Advertisement

- United Kingdom

- /

- Metals and Mining

- /

- AIM:AAZ

Is Anglo Asian Mining PLC's (LON:AAZ) Recent Performance Underpinned By Weak Financials?

With its stock down 33% over the past three months, it is easy to disregard Anglo Asian Mining (LON:AAZ). Given that stock prices are usually driven by a company’s fundamentals over the long term, which in this case look pretty weak, we decided to study the company's key financial indicators. Particularly, we will be paying attention to Anglo Asian Mining's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for Anglo Asian Mining

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Anglo Asian Mining is:

3.2% = US$3.7m ÷ US$114m (Based on the trailing twelve months to December 2022).

The 'return' is the yearly profit. Another way to think of that is that for every £1 worth of equity, the company was able to earn £0.03 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Anglo Asian Mining's Earnings Growth And 3.2% ROE

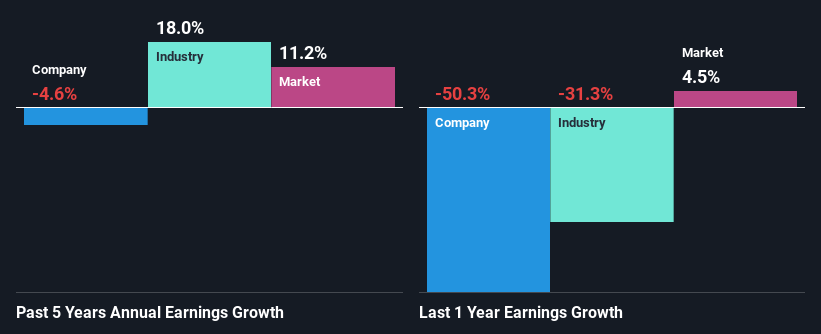

It is hard to argue that Anglo Asian Mining's ROE is much good in and of itself. Not just that, even compared to the industry average of 13%, the company's ROE is entirely unremarkable. Given the circumstances, the significant decline in net income by 4.6% seen by Anglo Asian Mining over the last five years is not surprising. However, there could also be other factors causing the earnings to decline. For instance, the company has a very high payout ratio, or is faced with competitive pressures.

So, as a next step, we compared Anglo Asian Mining's performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 18% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. What is AAZ worth today? The intrinsic value infographic in our free research report helps visualize whether AAZ is currently mispriced by the market.

Is Anglo Asian Mining Making Efficient Use Of Its Profits?

With a high three-year median payout ratio of 50% (implying that 50% of the profits are retained), most of Anglo Asian Mining's profits are being paid to shareholders, which explains the company's shrinking earnings. With only very little left to reinvest into the business, growth in earnings is far from likely. Our risks dashboard should have the 4 risks we have identified for Anglo Asian Mining.

Additionally, Anglo Asian Mining has paid dividends over a period of five years, which means that the company's management is rather focused on keeping up its dividend payments, regardless of the shrinking earnings. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 58%.

Conclusion

Overall, we would be extremely cautious before making any decision on Anglo Asian Mining. Because the company is not reinvesting much into the business, and given the low ROE, it's not surprising to see the lack or absence of growth in its earnings. Having said that, looking at current analyst estimates, we found that the company's earnings growth rate is expected to see a huge improvement. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:AAZ

Anglo Asian Mining

Owns and operates gold, silver, and copper producing properties in the Republic of Azerbaijan.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor