Advertisement

- Spain

- /

- Metals and Mining

- /

- BME:TRG

Tubos Reunidos (BME:TRG) Shareholders Will Want The ROCE Trajectory To Continue

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Speaking of which, we noticed some great changes in Tubos Reunidos' (BME:TRG) returns on capital, so let's have a look.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Tubos Reunidos is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

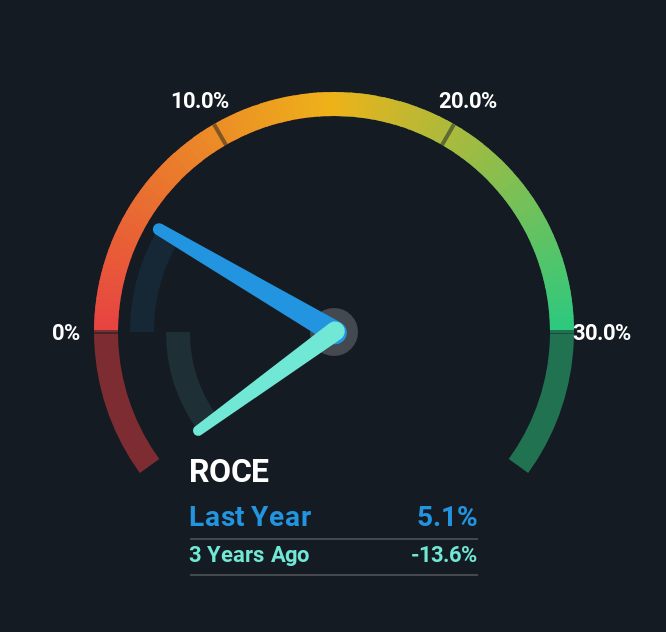

0.051 = €15m ÷ (€452m - €147m) (Based on the trailing twelve months to June 2025).

Therefore, Tubos Reunidos has an ROCE of 5.1%. In absolute terms, that's a low return and it also under-performs the Metals and Mining industry average of 9.5%.

View our latest analysis for Tubos Reunidos

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Tubos Reunidos.

So How Is Tubos Reunidos' ROCE Trending?

We're delighted to see that Tubos Reunidos is reaping rewards from its investments and has now broken into profitability. The company now earns 5.1% on its capital, because five years ago it was incurring losses. While returns have increased, the amount of capital employed by Tubos Reunidos has remained flat over the period. So while we're happy that the business is more efficient, just keep in mind that could mean that going forward the business is lacking areas to invest internally for growth. After all, a company can only become a long term multi-bagger if it continually reinvests in itself at high rates of return.

In Conclusion...

As discussed above, Tubos Reunidos appears to be getting more proficient at generating returns since capital employed has remained flat but earnings (before interest and tax) are up. And investors seem to expect more of this going forward, since the stock has rewarded shareholders with a 44% return over the last five years. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

One more thing, we've spotted 2 warning signs facing Tubos Reunidos that you might find interesting.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Tubos Reunidos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:TRG

Tubos Reunidos

Engages in the manufacture and sale of seamless steel pipe products in the United States, the United Kingdom, Germany, Italy, Spain, Saudi Arabia, Mexico, South Korea, the Netherlands, and internationally.

Very low risk with worrying balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor