Stock Analysis

- United Kingdom

- /

- IT

- /

- LSE:KNOS

UK Growth Companies With High Insider Ownership And At Least 13% Earnings Growth

Reviewed by Simply Wall St

Recent market movements in the United Kingdom, particularly the FTSE 100's downturn influenced by weak trade data from China, highlight a challenging global economic environment. Amidst these conditions, growth companies with high insider ownership can offer investors potential resilience, as aligned interests between shareholders and management often drive focused execution and long-term strategic planning.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Plant Health Care (AIM:PHC) | 34.1% | 121.3% |

| Petrofac (LSE:PFC) | 16.6% | 124% |

| Gulf Keystone Petroleum (LSE:GKP) | 12.1% | 74.6% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 26.7% | 23.5% |

| Foresight Group Holdings (LSE:FSG) | 31.9% | 27.9% |

| Helios Underwriting (AIM:HUW) | 23.1% | 14.7% |

| Velocity Composites (AIM:VEL) | 27.6% | 173.3% |

| B90 Holdings (AIM:B90) | 24.4% | 142.7% |

| Judges Scientific (AIM:JDG) | 11.5% | 25.3% |

| Hochschild Mining (LSE:HOC) | 38.4% | 42.6% |

Let's dive into some prime choices out of from the screener.

Craneware (AIM:CRW)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Craneware plc, a company that develops, licenses, and supports software for the healthcare industry primarily in the United States, has a market capitalization of approximately £828.40 million.

Operations: The company generates its revenue primarily from the healthcare software segment, totaling $180.56 million.

Insider Ownership: 17%

Earnings Growth Forecast: 29.4% p.a.

Craneware, a UK-based company, demonstrates promising growth with its earnings expected to increase by 29.39% annually. Although its revenue growth is modest at 6.7% per year, it still outpaces the UK market average. Recent strategic moves include a partnership with Microsoft, leveraging Azure for enhanced healthcare analytics and AI applications, positioning Craneware for innovative advancements and market expansion through significant cloud-based initiatives and joint marketing efforts. This collaboration underscores Craneware's commitment to technological evolution and market leadership in healthcare insights.

- Click here and access our complete growth analysis report to understand the dynamics of Craneware.

- In light of our recent valuation report, it seems possible that Craneware is trading beyond its estimated value.

Judges Scientific (AIM:JDG)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Judges Scientific plc, a company that designs, manufactures, and sells scientific instruments, has a market capitalization of approximately £747.15 million.

Operations: The company generates its revenue primarily from two segments: Vacuum (£63.60 million) and Materials Sciences (£72.50 million).

Insider Ownership: 11.5%

Earnings Growth Forecast: 25.3% p.a.

Judges Scientific, a UK firm, shows robust growth prospects with earnings expected to rise by 25.32% annually over the next three years, outperforming the UK market forecast of 12.6%. However, its profit margins have decreased from 11% to 7%, and it carries a high level of debt. Despite this, insider transactions have been more about buying than selling recently. Significant corporate governance changes were also approved at their last AGM, indicating proactive management adjustments.

- Navigate through the intricacies of Judges Scientific with our comprehensive analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Judges Scientific shares in the market.

