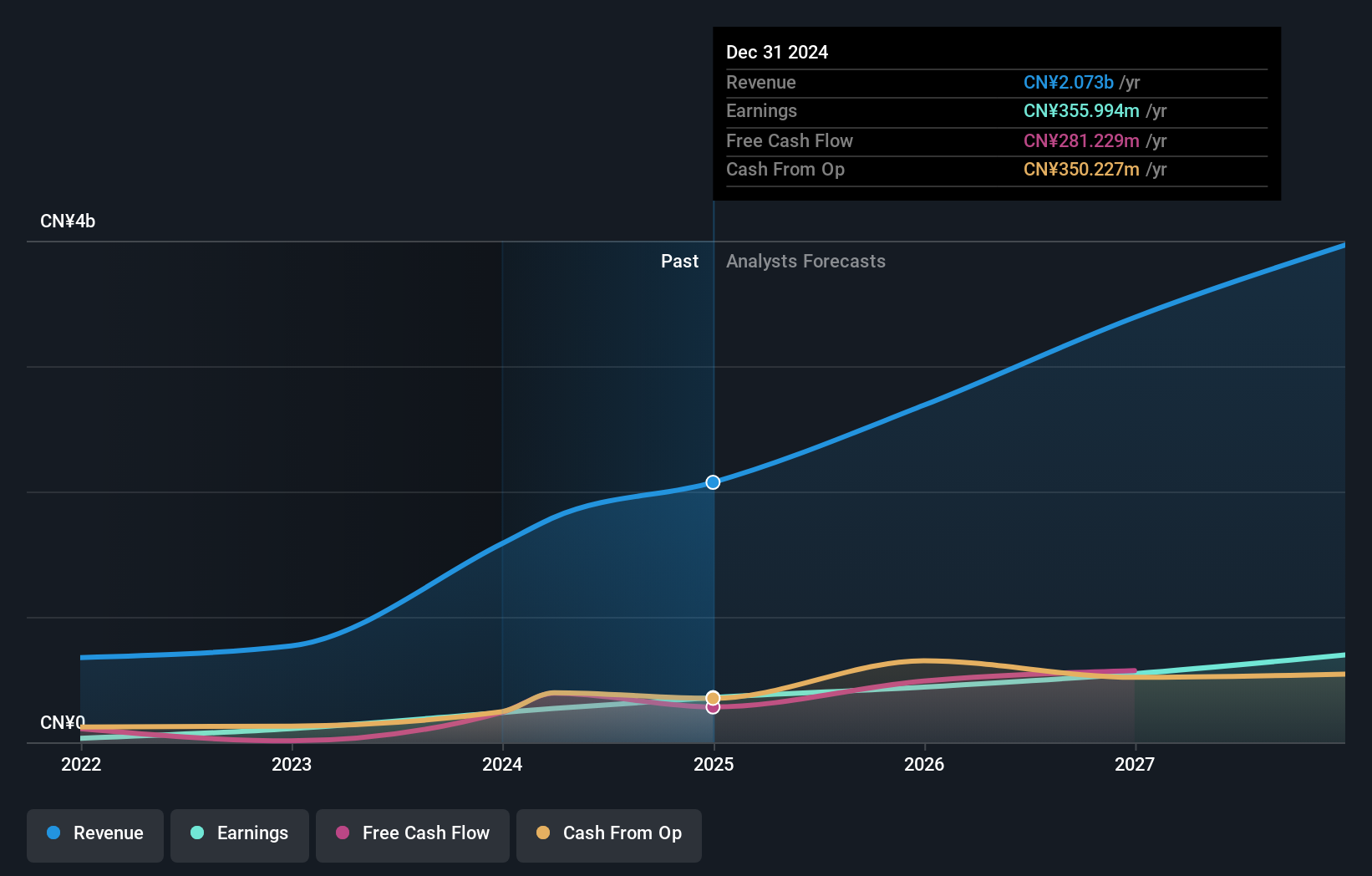

Kinetic Development Group (SEHK:1277)

Simply Wall St Value Rating: ★★★★★☆

Overview: Kinetic Development Group Limited is an investment holding company involved in the extraction and sale of coal products in China, with a market capitalization of HK$14.92 billion.

Operations: Kinetic Development Group generates revenue primarily from the sale of coal products in China. The company's financial performance is highlighted by a net profit margin trend that has shown variability over recent periods.

Kinetic Development Group, with a net debt to equity ratio of 4.7%, presents a satisfactory financial standing. The company's earnings growth of 39% over the past year outpaced the Oil and Gas industry average of 5%, showcasing strong performance. Trading at 54% below its estimated fair value, it offers potential upside for investors. Recent results highlighted sales of CNY 2.53 billion and net income of CNY 1.10 billion, reflecting robust revenue expansion from last year’s figures.

- Delve into the full analysis health report here for a deeper understanding of Kinetic Development Group.

Gain insights into Kinetic Development Group's past trends and performance with our Past report.

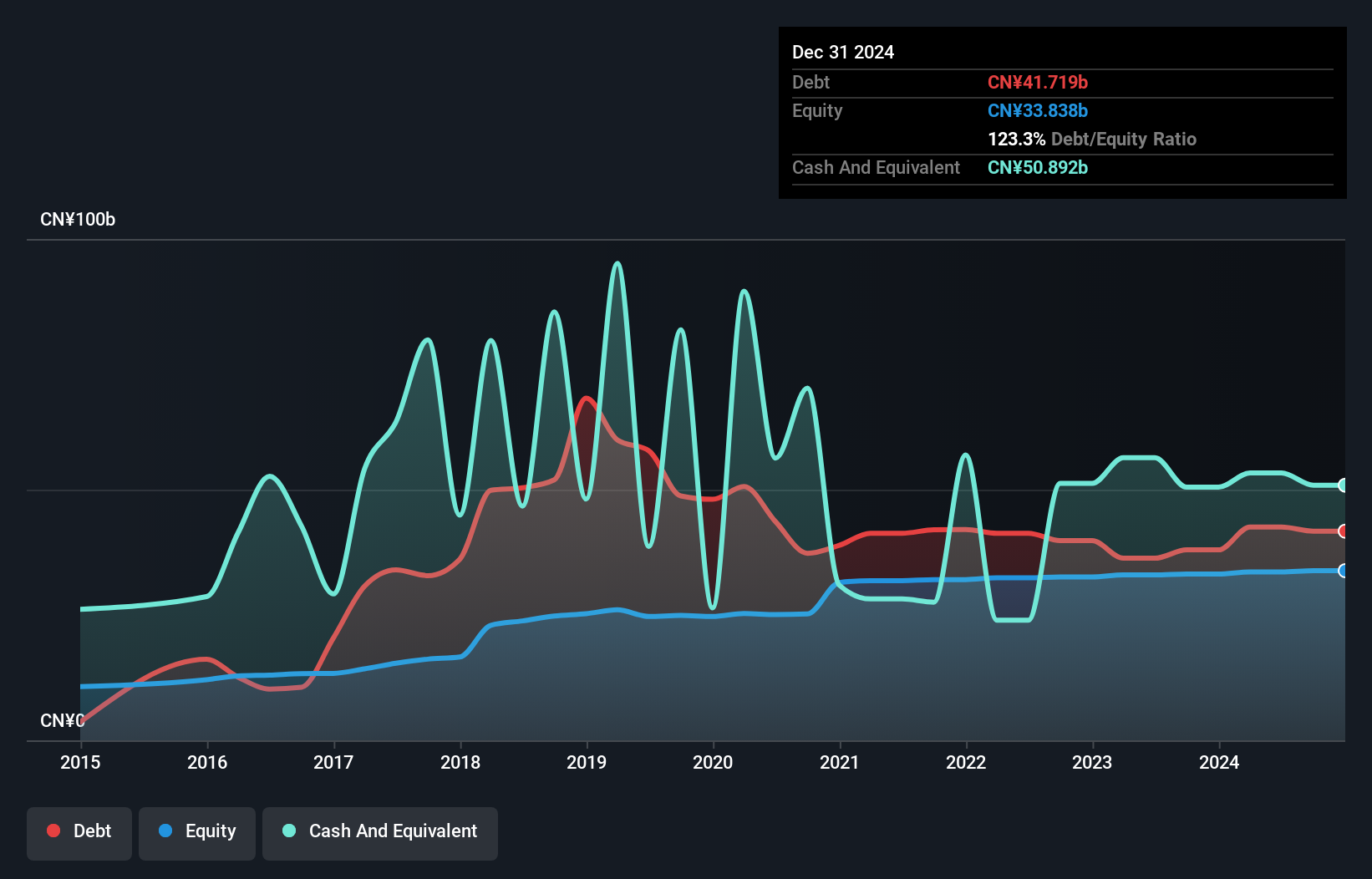

Bank of Gansu (SEHK:2139)

Simply Wall St Value Rating: ★★★★★★

Overview: Bank of Gansu Co., Ltd., operating alongside its subsidiary Pingliang Jingning Chengji Rural Bank Co., Ltd., offers a range of banking services in the People’s Republic of China and has a market capitalization of HK$6.78 billion.

Operations: The primary revenue streams for Bank of Gansu Co., Ltd. include retail banking, generating CN¥2.10 billion, and corporate banking, contributing CN¥1.21 billion. Financial market operations show a negative impact on revenue with a loss of CN¥368.60 million.

With CN¥422.2 billion in total assets, Bank of Gansu stands as a modest player with a focus on stability through its primarily low-risk funding sources, comprising 86% customer deposits. The bank's net interest margin is 1.5%, and it has an adequate allowance for bad loans at 1.9% of total loans, ensuring resilience against defaults. Despite earnings declining by 6.4% annually over five years, its price-to-earnings ratio of 9.7x suggests potential value compared to the broader Hong Kong market average of 10.6x.

- Take a closer look at Bank of Gansu's potential here in our health report.

Evaluate Bank of Gansu's historical performance by accessing our past performance report.

