Stock Analysis

- China

- /

- Electronic Equipment and Components

- /

- SHSE:603236

3 High Insider Ownership Growth Companies On Chinese Exchange With Earnings Up To 55% Growth

Reviewed by Simply Wall St

Amidst a backdrop of fluctuating global markets, Chinese equities have shown resilience, buoyed by strong export figures that counterbalance domestic economic pressures. This environment underscores the potential value in exploring growth companies with high insider ownership on Chinese exchanges, which can offer unique advantages in navigating market uncertainties.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| Ningbo Sunrise Elc TechnologyLtd (SZSE:002937) | 24.3% | 27.7% |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 19% | 27.9% |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 24% | 22.3% |

| Anhui Huaheng Biotechnology (SHSE:688639) | 31.4% | 28.4% |

| KEBODA TECHNOLOGY (SHSE:603786) | 12.8% | 25.1% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 25.8% |

| Cubic Sensor and InstrumentLtd (SHSE:688665) | 10.1% | 34.3% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 63.4% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 39.8% |

| UTour Group (SZSE:002707) | 23% | 33.1% |

Here's a peek at a few of the choices from the screener.

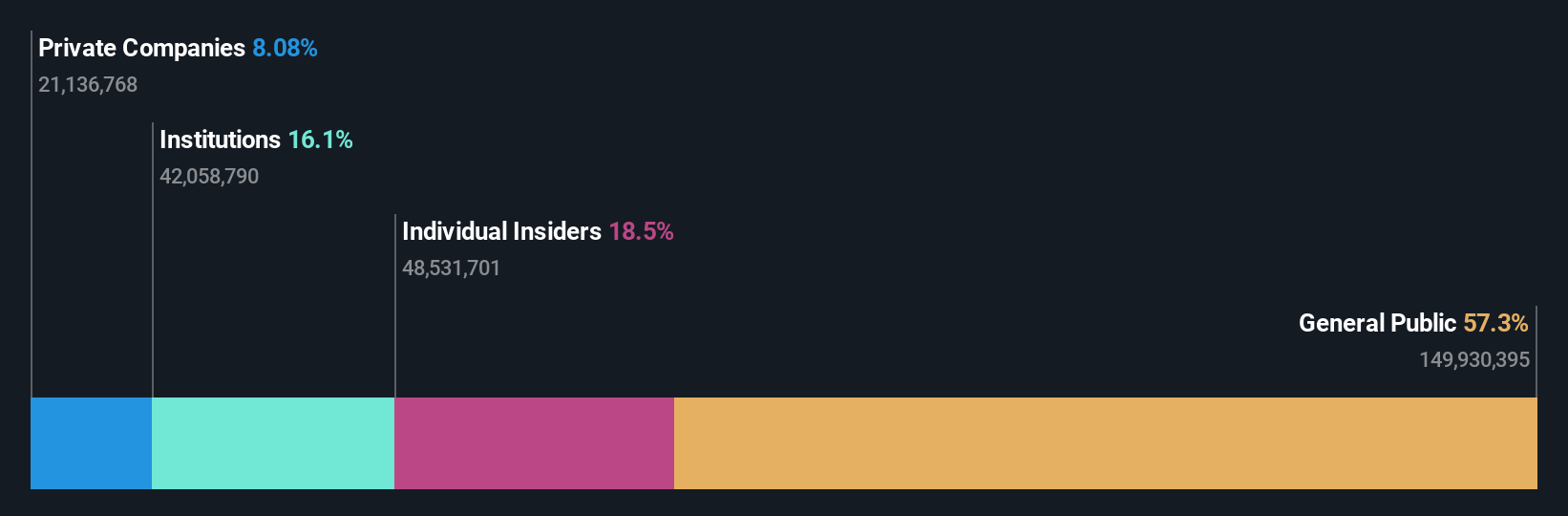

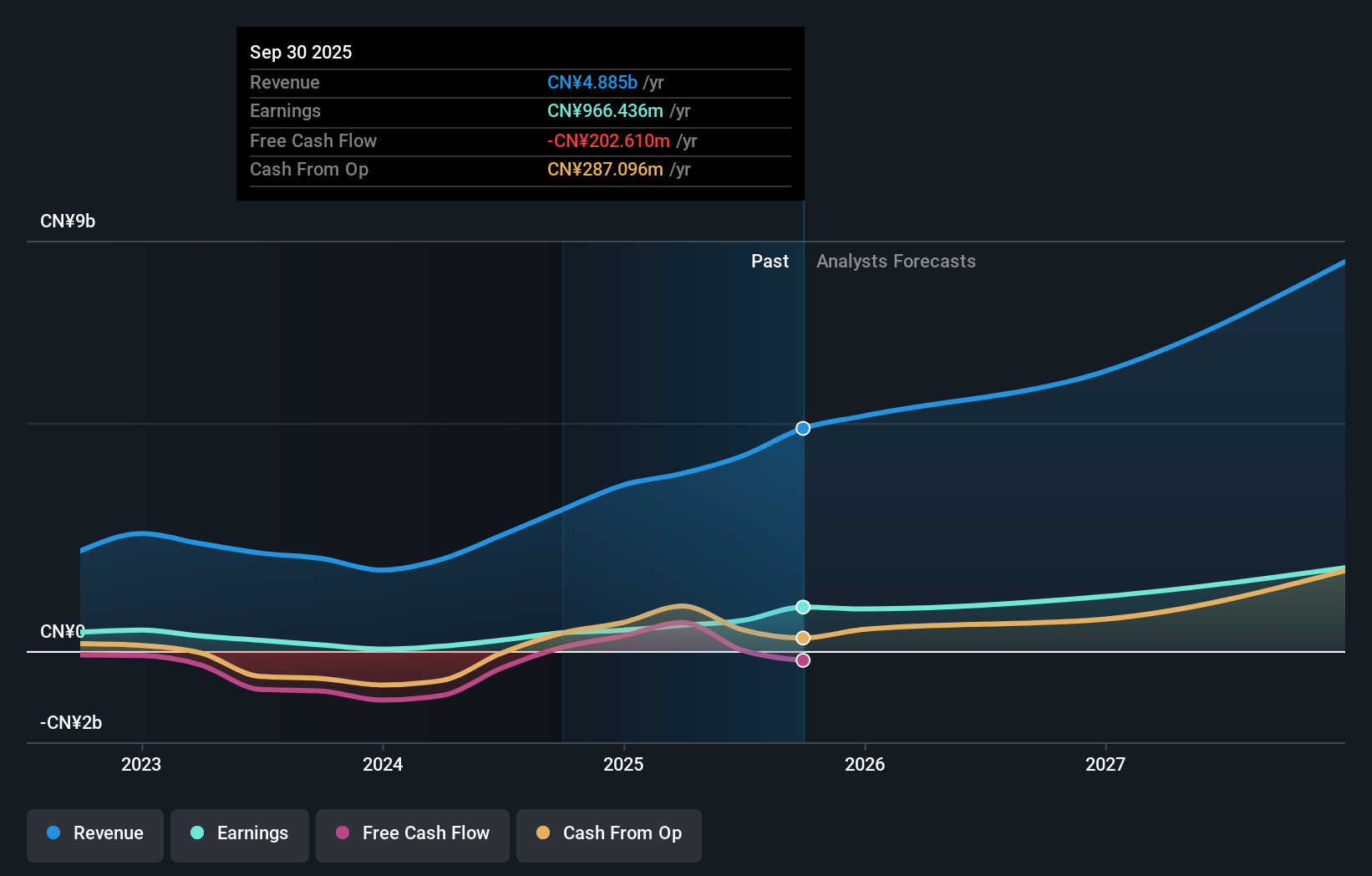

Quectel Wireless Solutions (SHSE:603236)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Quectel Wireless Solutions Co., Ltd. is a global company specializing in the research, development, design, production, and sales of wireless communication modules and solutions, with a market capitalization of approximately CN¥13.37 billion.

Operations: The company generates its revenue primarily from the design, production, and sales of wireless communication modules and solutions globally.

Insider Ownership: 24.4%

Earnings Growth Forecast: 37.8% p.a.

Quectel Wireless Solutions, a key player in the IoT sector, has shown substantial growth with its innovative product launches like the FLM263D Wi-Fi module enhancing smart home connectivity. Despite a challenging market, Quectel's recent earnings report indicates robust recovery with significant revenue and net income improvements. High insider ownership aligns management with shareholder interests, although its forecasted Return on Equity suggests modest future profitability relative to other investments. The firm is trading below its estimated fair value, suggesting potential undervaluation in a growing market.

- Get an in-depth perspective on Quectel Wireless Solutions' performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Quectel Wireless Solutions' share price might be on the cheaper side.

Hangzhou Changchuan TechnologyLtd (SZSE:300604)

Simply Wall St Growth Rating: ★★★★★★

