- United Kingdom

- /

- Food and Staples Retail

- /

- AIM:KITW

Kitwave Group And 2 Other Undiscovered Gems With Promising Potential

Reviewed by Simply Wall St

The United Kingdom's stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices slipping due to weak trade data from China, highlighting concerns about global economic recovery and its impact on commodity-driven companies. Amidst this backdrop of uncertainty, identifying promising small-cap stocks can be a strategic move for investors seeking opportunities that are less dependent on global macroeconomic trends. In this context, Kitwave Group and two other lesser-known stocks emerge as potential gems worth exploring for their unique market positions and growth prospects.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | 17.28% | 15.80% | ★★★★★★ |

| Metals Exploration | NA | 12.92% | 73.62% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Kodal Minerals | NA | nan | 72.74% | ★★★★★★ |

| VH Global Sustainable Energy Opportunities | NA | 18.30% | 20.03% | ★★★★★★ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

Here's a peek at a few of the choices from the screener.

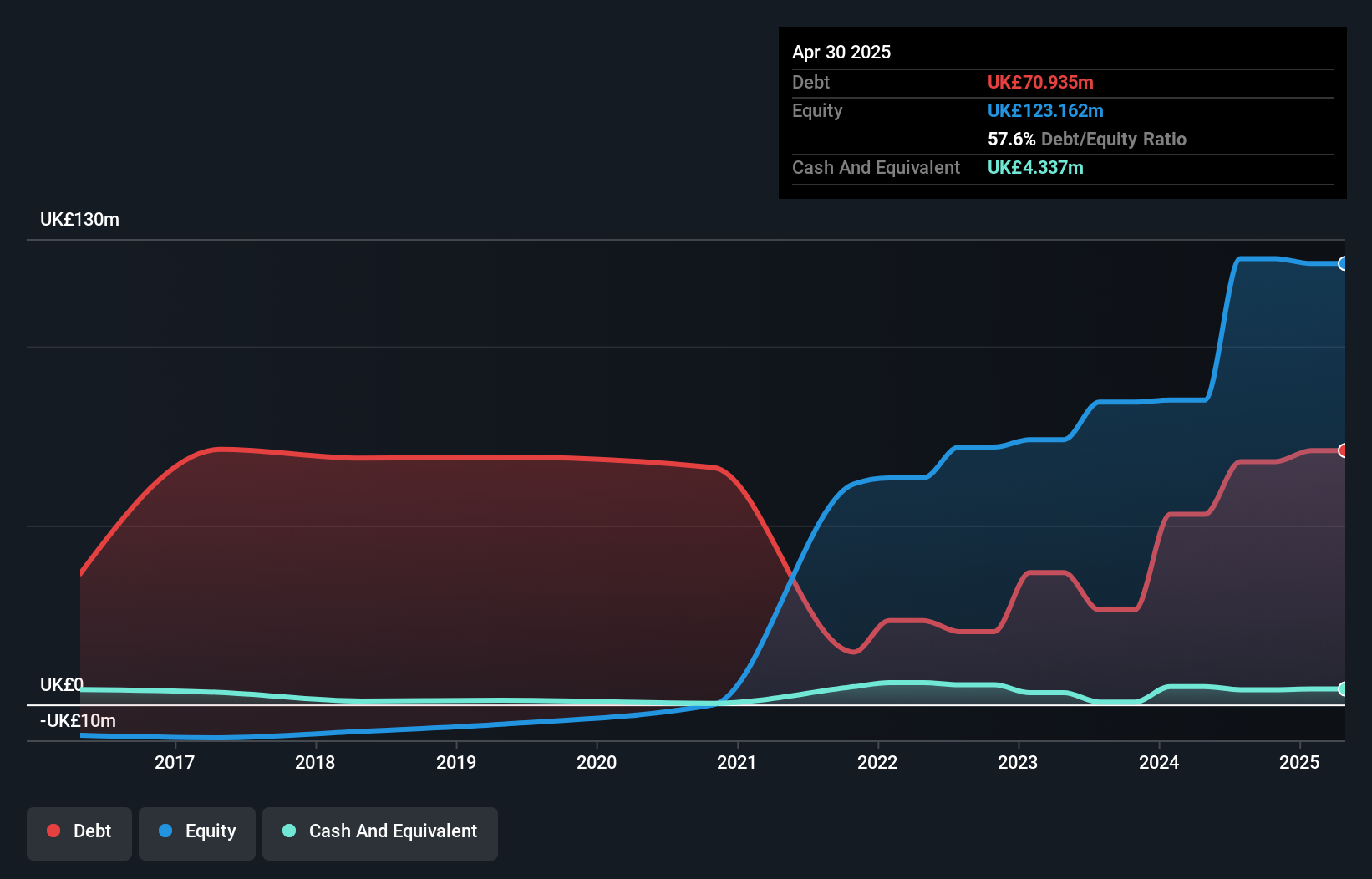

Kitwave Group (AIM:KITW)

Simply Wall St Value Rating: ★★★★★☆

Overview: Kitwave Group plc operates as a wholesale business in the United Kingdom with a market capitalization of £269.87 million.

Operations: Kitwave Group generates revenue primarily from its Ambient (£225.98 million), Foodservice (£191.60 million), and Frozen & Chilled (£229.17 million) segments, with a segment adjustment of -£2.94 million affecting the total figures.

Kitwave, a notable player in the UK market, has seen its earnings grow impressively at 40% annually over five years. Despite this growth, recent earnings of 8.7% lagged behind the industry average of 9.3%. The company carries a high net debt to equity ratio of 56.6%, yet it manages interest payments well with EBIT covering them 5.7 times over. Recently, Kitwave completed a £31 million follow-on equity offering priced at £3.05 per share, which may impact shareholder value perceptions due to dilution concerns but could provide capital for future ventures or debt management strategies.

- Get an in-depth perspective on Kitwave Group's performance by reading our health report here.

Understand Kitwave Group's track record by examining our Past report.

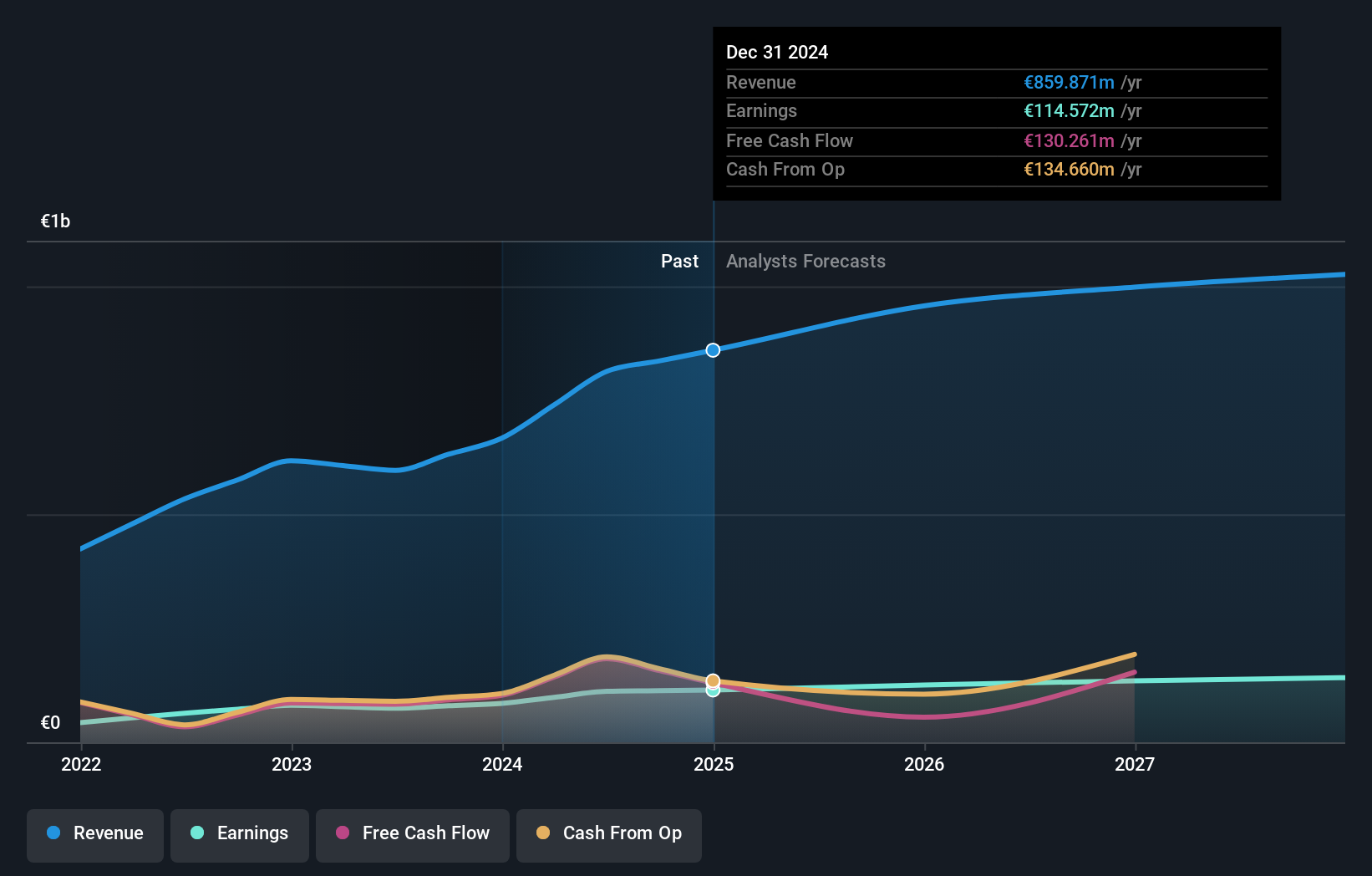

Cairn Homes (LSE:CRN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cairn Homes plc is a holding company that functions as a home and community builder in Ireland, with a market capitalization of £1.07 billion.

Operations: Cairn Homes generates revenue primarily through its building and property development segment, which reported €813.40 million in revenue.

Cairn Homes, a noteworthy player in the UK market, has demonstrated robust financial health with earnings surging 49.5% over the past year, outpacing its industry peers. The company's net debt to equity ratio stands at a satisfactory 20.7%, reflecting prudent financial management, while its price-to-earnings ratio of 11.4x suggests good value compared to the broader UK market average of 16.4x. Recently, Cairn Homes repurchased shares worth €70 million and reported half-year sales of €366 million with net income reaching €46.89 million.

- Take a closer look at Cairn Homes' potential here in our health report.

Gain insights into Cairn Homes' historical performance by reviewing our past performance report.

