Stock Analysis

- Germany

- /

- Electrical

- /

- XTRA:CEA

FRIWO (ETR:CEA shareholders incur further losses as stock declines 12% this week, taking one-year losses to 43%

The simplest way to benefit from a rising market is to buy an index fund. When you buy individual stocks, you can make higher profits, but you also face the risk of under-performance. Investors in FRIWO AG (ETR:CEA) have tasted that bitter downside in the last year, as the share price dropped 43%. That's disappointing when you consider the market returned 5.7%. At least the damage isn't so bad if you look at the last three years, since the stock is down 20% in that time. Shareholders have had an even rougher run lately, with the share price down 25% in the last 90 days. We note that the company has reported results fairly recently; and the market is hardly delighted. You can check out the latest numbers in our company report.

If the past week is anything to go by, investor sentiment for FRIWO isn't positive, so let's see if there's a mismatch between fundamentals and the share price.

See our latest analysis for FRIWO

FRIWO isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. When a company doesn't make profits, we'd generally hope to see good revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

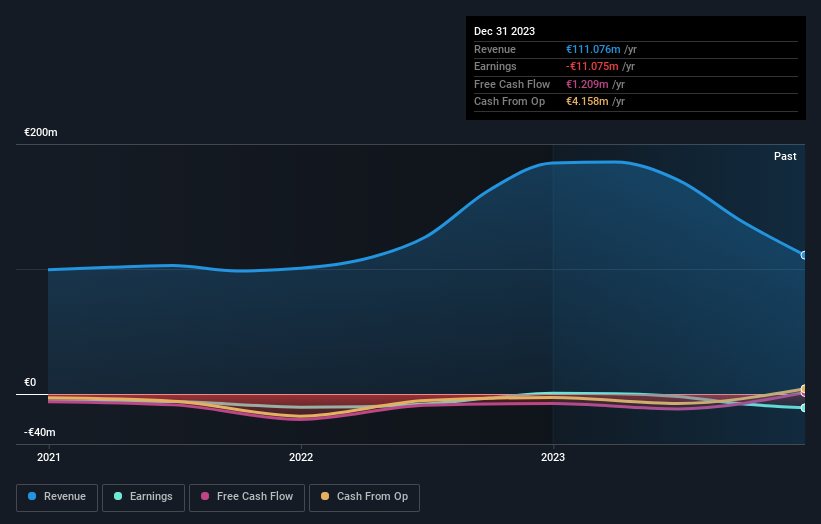

FRIWO's revenue didn't grow at all in the last year. In fact, it fell 40%. That's not what investors generally want to see. Shareholders have seen the share price drop 43% in that time. That seems pretty reasonable given the lack of both profits and revenue growth. We think most holders must believe revenue growth will improve, or else costs will decline.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

Take a more thorough look at FRIWO's financial health with this free report on its balance sheet.

A Different Perspective

While the broader market gained around 5.7% in the last year, FRIWO shareholders lost 43%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 1.4% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For instance, we've identified 2 warning signs for FRIWO (1 makes us a bit uncomfortable) that you should be aware of.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on German exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether FRIWO is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:CEA

FRIWO

FRIWO AG develops, manufactures, and sells power supplies units and drive solutions worldwide.

Adequate balance sheet with weak fundamentals.