- Taiwan

- /

- Electronic Equipment and Components

- /

- TPEX:3211

Three Undiscovered Gems with Promising Potential

Reviewed by Simply Wall St

In a week marked by busy earnings reports and mixed economic data, global markets experienced volatility with major indices like the S&P 500 and Nasdaq Composite pulling back after reaching record highs. Amidst this backdrop, small-cap stocks showed resilience, suggesting potential opportunities for investors willing to explore beyond the larger market players. In such an environment, identifying promising stocks often involves looking for companies with strong fundamentals that can weather economic uncertainties while capitalizing on niche market positions or innovative growth strategies.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Winstek Semiconductor | 11.42% | 9.38% | 24.14% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Fourth Milling | NA | 4.35% | 29.30% | ★★★★★☆ |

| Billion Industrial Holdings | 3.63% | 18.00% | -11.38% | ★★★★★☆ |

| Jamuna Bank | 85.07% | 7.37% | -3.87% | ★★★★☆☆ |

| Can-One Berhad | 88.80% | 9.35% | 23.83% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

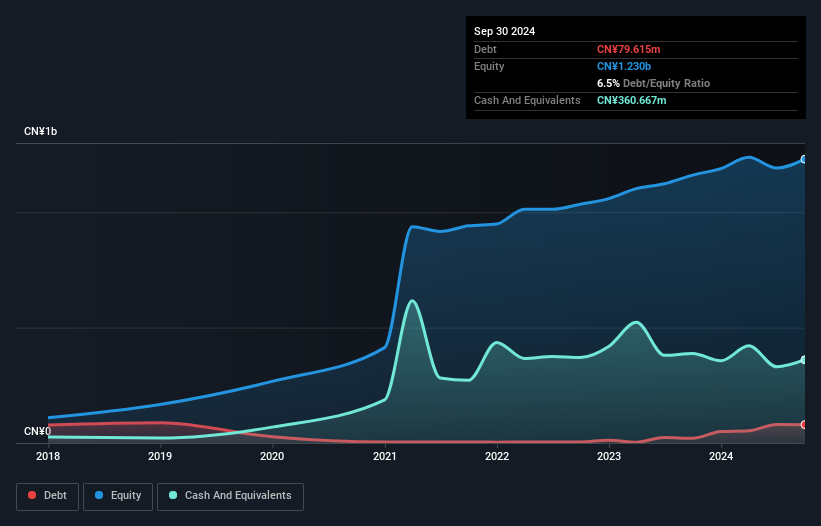

Uni-Trend Technology (China) (SHSE:688628)

Simply Wall St Value Rating: ★★★★★★

Overview: Uni-Trend Technology (China) Co., Ltd. designs and manufactures test and measurement products worldwide, with a market cap of CN¥4.44 billion.

Operations: Uni-Trend Technology generates revenue primarily from the sale of its test and measurement products. The company focuses on optimizing its cost structure to enhance profitability, with a particular emphasis on managing production and operational expenses. Notably, Uni-Trend's gross profit margin has shown interesting variations over recent periods, reflecting changes in pricing strategies and cost efficiencies.

Uni-Trend Technology, a nimble player in the electronics sector, has shown impressive earnings growth of 15.6% over the past year, outpacing the industry's 1.7%. Trading at a notable 38.7% below its estimated fair value suggests potential for investors seeking undervalued opportunities. The company's debt to equity ratio has improved significantly from 17.6% to 6.5% over five years, indicating better financial health and reduced leverage risks. Recent earnings reports reveal sales of CNY 853 million and net income of CNY 152 million for nine months ending September, with basic EPS rising from CNY 1.19 to CNY 1.37 year-on-year.

- Click here and access our complete health analysis report to understand the dynamics of Uni-Trend Technology (China).

Learn about Uni-Trend Technology (China)'s historical performance.

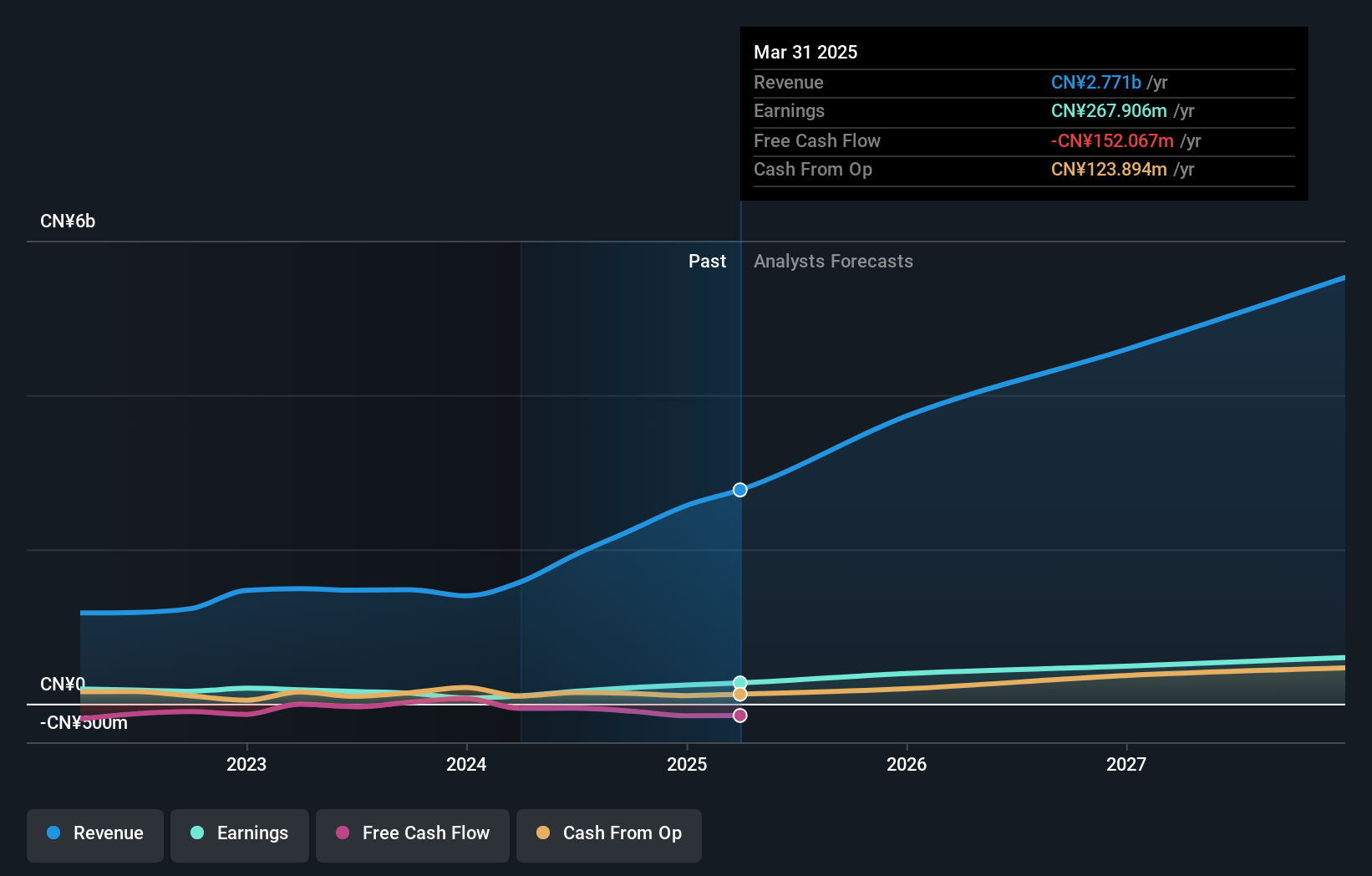

Dongguan Tarry ElectronicsLtd (SZSE:300976)

Simply Wall St Value Rating: ★★★★★★

Overview: Dongguan Tarry Electronics Co., Ltd. operates in China, specializing in the manufacturing and sale of precision die cutting products, foam protective film tapes, insulation heat conduction products, EMI shielding products, sewing and high frequency earmuffs, headbands, and assembly automation equipment with a market cap of approximately CN¥5.85 billion.

Operations: With revenue from the manufacturing industry amounting to approximately CN¥2.24 billion, Dongguan Tarry Electronics Co., Ltd. focuses on precision die cutting and related products. The company's financial performance is highlighted by its gross profit margin trends, which provide insight into cost management and pricing strategies within its core operations.

Dongguan Tarry Electronics, a nimble player in the electronics sector, has shown impressive growth with earnings surging 53% over the past year. The company reported nine-month sales of CNY 1.77 billion, significantly up from CNY 925.06 million a year ago, while net income climbed to CNY 182.14 million from CNY 47.78 million. Trading at a price-to-earnings ratio of 28x, it offers good value relative to the CN market average of 36x. Despite its high-quality earnings and robust performance exceeding industry growth rates, its free cash flow remains negative and share price has been volatile recently.

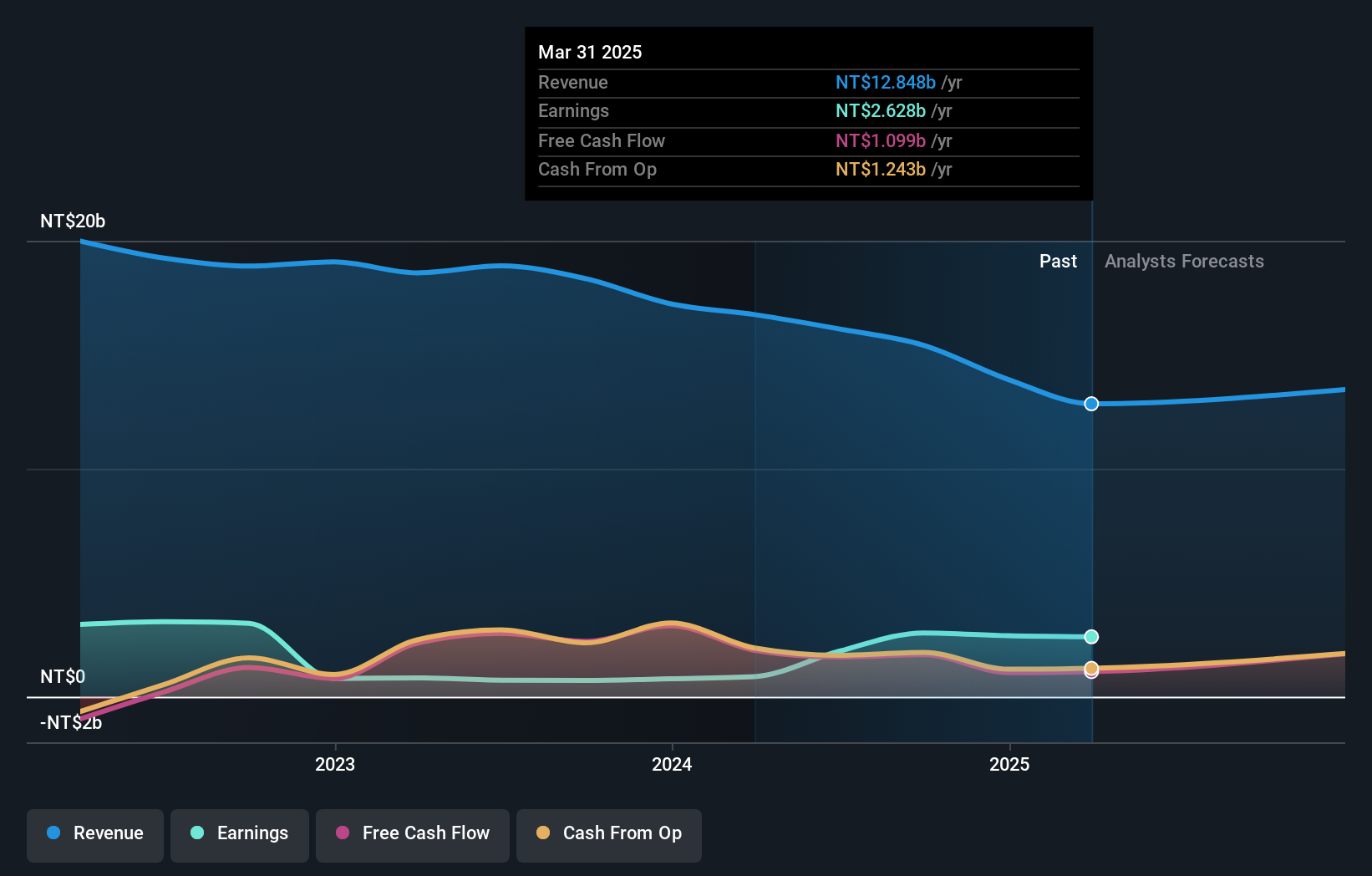

Dynapack International Technology (TPEX:3211)

Simply Wall St Value Rating: ★★★★★★

Overview: Dynapack International Technology Corporation specializes in the production and distribution of lithium-ion battery packs across Taiwan, the United States, and various international markets, with a market capitalization of NT$18.39 billion.

Operations: Dynapack generates revenue primarily from the production and sales of lithium-ion battery packs, amounting to NT$16.13 billion. The company's financial performance is influenced by its cost structure and market dynamics, with a focus on maintaining competitive pricing in its core markets.

Dynapack International Technology, a promising entity in the electronics sector, has seen its earnings grow by 174% over the past year, significantly outpacing the industry's 4.8%. Despite a decrease in sales to TWD 3.95 billion from TWD 4.57 billion last year for Q2, net income soared to TWD 1.36 billion from TWD 250 million, thanks partly to a one-off gain of NT$1.2 billion impacting recent results. The company’s price-to-earnings ratio stands at an attractive 9.3x compared to the TW market's average of 21.5x, indicating potential undervaluation and investment appeal.

Taking Advantage

- Unlock our comprehensive list of 4699 Undiscovered Gems With Strong Fundamentals by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TPEX:3211

Dynapack International Technology

Manufactures and sells lithium-ion battery packs in Taiwan, the United States, and internationally.

Flawless balance sheet with solid track record and pays a dividend.