- United Kingdom

- /

- Machinery

- /

- AIM:JDG

3 Top Growth Companies With High Insider Ownership On The UK Exchange

Reviewed by Simply Wall St

Over the last 7 days, the market has dropped 2.0%. In contrast to the last week, the market is up 5.0% over the past year, with earnings forecast to grow by 14% annually. In this context, identifying growth companies with high insider ownership can be crucial as it often signals confidence in long-term prospects and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Filtronic (AIM:FTC) | 28.6% | 33.5% |

| Plant Health Care (AIM:PHC) | 34.7% | 121.3% |

| Gulf Keystone Petroleum (LSE:GKP) | 12.1% | 74.6% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 26.7% | 23.5% |

| Foresight Group Holdings (LSE:FSG) | 31.9% | 27.9% |

| Helios Underwriting (AIM:HUW) | 23.9% | 14.7% |

| Belluscura (AIM:BELL) | 39.5% | 117.8% |

| Velocity Composites (AIM:VEL) | 27.6% | 173.3% |

| B90 Holdings (AIM:B90) | 24.4% | 142.7% |

| Hochschild Mining (LSE:HOC) | 38.4% | 53.8% |

Here's a peek at a few of the choices from the screener.

Craneware (AIM:CRW)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Craneware plc, with a market cap of £821.41 million, develops, licenses, and supports computer software for the healthcare industry in the United States.

Operations: Revenue from healthcare software amounts to $180.56 million.

Insider Ownership: 17%

Craneware, a growth company with high insider ownership, is forecasted to achieve significant annual earnings growth of 29.39% over the next three years, outpacing the UK market's 13.5%. Despite a lower projected Return on Equity of 11.2%, Craneware's revenue is expected to grow at 6.7% annually, faster than the market average. Recent strategic collaborations with Microsoft enhance its innovation capabilities and market reach through Azure Marketplace integrations and AI advancements in healthcare solutions.

- Navigate through the intricacies of Craneware with our comprehensive analyst estimates report here.

- Our expertly prepared valuation report Craneware implies its share price may be too high.

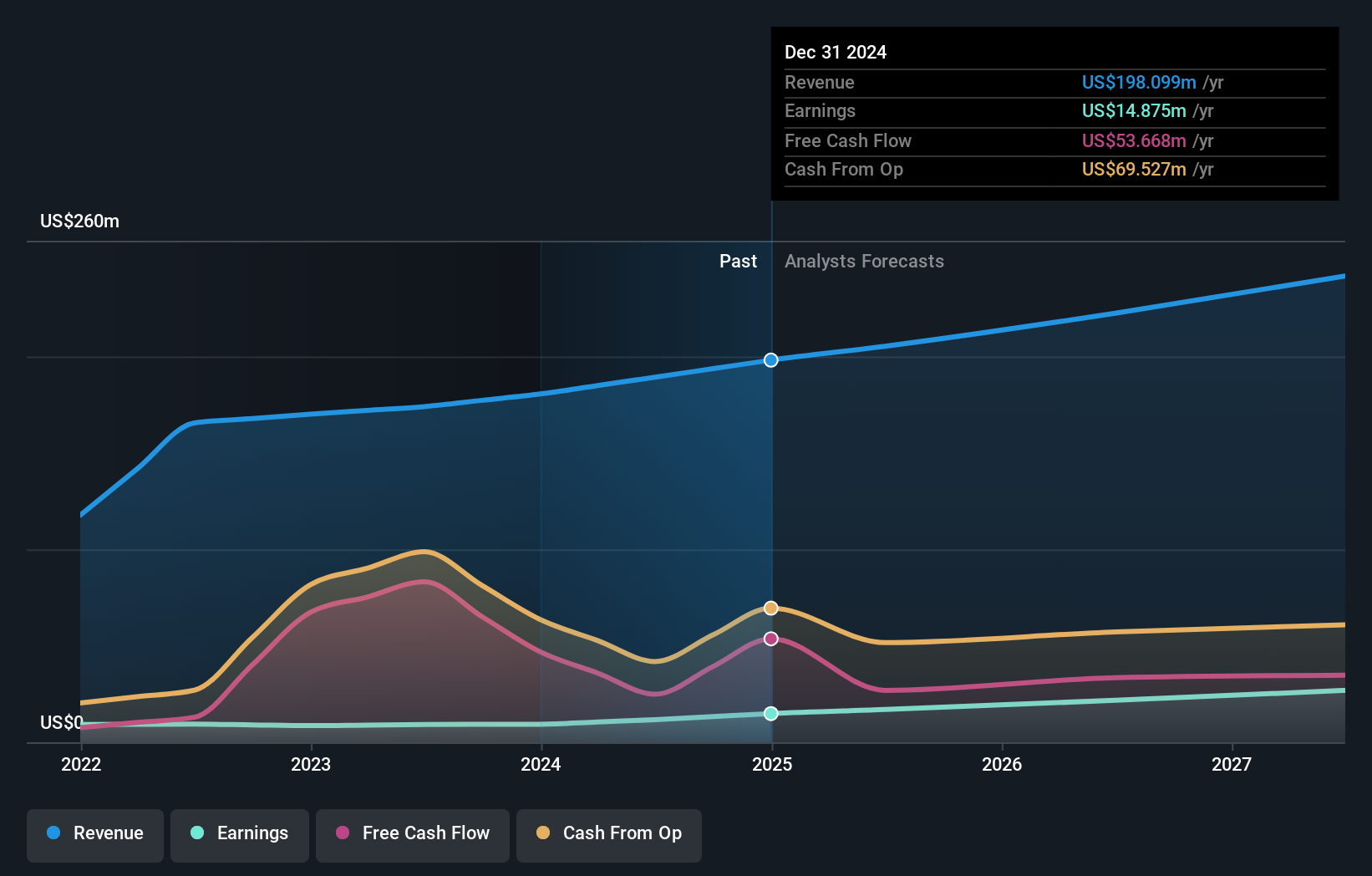

Judges Scientific (AIM:JDG)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Judges Scientific plc designs, manufactures, and sells scientific instruments with a market cap of £664.13 million.

Operations: The company generates revenue from two main segments: Vacuum (£63.60 million) and Materials Sciences (£72.50 million).

Insider Ownership: 11.9%

Judges Scientific, characterized by high insider ownership, is projected to achieve significant annual earnings growth of 26.22% over the next three years, surpassing the UK market's 13.5%. Despite a recent decline in profit margins from 11% to 7%, analysts agree that its stock price will rise by 20.1%. Recent changes in company bylaws and a final dividend increase to £0.68 per share were approved at the May AGM, reflecting strong governance and shareholder returns.

- Unlock comprehensive insights into our analysis of Judges Scientific stock in this growth report.

- According our valuation report, there's an indication that Judges Scientific's share price might be on the expensive side.

Property Franchise Group (AIM:TPFG)

Simply Wall St Growth Rating: ★★★★★☆

Overview: The Property Franchise Group PLC, with a market cap of £288.58 million, manages and leases residential real estate properties in the United Kingdom.

Operations: The company generates revenue from two main segments: Property Franchising (£25.78 million) and Financial Services (£1.50 million).

Insider Ownership: 13.5%

Property Franchise Group, with substantial insider ownership, is forecasted to achieve significant annual earnings growth of 36.7% over the next three years, outpacing the UK market's 13.5%. Despite recent shareholder dilution and an unstable dividend track record, its revenue is expected to grow at a robust rate of 44.7% per year. The company recently announced CFO David Raggett's planned retirement in 2025, ensuring a smooth transition period for leadership continuity.

- Click to explore a detailed breakdown of our findings in Property Franchise Group's earnings growth report.

- The valuation report we've compiled suggests that Property Franchise Group's current price could be inflated.

Key Takeaways

- Click through to start exploring the rest of the 63 Fast Growing UK Companies With High Insider Ownership now.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:JDG

Judges Scientific

Designs, manufactures, and sells scientific instruments.

High growth potential moderate.