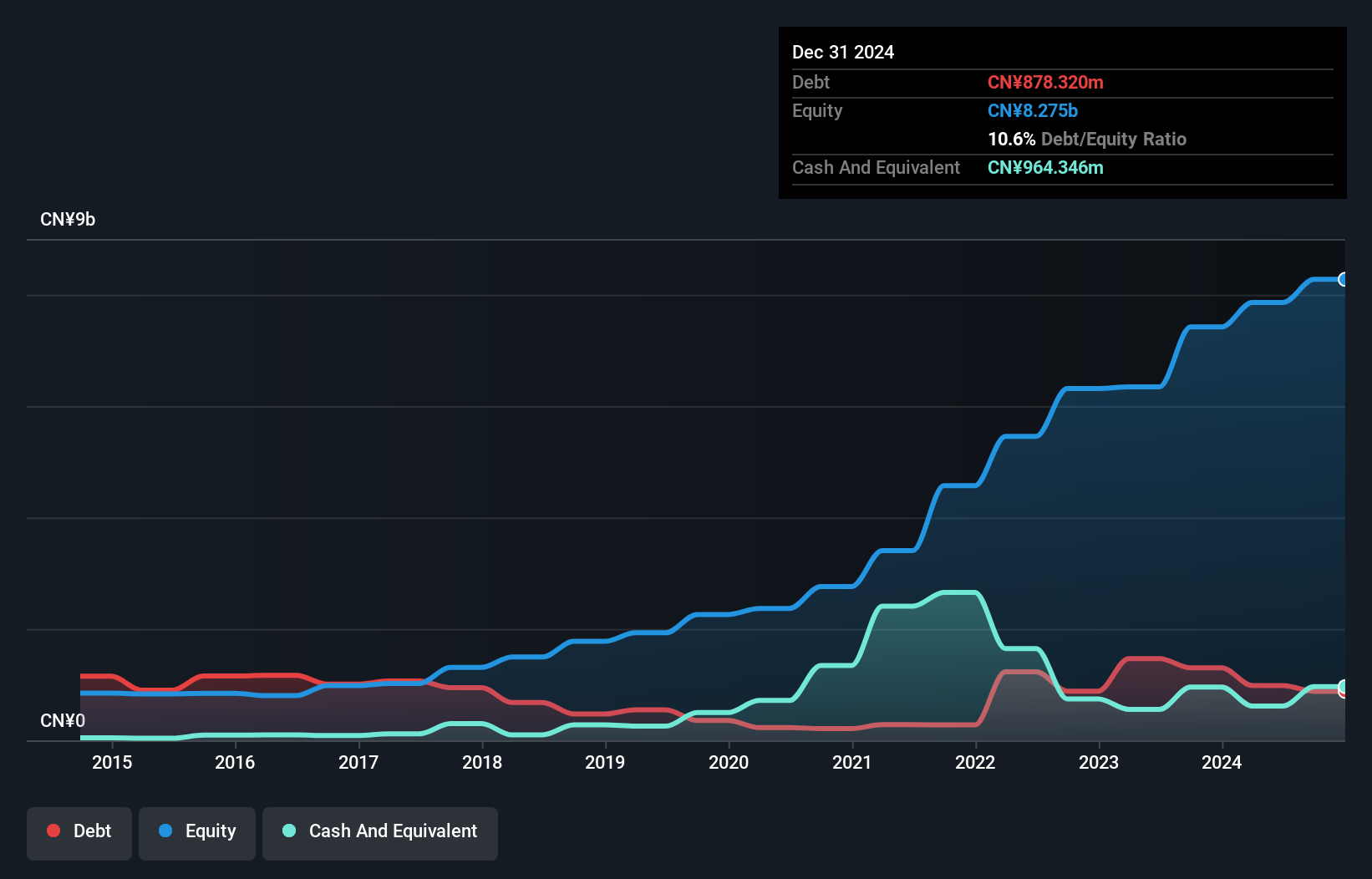

Carote (SEHK:2549)

Simply Wall St Value Rating: ★★★★★☆

Overview: Carote Ltd is an investment holding company that offers a variety of kitchenware products to brand-owners and retailers under the CAROTE brand, with a market cap of HK$3.91 billion.

Operations: Carote Ltd generates revenue primarily from its Branded Business, contributing CN¥1.58 billion, and its ODM Business, which adds CN¥210.80 million. The Branded Business is the dominant segment in terms of revenue contribution.

Carote, a small player in the market, recently completed an IPO, raising HK$750.62 million with shares priced at HK$5.78 each. Over the past year, earnings surged by 92%, outpacing the Consumer Durables industry average of 20%. The company holds more cash than its total debt and trades at nearly 78% below its fair value estimate. Despite high-quality earnings and positive free cash flow, share liquidity remains low.

- Click to explore a detailed breakdown of our findings in Carote's health report.

Understand Carote's track record by examining our Past report.

Key Takeaways

- Unlock our comprehensive list of 173 SEHK Undiscovered Gems With Strong Fundamentals by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kinetic Development Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1277

Kinetic Development Group

An investment holding company, engages in the extraction and sale of coal products in the People’s Republic of China.

Outstanding track record with excellent balance sheet.