Advertisement

- United Kingdom

- /

- Basic Materials

- /

- LSE:BREE

Here's What Analysts Are Forecasting For Breedon Group plc (LON:BREE) After Its Half-Year Results

As you might know, Breedon Group plc (LON:BREE) recently reported its half-year numbers. Results overall were respectable, with statutory earnings of UK£0.33 per share roughly in line with what the analysts had forecast. Revenues of UK£743m came in 3.3% ahead of analyst predictions. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Breedon Group after the latest results.

View our latest analysis for Breedon Group

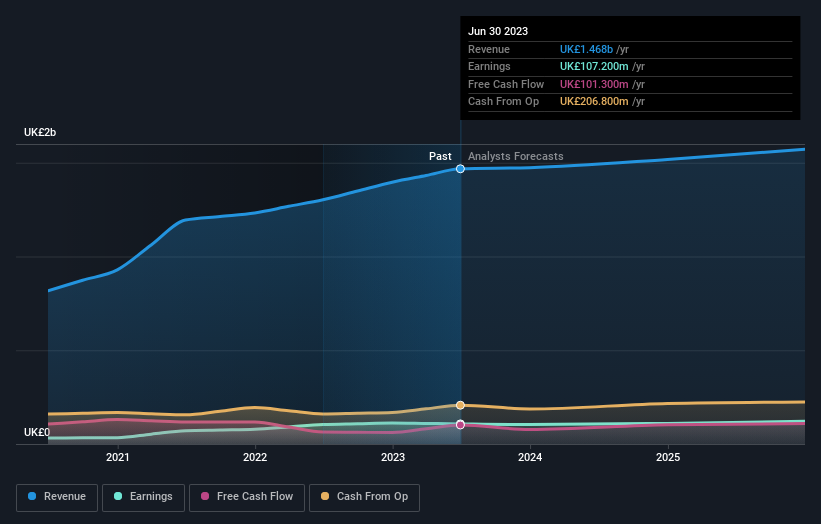

Following last week's earnings report, Breedon Group's eleven analysts are forecasting 2023 revenues to be UK£1.47b, approximately in line with the last 12 months. Statutory earnings per share are expected to decrease 5.4% to UK£0.30 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of UK£1.44b and earnings per share (EPS) of UK£0.30 in 2023. So it looks like there's been no major change in sentiment following the latest results, although the analysts have made a slight bump in to revenue forecasts.

It may not be a surprise to see thatthe analysts have reconfirmed their price target of UK£4.55, implying that the uplift in revenue is not expected to greatly contribute to Breedon Group's valuation in the near term. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Breedon Group analyst has a price target of UK£6.00 per share, while the most pessimistic values it at UK£3.80. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Breedon Group shareholders.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Breedon Group's revenue growth will slow down substantially, with revenues to the end of 2023 expected to display 0.8% growth on an annualised basis. This is compared to a historical growth rate of 14% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 3.9% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Breedon Group.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. Fortunately, they also upgraded their revenue estimates, although our data indicates it is expected to perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Breedon Group going out to 2025, and you can see them free on our platform here..

We don't want to rain on the parade too much, but we did also find 1 warning sign for Breedon Group that you need to be mindful of.

Valuation is complex, but we're here to simplify it.

Discover if Breedon Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BREE

Breedon Group

Engages in the quarrying, manufacture, and sale of construction materials and building products primarily in the United Kingdom and internationally.

Very undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor