- Hong Kong

- /

- Trade Distributors

- /

- SEHK:1231

Newton Resources (HKG:1231) adds HK$200m to market cap in the past 7 days, though investors from five years ago are still down 41%

Newton Resources Ltd (HKG:1231) shareholders should be happy to see the share price up 11% in the last week. But over the last half decade, the stock has not performed well. After all, the share price is down 41% in that time, significantly under-performing the market.

On a more encouraging note the company has added HK$200m to its market cap in just the last 7 days, so let's see if we can determine what's driven the five-year loss for shareholders.

Check out our latest analysis for Newton Resources

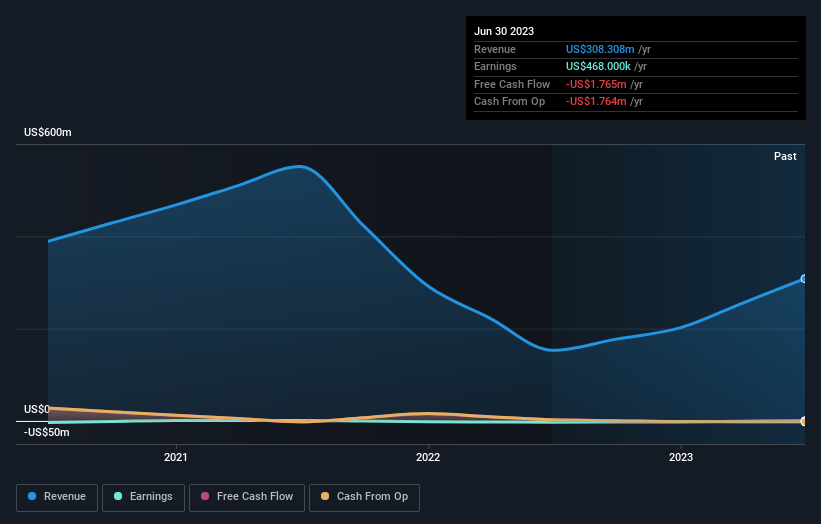

Given that Newton Resources only made minimal earnings in the last twelve months, we'll focus on revenue to gauge its business development. Generally speaking, we'd consider a stock like this alongside loss-making companies, simply because the quantum of the profit is so low. It would be hard to believe in a more profitable future without growing revenues.

In the last half decade, Newton Resources saw its revenue increase by 11% per year. That's a pretty good rate for a long time period. We doubt many shareholders are ok with the fact the share price has fallen 7% each year for half a decade. Those who bought back then clearly believed in stronger growth - and maybe even profits. The lesson is that if you buy shares in a money losing company you could end up losing money.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

Take a more thorough look at Newton Resources' financial health with this free report on its balance sheet.

A Different Perspective

We regret to report that Newton Resources shareholders are down 20% for the year. Unfortunately, that's worse than the broader market decline of 8.8%. Having said that, it's inevitable that some stocks will be oversold in a falling market. The key is to keep your eyes on the fundamental developments. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 7% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. You could get a better understanding of Newton Resources' growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Newton Resources might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1231

Newton Resources

An investment holding company, engages in the sourcing and supply of iron ores and other commodities in Mainland China and internationally.

Excellent balance sheet with questionable track record.