- United Kingdom

- /

- Professional Services

- /

- LSE:HAS

3 UK Stocks Estimated To Be Trading Below Intrinsic Value

Reviewed by Simply Wall St

The United Kingdom market has recently faced challenges, with the FTSE 100 index closing lower amid weak trade data from China and a sluggish global economic recovery. Despite these headwinds, investors can still find opportunities in stocks that are estimated to be trading below their intrinsic value. Identifying such undervalued stocks requires careful analysis of their fundamentals, especially in uncertain market conditions like those we are currently experiencing.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| TBC Bank Group (LSE:TBCG) | £30.15 | £57.68 | 47.7% |

| Gaming Realms (AIM:GMR) | £0.4005 | £0.76 | 47.3% |

| Liontrust Asset Management (LSE:LIO) | £6.51 | £12.24 | 46.8% |

| Topps Tiles (LSE:TPT) | £0.47 | £0.9 | 47.6% |

| Marks Electrical Group (AIM:MRK) | £0.645 | £1.27 | 49.2% |

| C&C Group (LSE:CCR) | £1.562 | £2.99 | 47.7% |

| AstraZeneca (LSE:AZN) | £130.76 | £248.35 | 47.3% |

| Mercia Asset Management (AIM:MERC) | £0.35 | £0.67 | 48.1% |

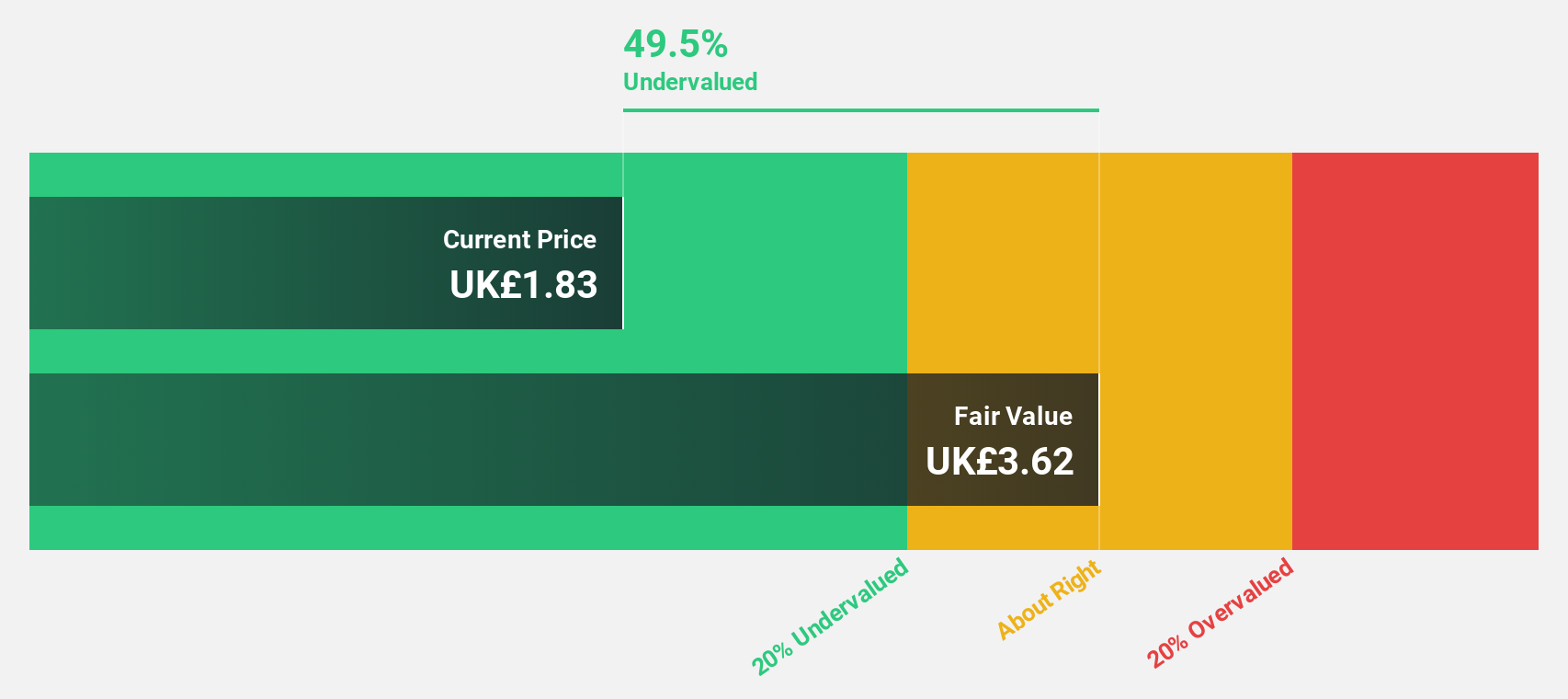

| Franchise Brands (AIM:FRAN) | £1.82 | £3.60 | 49.5% |

| Forterra (LSE:FORT) | £1.786 | £3.50 | 49% |

Below we spotlight a couple of our favorites from our exclusive screener.

