Advertisement

Is Nanjing Vazyme BiotechLtd (SHSE:688105) Using Debt In A Risky Way?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Nanjing Vazyme Biotech Co.,Ltd (SHSE:688105) does use debt in its business. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Nanjing Vazyme BiotechLtd

How Much Debt Does Nanjing Vazyme BiotechLtd Carry?

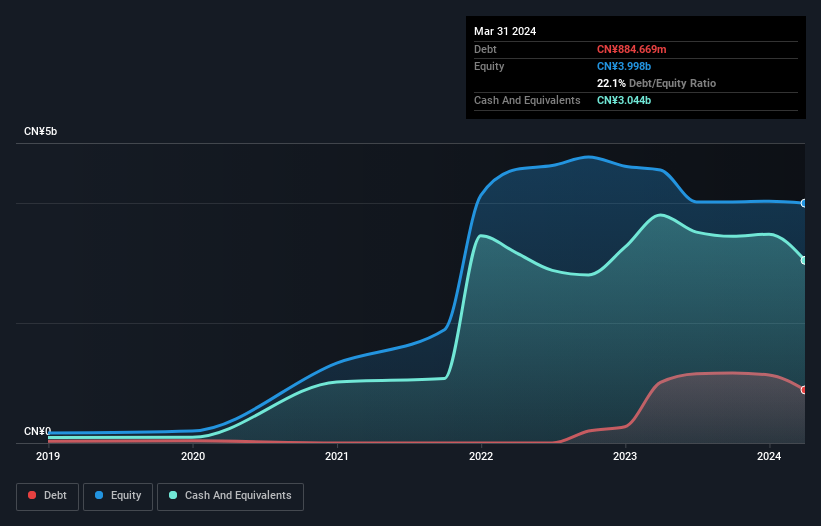

The image below, which you can click on for greater detail, shows that Nanjing Vazyme BiotechLtd had debt of CN¥884.7m at the end of March 2024, a reduction from CN¥1.01b over a year. But it also has CN¥3.04b in cash to offset that, meaning it has CN¥2.16b net cash.

How Strong Is Nanjing Vazyme BiotechLtd's Balance Sheet?

We can see from the most recent balance sheet that Nanjing Vazyme BiotechLtd had liabilities of CN¥1.18b falling due within a year, and liabilities of CN¥234.8m due beyond that. Offsetting this, it had CN¥3.04b in cash and CN¥407.4m in receivables that were due within 12 months. So it can boast CN¥2.04b more liquid assets than total liabilities.

It's good to see that Nanjing Vazyme BiotechLtd has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Simply put, the fact that Nanjing Vazyme BiotechLtd has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Nanjing Vazyme BiotechLtd can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Nanjing Vazyme BiotechLtd made a loss at the EBIT level, and saw its revenue drop to CN¥1.3b, which is a fall of 56%. To be frank that doesn't bode well.

So How Risky Is Nanjing Vazyme BiotechLtd?

Although Nanjing Vazyme BiotechLtd had an earnings before interest and tax (EBIT) loss over the last twelve months, it generated positive free cash flow of CN¥12m. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. We'll feel more comfortable with the stock once EBIT is positive, given the lacklustre revenue growth. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Nanjing Vazyme BiotechLtd's profit, revenue, and operating cashflow have changed over the last few years.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Nanjing Vazyme Biotech might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688105

Nanjing Vazyme Biotech

Offers technology solutions for life science, biomedicine, and in vitro diagnostics.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor