Analyzing 3 High Insider Ownership Growth Companies On Chinese Exchange With Up To 76% Earnings Increase

Reviewed by Simply Wall St

Amidst a turbulent week for global markets, Chinese stocks experienced notable declines as concerns over U.S. interest rates overshadowed Beijing's new initiatives to support its struggling housing sector. In this context, analyzing growth companies with high insider ownership on the Chinese exchange becomes particularly intriguing, as these firms may offer unique resilience and potential for growth in challenging economic times.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| KEBODA TECHNOLOGY (SHSE:603786) | 12.8% | 25.1% |

| Suzhou Sunmun Technology (SZSE:300522) | 37.6% | 63.4% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 24.5% |

| Ningbo Deye Technology Group (SHSE:605117) | 24.8% | 28.4% |

| Suzhou Shijing Environmental TechnologyLtd (SZSE:301030) | 22% | 54.9% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 39.8% |

| Anhui Huaheng Biotechnology (SHSE:688639) | 31.5% | 28.4% |

| Fujian Wanchen Biotechnology Group (SZSE:300972) | 15.3% | 75.9% |

| UTour Group (SZSE:002707) | 24% | 33.1% |

| Offcn Education Technology (SZSE:002607) | 26.1% | 65.3% |

Here we highlight a subset of our preferred stocks from the screener.

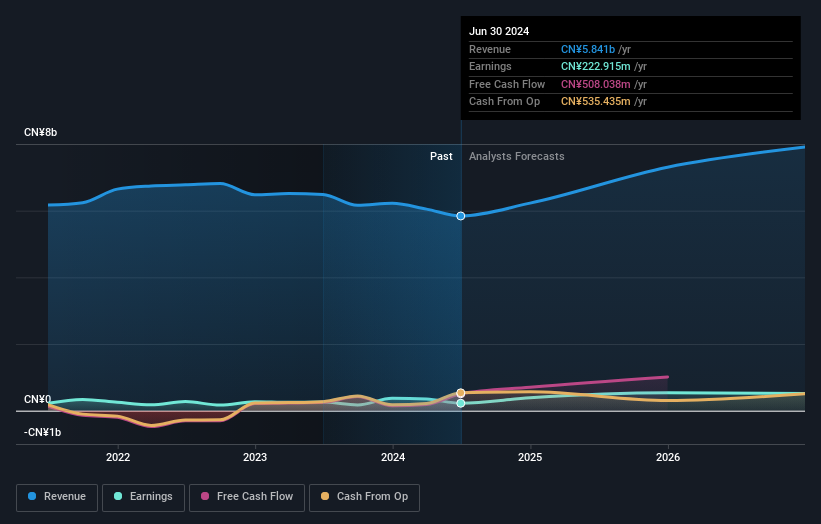

Shenzhen Kingdom Sci-Tech (SHSE:600446)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Shenzhen Kingdom Sci-Tech Co., Ltd. operates in the fintech sector in China and has a market capitalization of approximately CN¥10.41 billion.

Operations: The company generates revenue primarily from its fintech services in China.

Insider Ownership: 29.9%

Earnings Growth Forecast: 28.0% p.a.

Shenzhen Kingdom Sci-Tech, despite a recent downturn in quarterly revenue and profits, shows promising growth prospects. The company's earnings have grown by 39.8% over the past year and are forecasted to increase significantly at 28% annually over the next three years, outpacing the broader Chinese market's growth. Trading at 61.9% below its estimated fair value and with expected revenue growth also above market trends, it presents a compelling case for investors interested in high insider ownership entities. However, recent one-off items have impacted its financial results, suggesting potential volatility in its high-quality earnings claim.

- Unlock comprehensive insights into our analysis of Shenzhen Kingdom Sci-Tech stock in this growth report.

- Upon reviewing our latest valuation report, Shenzhen Kingdom Sci-Tech's share price might be too pessimistic.

Jiangsu Leadmicro Nano-Equipment Technology (SHSE:688147)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Leadmicro Nano-Equipment Technology Ltd specializes in designing, manufacturing, and servicing film deposition and etching equipment, with a market capitalization of approximately CN¥13.66 billion.

Operations: The company generates CN¥1.78 billion from its equipment manufacturing segment.

Insider Ownership: 18.6%

Earnings Growth Forecast: 37.7% p.a.

Jiangsu Leadmicro Nano-Equipment Technology, amidst robust growth metrics, exhibits potential as a growth entity with high insider ownership in China. The company's earnings surged by 418.5% last year and are projected to grow at 37.7% annually over the next three years, significantly outpacing the broader Chinese market. Recent initiatives include a share buyback program where it repurchased shares worth CNY 30.01 million, reflecting confidence from management despite its modest return on equity forecast of 19.8%.

- Click here and access our complete growth analysis report to understand the dynamics of Jiangsu Leadmicro Nano-Equipment Technology.

- The analysis detailed in our Jiangsu Leadmicro Nano-Equipment Technology valuation report hints at an inflated share price compared to its estimated value.

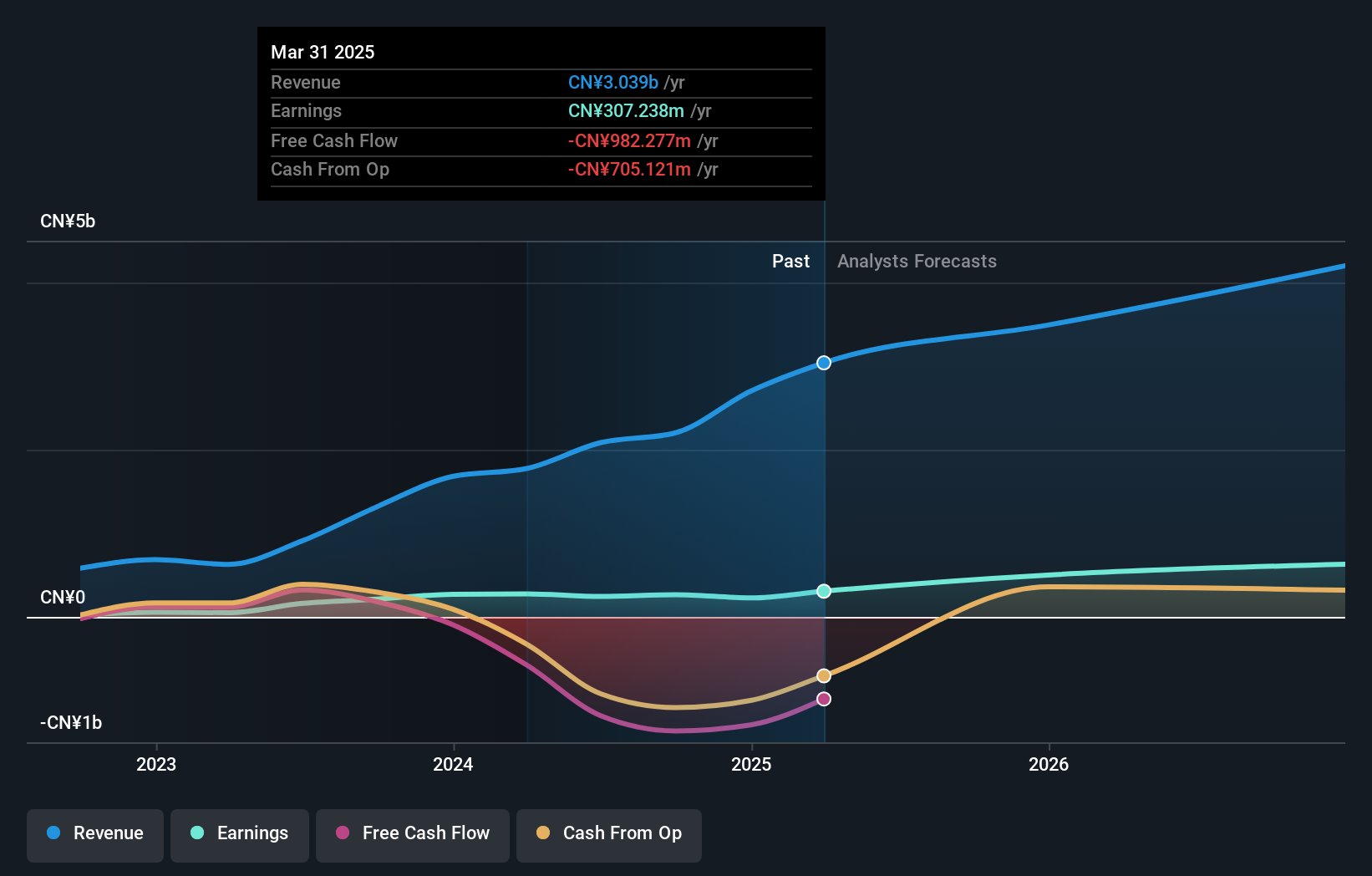

Shenzhen Highpower Technology (SZSE:001283)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen Highpower Technology Co., Ltd. specializes in the research, design, development, manufacture, and sale of lithium-ion and nickel-metal hydride batteries in China, with a market capitalization of approximately CN¥3.97 billion.

