- United Kingdom

- /

- Food and Staples Retail

- /

- AIM:KITW

Unveiling Griffin Mining And 2 Other Undiscovered Gems in the United Kingdom

Reviewed by Simply Wall St

The UK market has recently faced challenges, with the FTSE 100 closing lower amid weak trade data from China and global economic uncertainties. Despite these headwinds, there are still opportunities to uncover promising stocks that may offer significant potential. In this article, we will unveil Griffin Mining and two other undiscovered gems in the United Kingdom that could stand out in the current market landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 1.69% | 3.16% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| London Security | 0.31% | 9.47% | 7.41% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | -0.35% | 1.18% | ★★★★★★ |

| Rights and Issues Investment Trust | NA | -3.68% | -4.07% | ★★★★★★ |

| FW Thorpe | 3.34% | 11.37% | 9.41% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 6.58% | 9.90% | ★★★★★☆ |

| Mountview Estates | 16.64% | 4.50% | -0.59% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

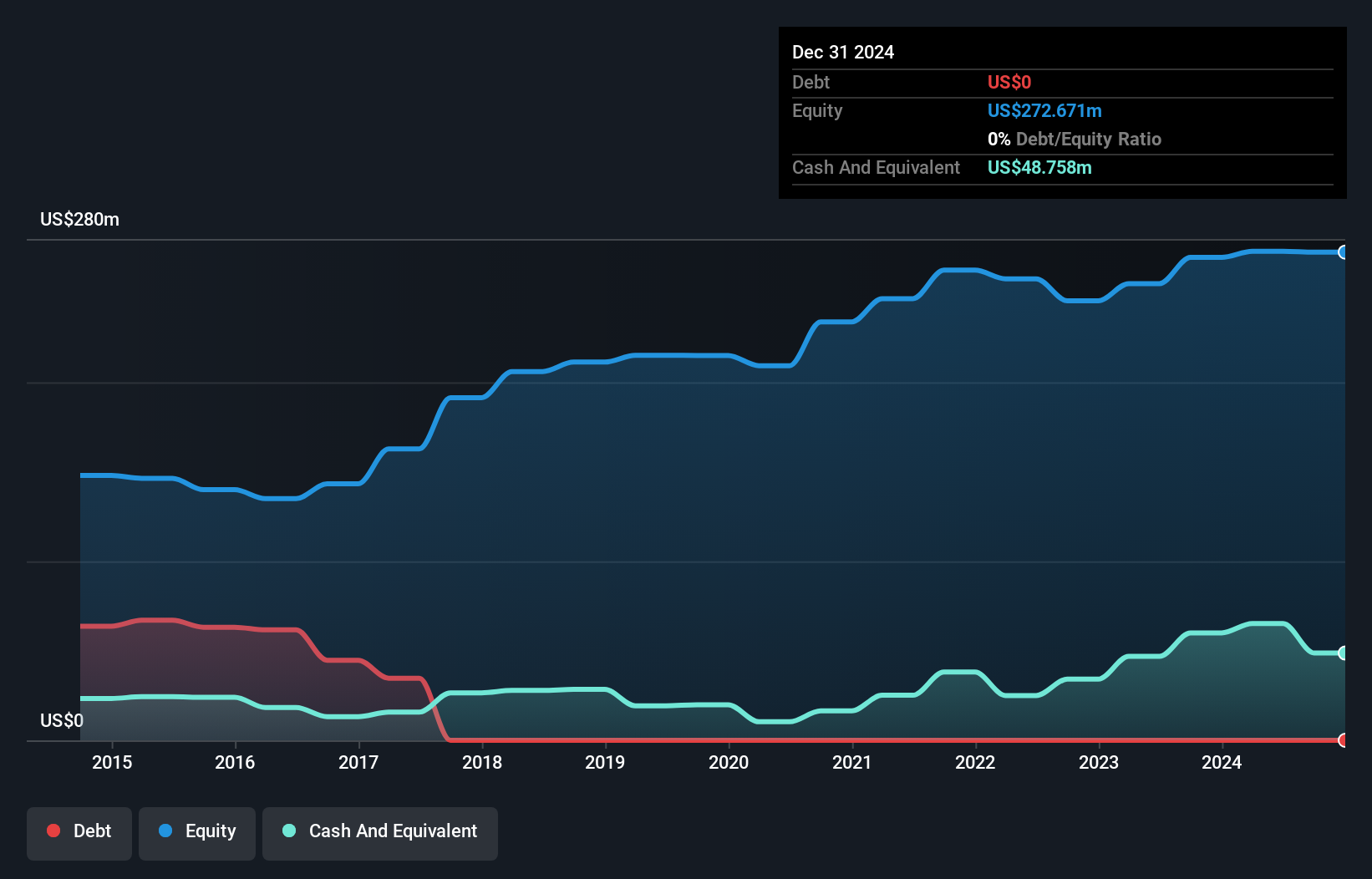

Griffin Mining (AIM:GFM)

Simply Wall St Value Rating: ★★★★★★

Overview: Griffin Mining Limited is a mining and investment company focused on the mining, exploration, and development of mineral properties with a market cap of £251.14 million.

Operations: Griffin's primary revenue stream is derived from the Caijiaying Zinc Gold Mine, generating $146.02 million. The company's market cap stands at £251.14 million.

