- Cyprus

- /

- Hospitality

- /

- CSE:SAL

Investors in Salamis Tours (Holdings) (CSE:SAL) have seen fantastic returns of 489% over the past five years

Long term investing can be life changing when you buy and hold the truly great businesses. And highest quality companies can see their share prices grow by huge amounts. Don't believe it? Then look at the Salamis Tours (Holdings) Public Limited (CSE:SAL) share price. It's 340% higher than it was five years ago. This just goes to show the value creation that some businesses can achieve. Also pleasing for shareholders was the 20% gain in the last three months.

So let's investigate and see if the longer term performance of the company has been in line with the underlying business' progress.

See our latest analysis for Salamis Tours (Holdings)

SWOT Analysis for Salamis Tours (Holdings)

- Earnings growth over the past year exceeded the industry.

- Currently debt free.

- Dividends are covered by earnings and cash flows.

- Dividend is low compared to the top 25% of dividend payers in the Hospitality market.

- Trading below our estimate of fair value by more than 20%.

- Lack of analyst coverage makes it difficult to determine SAL's earnings prospects.

- No apparent threats visible for SAL.

To quote Buffett, 'Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace...' One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

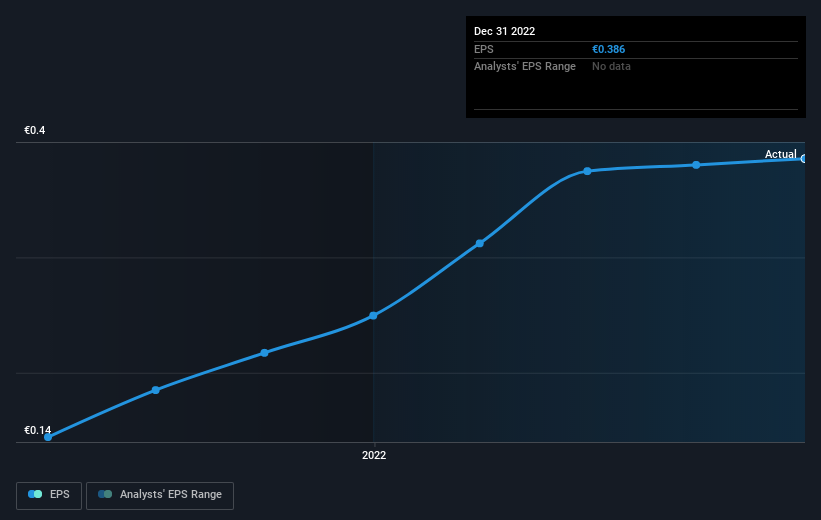

Over half a decade, Salamis Tours (Holdings) managed to grow its earnings per share at 22% a year. This EPS growth is lower than the 34% average annual increase in the share price. This suggests that market participants hold the company in higher regard, these days. That's not necessarily surprising considering the five-year track record of earnings growth.

The company's earnings per share (over time) is depicted in the image below (click to see the exact numbers).

It might be well worthwhile taking a look at our free report on Salamis Tours (Holdings)'s earnings, revenue and cash flow.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. We note that for Salamis Tours (Holdings) the TSR over the last 5 years was 489%, which is better than the share price return mentioned above. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

Salamis Tours (Holdings) shareholders are up 42% for the year (even including dividends). But that was short of the market average. It's probably a good sign that the company has an even better long term track record, having provided shareholders with an annual TSR of 43% over five years. It's quite possible the business continues to execute with prowess, even as the share price gains are slowing. It's always interesting to track share price performance over the longer term. But to understand Salamis Tours (Holdings) better, we need to consider many other factors. Case in point: We've spotted 2 warning signs for Salamis Tours (Holdings) you should be aware of.

Of course Salamis Tours (Holdings) may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Cypriot exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About CSE:SAL

Salamis Tours (Holdings)

Operates in the travel, tourism, cruise, shipping, and transport sectors in Cyprus and Greece.

Flawless balance sheet second-rate dividend payer.