Advertisement

- United Kingdom

- /

- Specialty Stores

- /

- LSE:WIX

Wickes Group (LON:WIX) Is Experiencing Growth In Returns On Capital

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Speaking of which, we noticed some great changes in Wickes Group's (LON:WIX) returns on capital, so let's have a look.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Wickes Group:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

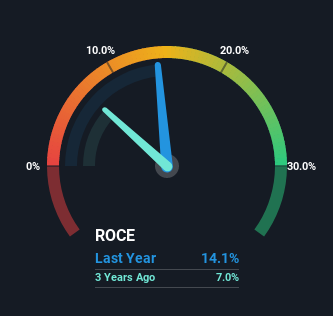

0.14 = UK£116m ÷ (UK£1.2b - UK£334m) (Based on the trailing twelve months to January 2022).

So, Wickes Group has an ROCE of 14%. In absolute terms, that's a pretty normal return, and it's somewhat close to the Specialty Retail industry average of 16%.

View our latest analysis for Wickes Group

Above you can see how the current ROCE for Wickes Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Wickes Group here for free.

How Are Returns Trending?

You'd find it hard not to be impressed with the ROCE trend at Wickes Group. The data shows that returns on capital have increased by 101% over the trailing three years. The company is now earning UK£0.1 per dollar of capital employed. Interestingly, the business may be becoming more efficient because it's applying 24% less capital than it was three years ago. A business that's shrinking its asset base like this isn't usually typical of a soon to be multi-bagger company.

One more thing to note, Wickes Group has decreased current liabilities to 29% of total assets over this period, which effectively reduces the amount of funding from suppliers or short-term creditors. This tells us that Wickes Group has grown its returns without a reliance on increasing their current liabilities, which we're very happy with.

In Conclusion...

In a nutshell, we're pleased to see that Wickes Group has been able to generate higher returns from less capital. And since the stock has fallen 19% over the last year, there might be an opportunity here. That being the case, research into the company's current valuation metrics and future prospects seems fitting.

Wickes Group does have some risks though, and we've spotted 3 warning signs for Wickes Group that you might be interested in.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Wickes Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:WIX

Wickes Group

Operates as a retailer of home improvement products and services in the United Kingdom.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor