Stock Analysis

- Germany

- /

- Real Estate

- /

- XTRA:PAT

Investors three-year losses continue as PATRIZIA (ETR:PAT) dips a further 8.1% this week, earnings continue to decline

If you love investing in stocks you're bound to buy some losers. Long term PATRIZIA SE (ETR:PAT) shareholders know that all too well, since the share price is down considerably over three years. Regrettably, they have had to cope with a 63% drop in the share price over that period. On top of that, the share price is down 8.1% in the last week.

Since PATRIZIA has shed €61m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

View our latest analysis for PATRIZIA

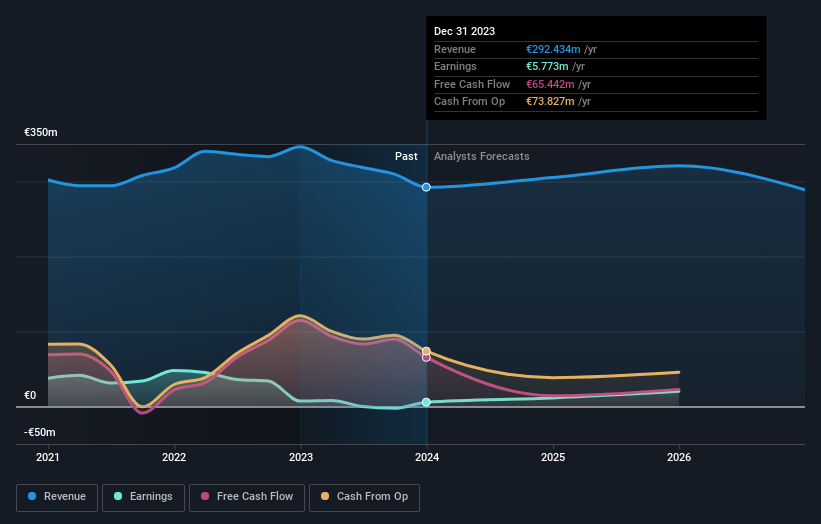

We don't think that PATRIZIA's modest trailing twelve month profit has the market's full attention at the moment. We think revenue is probably a better guide. Generally speaking, we'd consider a stock like this alongside loss-making companies, simply because the quantum of the profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

Over three years, PATRIZIA grew revenue at 1.6% per year. That's not a very high growth rate considering it doesn't make profits. This uninspiring revenue growth has no doubt helped send the share price lower; it dropped 18% during the period. When a stock falls hard like this, some investors like to add the company to a watchlist (in case the business recovers, longer term). Keep in mind it isn't unusual for good businesses to have a tough time or a couple of uninspiring years.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

Balance sheet strength is crucial. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. In the case of PATRIZIA, it has a TSR of -60% for the last 3 years. That exceeds its share price return that we previously mentioned. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

Investors in PATRIZIA had a tough year, with a total loss of 9.3% (including dividends), against a market gain of about 4.6%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Unfortunately, longer term shareholders are suffering worse, given the loss of 9% doled out over the last five years. We'd need to see some sustained improvements in the key metrics before we could muster much enthusiasm. It's always interesting to track share price performance over the longer term. But to understand PATRIZIA better, we need to consider many other factors. For example, we've discovered 2 warning signs for PATRIZIA that you should be aware of before investing here.

But note: PATRIZIA may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on German exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether PATRIZIA is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:PAT

PATRIZIA

With operations around the world, PATRIZIA has been offering investment opportunities in real estate and infrastructure assets for institutional, semi-professional and private investors for 40 years.

Moderate growth potential with mediocre balance sheet.