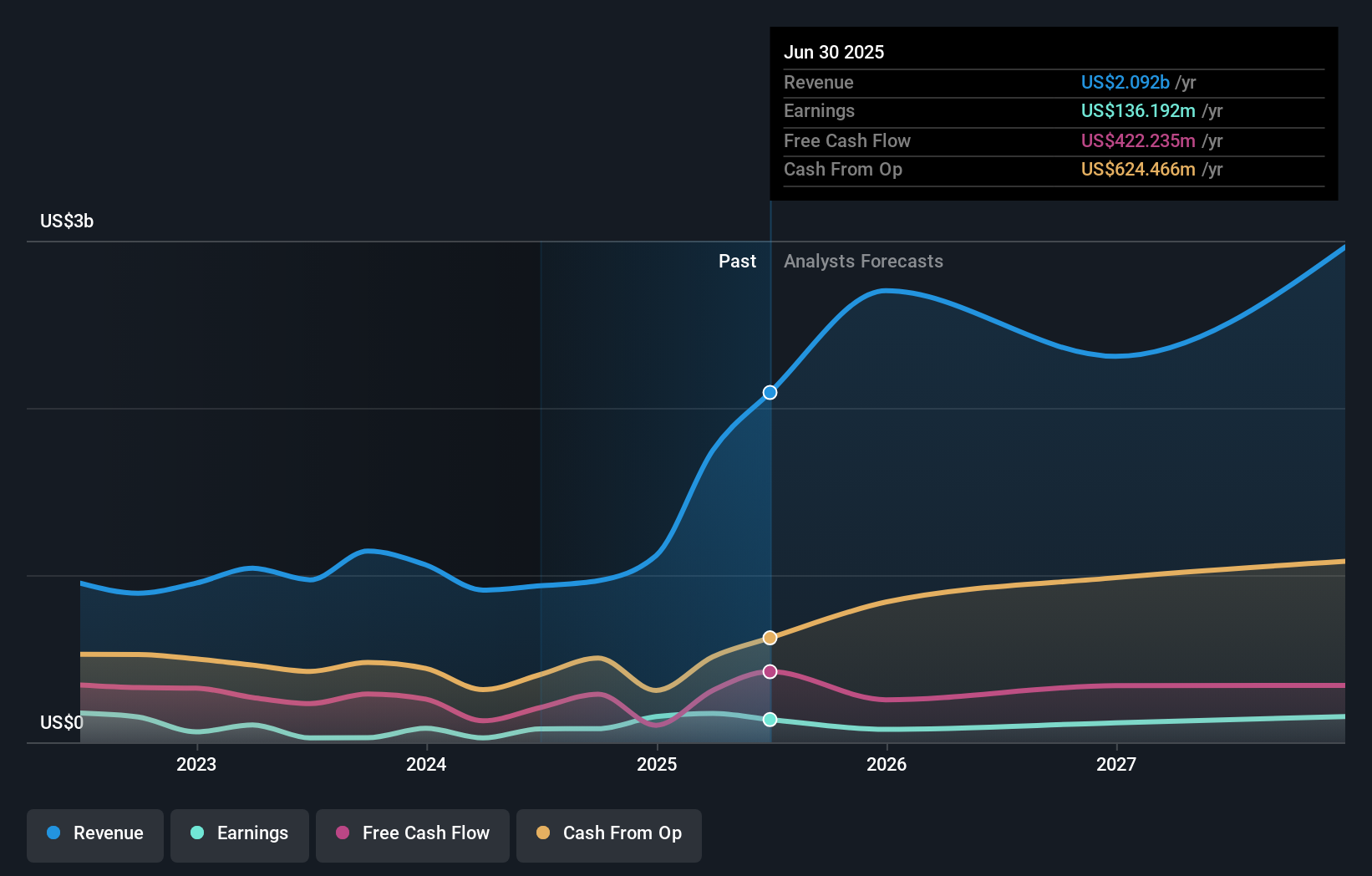

Seplat Energy (LSE:SEPL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Seplat Energy Plc is involved in oil and gas exploration, production, and gas processing across Nigeria, the Bahamas, Italy, Switzerland, Barbados, and England with a market cap of £1.25 billion.

Operations: Seplat Energy generates revenue primarily from oil and gas, with oil contributing $815.03 million and gas $120.87 million.

Seplat Energy, a dynamic player in the UK's oil and gas sector, has shown impressive earnings growth of 208% over the past year, outpacing its industry peers. With sales reaching US$241.82 million in Q2 2024, up from US$216.03 million last year, it seems to be on a solid path despite a net debt to equity ratio rising to 41.5%. The company’s interest payments are well-covered by EBIT at 5.8 times coverage, indicating robust financial health amidst fluctuating production levels.

- Click here to discover the nuances of Seplat Energy with our detailed analytical health report.

Review our historical performance report to gain insights into Seplat Energy's's past performance.

Turning Ideas Into Actions

- Investigate our full lineup of 81 UK Undiscovered Gems With Strong Fundamentals right here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kitwave Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:KITW

Excellent balance sheet and good value.