Operations: The company generates revenue primarily through the design and production of lithium-ion and nickel-metal hydride batteries.

Insider Ownership: 29.7%

Earnings Growth Forecast: 76.1% p.a.

Shenzhen Highpower Technology, despite its low profit margins of 1.1% down from 3.4% last year, is poised for substantial growth with earnings forecasted to increase by 76.1% annually over the next three years, outstripping the Chinese market's expectations. Recent corporate actions include a dividend increase and amendments to company bylaws, signaling active management and shareholder engagement. However, its dividends are poorly covered by cash flows, indicating potential liquidity concerns in maintaining dividend payouts.

- Delve into the full analysis future growth report here for a deeper understanding of Shenzhen Highpower Technology.

- Our comprehensive valuation report raises the possibility that Shenzhen Highpower Technology is priced higher than what may be justified by its financials.

Key Takeaways

- Get an in-depth perspective on all 403 Fast Growing Chinese Companies With High Insider Ownership by using our screener here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

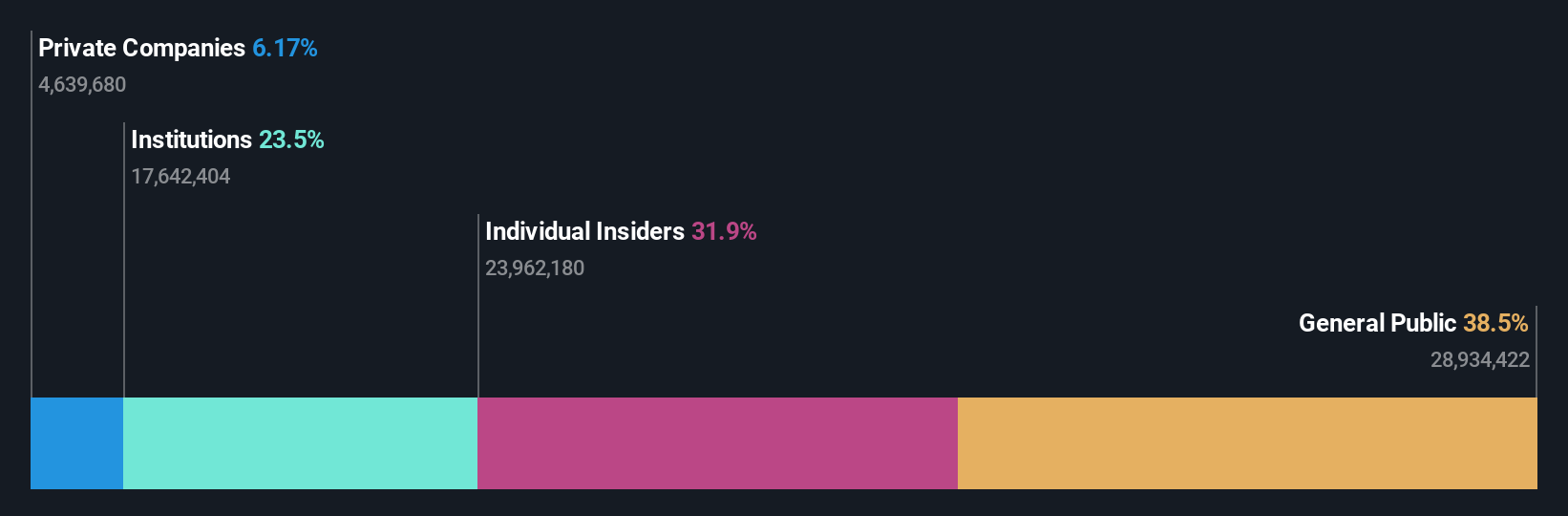

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:600446

Undervalued with excellent balance sheet.