Forterra (LSE:FORT)

Overview: Forterra plc manufactures and sells building products in the United Kingdom, with a market cap of £369.52 million.

Operations: Forterra's revenue segments include Bespoke Products generating £67.70 million and Bricks and Blocks contributing £261.10 million.

Estimated Discount To Fair Value: 49%

Forterra (£1.79) is trading significantly below its estimated fair value of £3.5, indicating it may be undervalued based on cash flows. Despite forecasted annual earnings growth of 42.7%, profit margins have declined from 8.9% to 2.5%. Revenue growth is expected to be slower at 8% per year compared to the UK market's 3.7%. Recent financials show a drop in sales and net income for H1 2024, with dividends also reduced from last year’s interim payout.

- Our earnings growth report unveils the potential for significant increases in Forterra's future results.

- Click here and access our complete balance sheet health report to understand the dynamics of Forterra.

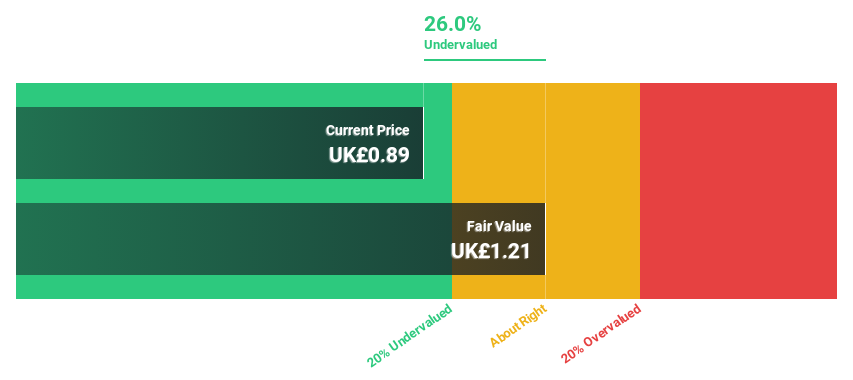

Hays (LSE:HAS)

Overview: Hays plc provides recruitment services across Australia, New Zealand, Germany, the United Kingdom, Ireland, and internationally with a market cap of £1.51 billion.

Operations: The company's revenue primarily comes from Qualified, Professional, and Skilled Recruitment services, amounting to £6.95 billion.

Estimated Discount To Fair Value: 18.3%

Hays (£0.95) is trading below its estimated fair value of £1.17, suggesting it may be undervalued based on cash flows. Despite a forecasted annual earnings growth of 63.29%, recent financials show a decline in sales to £6.95 billion and a net loss of £4.9 million for the year ended June 30, 2024, compared to net income last year. The dividend yield is currently not well covered by earnings, indicating potential sustainability issues.

- Upon reviewing our latest growth report, Hays' projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of Hays stock in this financial health report.

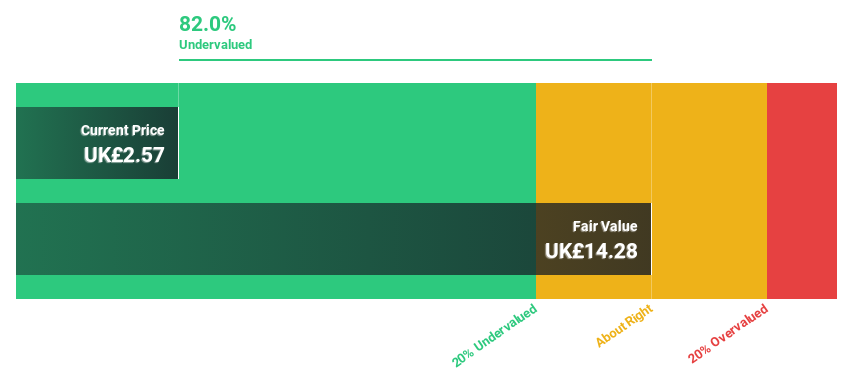

Harbour Energy (LSE:HBR)

Overview: Harbour Energy plc, with a market cap of £2.16 billion, focuses on the acquisition, exploration, development, and production of oil and gas reserves through its subsidiaries.

Operations: Harbour Energy's revenue from the acquisition, exploration, development, and production of oil and gas reserves amounts to $3.62 billion.

Estimated Discount To Fair Value: 15.3%

Harbour Energy (£2.81) trades below its estimated fair value of £3.32, indicating potential undervaluation based on cash flows. Earnings are forecast to grow 36.18% annually over the next three years, outpacing the UK market's 14.3%. Despite becoming profitable this year with a net income of US$57 million for H1 2024, revenue and production have declined compared to last year. The dividend yield of 7.01% is not well covered by earnings, raising sustainability concerns.

- Our expertly prepared growth report on Harbour Energy implies its future financial outlook may be stronger than recent results.

- Navigate through the intricacies of Harbour Energy with our comprehensive financial health report here.

Key Takeaways

- Gain an insight into the universe of 61 Undervalued UK Stocks Based On Cash Flows by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hays might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:HAS

Hays

Engages in the provision of recruitment services in Australia, New Zealand, Germany, the United Kingdom, Ireland, and internationally.

Excellent balance sheet and good value.