Griffin Mining, a small-cap player in the UK, has shown impressive performance recently. Over the past year, earnings grew by 97.8%, significantly outpacing the Metals and Mining industry average of 7.6%. The company reported ore mined at 429,448 tonnes for Q2 2024 compared to 366,762 tonnes a year ago and produced gold in concentrate of 6,037 Ozs against last year's 3,237 Ozs. Trading at nearly 69% below estimated fair value and being debt-free further underscores its potential as an attractive investment opportunity.

- Unlock comprehensive insights into our analysis of Griffin Mining stock in this health report.

Understand Griffin Mining's track record by examining our Past report.

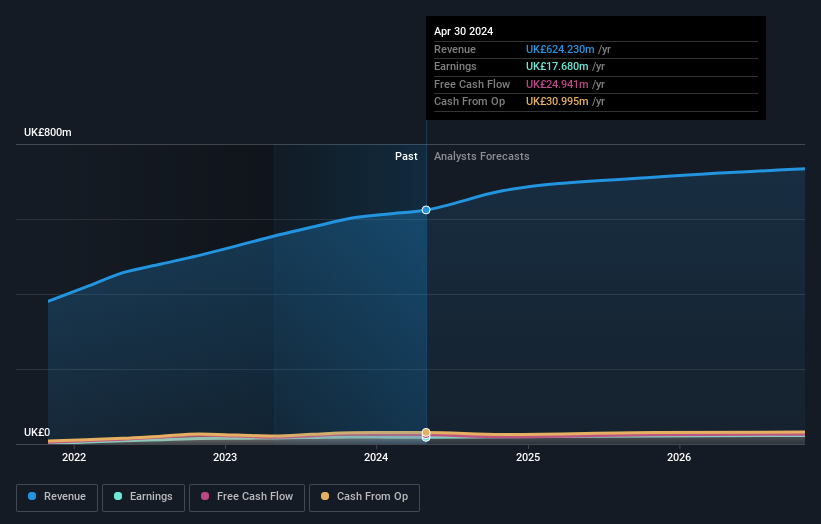

Kitwave Group (AIM:KITW)

Simply Wall St Value Rating: ★★★★★☆

Overview: Kitwave Group plc operates as a wholesale distributor in the United Kingdom with a market cap of £232.07 million.

Operations: Kitwave Group plc generates revenue from three primary segments: Ambient (£225.98 million), Foodservice (£191.60 million), and Frozen & Chilled (£229.17 million).

Kitwave Group has demonstrated robust earnings growth, averaging 40.2% annually over the past five years, though recent performance saw net income at £5.08 million for the half-year ending April 2024, down from £6.36 million a year earlier. Trading at 63% below estimated fair value, it offers significant upside potential despite a high net debt to equity ratio of 56.6%. Earnings are well-covered by EBIT (5.7x), and future growth is projected at nearly 10% per year.

- Navigate through the intricacies of Kitwave Group with our comprehensive health report here.

Review our historical performance report to gain insights into Kitwave Group's's past performance.

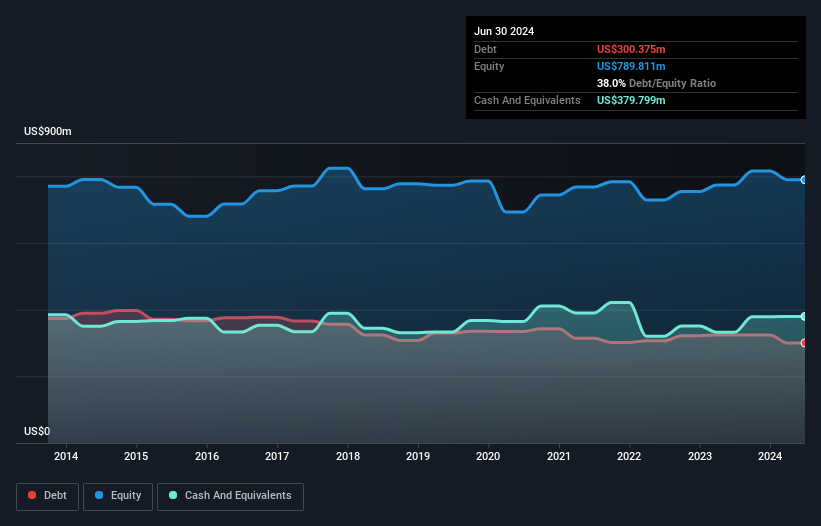

Ocean Wilsons Holdings (LSE:OCN)

Simply Wall St Value Rating: ★★★★★★

Overview: Ocean Wilsons Holdings Limited, an investment holding company with a market cap of £518.07 million, provides maritime and logistics services in Brazil.

Operations: The primary revenue stream for Ocean Wilsons Holdings comes from its maritime services in Brazil, generating $519.35 million. The company has a market cap of £518.07 million.

Ocean Wilsons Holdings, a UK-based company with significant Brazilian operations, has seen its debt to equity ratio improve from 42.7% to 38% over the past five years. Its interest payments on debt are well covered by EBIT at 4.6x coverage, and it boasts a P/E ratio of 11.1x, lower than the UK market average of 17x. Earnings surged by 32.7% last year, outpacing the infrastructure industry's growth of 20.5%. Recent discussions about selling its subsidiary Wilson Sons could further impact future performance positively or negatively depending on the outcome.

- Delve into the full analysis health report here for a deeper understanding of Ocean Wilsons Holdings.

Explore historical data to track Ocean Wilsons Holdings' performance over time in our Past section.

Turning Ideas Into Actions

- Click here to access our complete index of 80 UK Undiscovered Gems With Strong Fundamentals.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kitwave Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:KITW

Undervalued with excellent balance sheet.