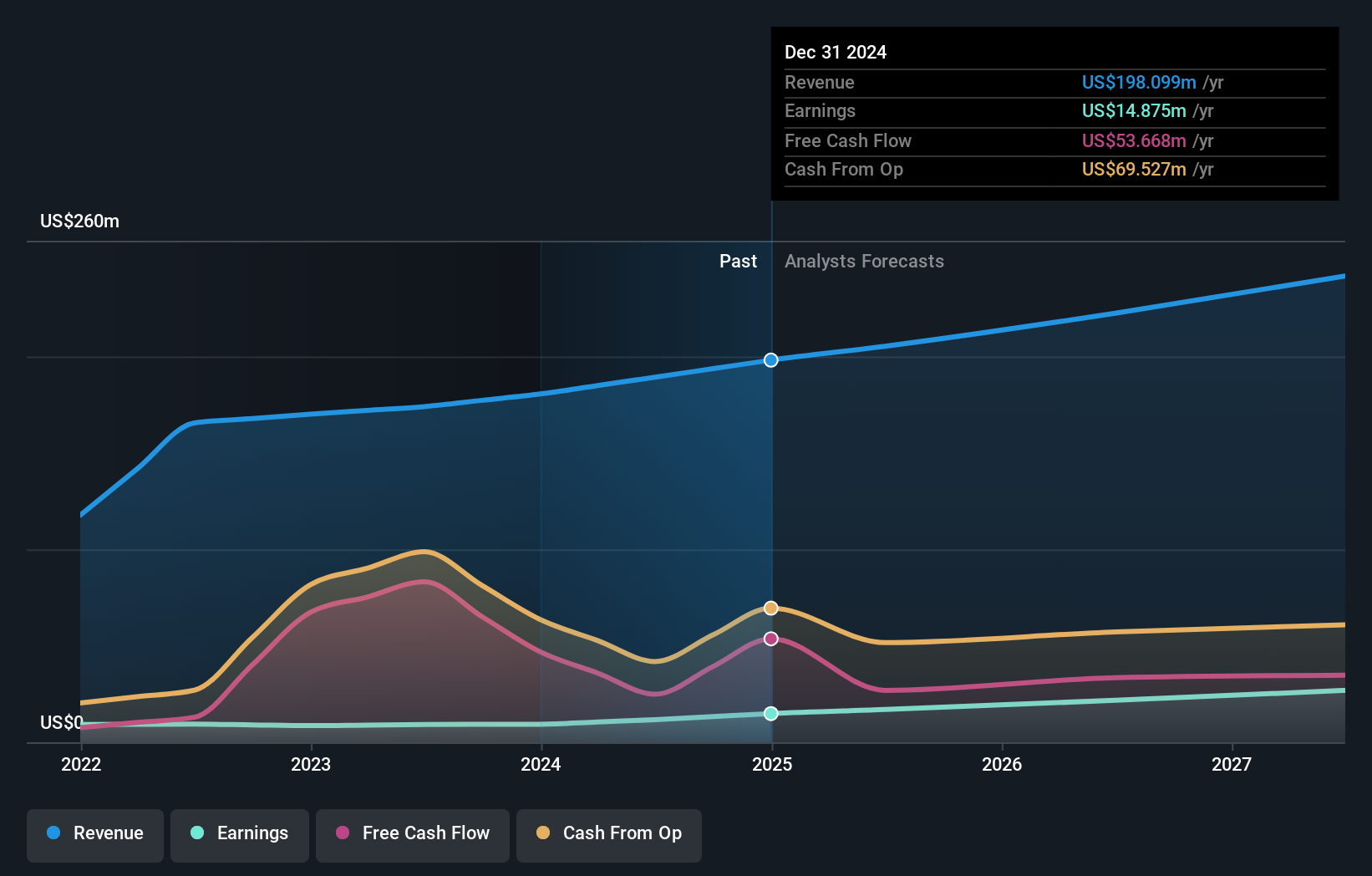

Kainos Group (LSE:KNOS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kainos Group plc operates as a provider of digital technology services across the United Kingdom, Ireland, North America, Central Europe, and other international markets, with a market capitalization of approximately £1.35 billion.

Operations: The company generates revenue primarily through three segments: Digital Services (£213.10 million), Workday Products (£57.25 million), and Workday Services (£112.04 million).

Insider Ownership: 23.3%

Earnings Growth Forecast: 13.1% p.a.

Kainos Group, a UK-based company, is demonstrating solid growth with earnings anticipated to increase by 13.09% annually. It's trading slightly below its estimated fair value and has a strong forecasted return on equity of 30.4% in three years. Recently, Kainos formed a strategic partnership with Pulsora to enhance corporate sustainability reporting through digital solutions, highlighting its commitment to ESG initiatives. However, revenue growth at 8.8% per year is modest compared to higher market expectations.

- Click to explore a detailed breakdown of our findings in Kainos Group's earnings growth report.

- Upon reviewing our latest valuation report, Kainos Group's share price might be too pessimistic.

Seize The Opportunity

- Gain an insight into the universe of 61 Fast Growing UK Companies With High Insider Ownership by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Kainos Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:KNOS

Kainos Group

Provides digital technology services in the United Kingdom, Ireland, North America, Central Europe, and internationally.

Flawless balance sheet with solid track record.