Overview: Hangzhou Changchuan Technology Co., Ltd. focuses on researching, developing, producing, and selling integrated circuit equipment and high-frequency communication materials, with a market capitalization of approximately CN¥20.06 billion.

Operations: The company generates its revenue from the sale of integrated circuit equipment and high-frequency communication materials.

Insider Ownership: 28.4%

Earnings Growth Forecast: 55.3% p.a.

Hangzhou Changchuan Technology Co., Ltd, a Chinese growth company with substantial insider ownership, recently affirmed its dividend and reported a significant turnaround in quarterly earnings from a loss last year to profits this year. Despite challenges like shareholder dilution and lower profit margins compared to the previous year, the company is poised for robust revenue and earnings growth over the next three years. Recent board changes could influence future governance and strategic direction, aligning with long-term growth objectives.

- Navigate through the intricacies of Hangzhou Changchuan TechnologyLtd with our comprehensive analyst estimates report here.

- Our expertly prepared valuation report Hangzhou Changchuan TechnologyLtd implies its share price may be too high.

SG Micro (SZSE:300661)

Simply Wall St Growth Rating: ★★★★★☆

Overview: SG Micro Corp, specializing in the design, marketing, and sale of analog integrated circuits primarily in China, has a market capitalization of approximately CN¥36.86 billion.

Operations: The company generates CN¥2.83 billion in revenue from its integrated circuit industry segment.

Insider Ownership: 32.8%

Earnings Growth Forecast: 41.3% p.a.

SG Micro, a Chinese growth company, is experiencing substantial earnings growth, forecasted at 41.28% annually. However, its profit margins have declined from 22% to 10.8%. Despite this drop, revenue growth is robust at 20.7% yearly, outpacing the national market average of 13.7%. Recent corporate actions include consistent dividend payments and significant changes in governance aimed at bolstering long-term strategies. These factors indicate a focused but challenging path ahead for SG Micro in leveraging insider ownership for growth.

- Click here to discover the nuances of SG Micro with our detailed analytical future growth report.

- Our valuation report here indicates SG Micro may be overvalued.

Make It Happen

- Get an in-depth perspective on all 365 Fast Growing Chinese Companies With High Insider Ownership by using our screener here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Quectel Wireless Solutions is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603236

Quectel Wireless Solutions

Engages in the research and development, design, production, and sales of wireless communication modules and solutions worldwide.

High growth potential with adequate balance sheet.