Advertisement

- United Kingdom

- /

- Machinery

- /

- LSE:TRI

Results: Trifast plc Exceeded Expectations And The Consensus Has Updated Its Estimates

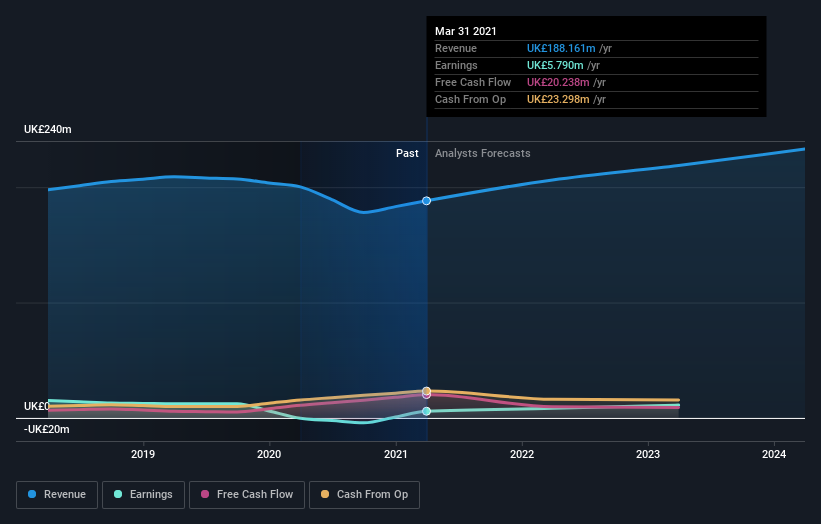

Trifast plc (LON:TRI) came out with its annual results last week, and we wanted to see how the business is performing and what industry forecasters think of the company following this report. Trifast reported UK£188m in revenue, roughly in line with analyst forecasts, although statutory earnings per share (EPS) of UK£0.043 beat expectations, being 6.4% higher than what the analysts expected. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

See our latest analysis for Trifast

Taking into account the latest results, the current consensus from Trifast's six analysts is for revenues of UK£206.3m in 2022, which would reflect a decent 9.6% increase on its sales over the past 12 months. Statutory earnings per share are predicted to shoot up 39% to UK£0.06. Before this earnings report, the analysts had been forecasting revenues of UK£205.7m and earnings per share (EPS) of UK£0.052 in 2022. Although the revenue estimates have not really changed, we can see there's been a nice increase in earnings per share expectations, suggesting that the analysts have become more bullish after the latest result.

The consensus price target was unchanged at UK£1.77, implying that the improved earnings outlook is not expected to have a long term impact on value creation for shareholders. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Trifast at UK£1.90 per share, while the most bearish prices it at UK£1.55. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Trifast is an easy business to forecast or the the analysts are all using similar assumptions.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The analysts are definitely expecting Trifast's growth to accelerate, with the forecast 9.6% annualised growth to the end of 2022 ranking favourably alongside historical growth of 2.1% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 4.8% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Trifast to grow faster than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Trifast following these results. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Trifast going out to 2024, and you can see them free on our platform here.

We also provide an overview of the Trifast Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

If you’re looking to trade Trifast, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Trifast might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About LSE:TRI

Trifast

Designs, engineers, manufactures, and supplies industrial fasteners and category C components in the United Kingdom, Ireland, Europe, North America, and Asia.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor