Stock Analysis

- China

- /

- Electronic Equipment and Components

- /

- SHSE:688337

High Insider Ownership Growth Companies On Chinese Exchanges July 2024

Reviewed by Simply Wall St

As of July 2024, Chinese markets have shown resilience, with the Shanghai Composite and CSI 300 indices experiencing gains amid strong export data and easing deflationary pressures. This backdrop provides a promising environment for exploring growth companies with high insider ownership on Chinese exchanges. In such a market context, companies with significant insider ownership can be particularly compelling as these stakeholders often have a vested interest in the company's long-term success, aligning closely with external investors' goals.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| Ningbo Sunrise Elc TechnologyLtd (SZSE:002937) | 24.3% | 27.7% |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 19% | 27.9% |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 24% | 22.3% |

| Anhui Huaheng Biotechnology (SHSE:688639) | 31.4% | 28.4% |

| KEBODA TECHNOLOGY (SHSE:603786) | 12.8% | 25.1% |

| Cubic Sensor and InstrumentLtd (SHSE:688665) | 10.1% | 34.3% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 25.4% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 63.4% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 39.8% |

| UTour Group (SZSE:002707) | 23% | 33.1% |

We're going to check out a few of the best picks from our screener tool.

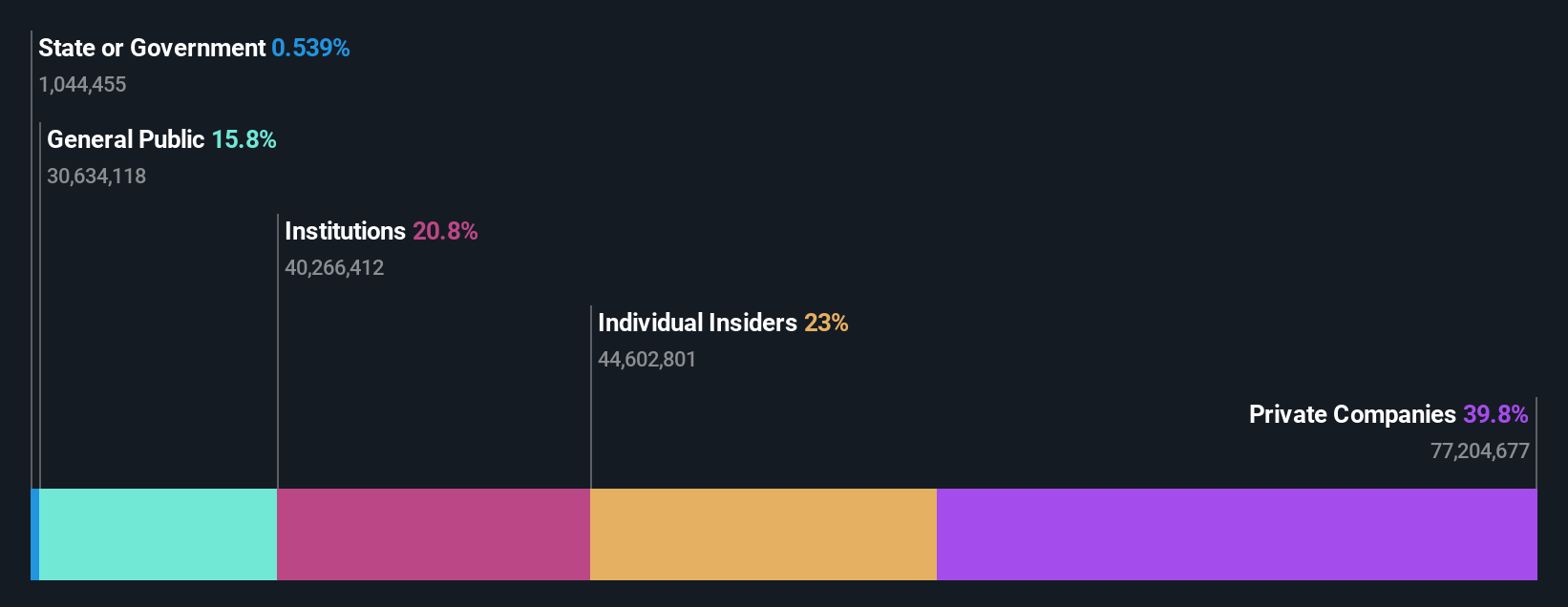

Rigol Technologies (SHSE:688337)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Rigol Technologies Co., Ltd. is a global company that manufactures and sells test and measurement instruments, with a market capitalization of approximately CN¥4.72 billion.

Operations: Rigol Technologies generates revenue primarily through its electronic test and measurement instruments segment, totaling CN¥665 million.

Insider Ownership: 23%

Earnings Growth Forecast: 34.9% p.a.

Rigol Technologies, a company based in China, showcases strong growth potential with forecasted earnings increasing by 34.91% annually and revenue expected to grow at 27.7% per year, outpacing the Chinese market's average. Despite a recent dip in quarterly net income from CNY 23.15 million to CNY 6.31 million, the firm remains under high insider ownership which aligns management’s interests with shareholders'. However, its Return on Equity is projected to be low at 7.1%, and recent shareholder dilution could raise concerns about future value per share.

- Click here and access our complete growth analysis report to understand the dynamics of Rigol Technologies.

- The analysis detailed in our Rigol Technologies valuation report hints at an inflated share price compared to its estimated value.

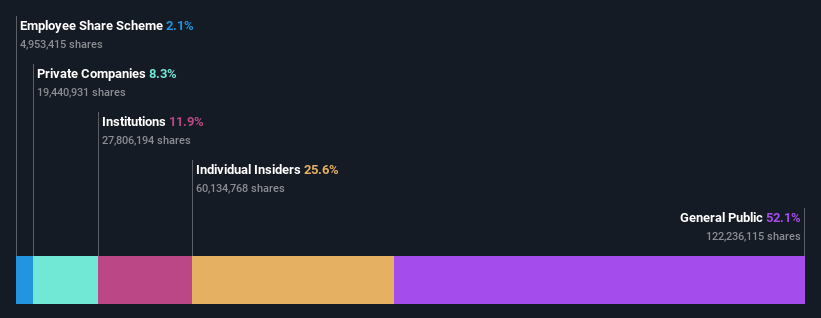

Changzhou Fusion New Material (SHSE:688503)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Changzhou Fusion New Material Co., Ltd. is a company based in China that specializes in the development, production, and sale of various materials such as conductive silver paste and semiconductor materials for the photovoltaic industry, operating both domestically and internationally with a market capitalization of approximately CN¥6.31 billion.

Operations: The company generates its revenue primarily from the sale of electronic components and parts, totaling CN¥11.46 billion.

Insider Ownership: 32.3%

Earnings Growth Forecast: 31.3% p.a.

Changzhou Fusion New Material is positioned as a growth-oriented entity, with its earnings and revenue both forecasted to surpass the Chinese market's average growth rates. Despite trading at 64% below its estimated fair value, indicating potential undervaluation, concerns arise from its low Return on Equity forecast and poor dividend coverage by free cash flows. Recent activities include a share repurchase program aimed at maintaining shareholder value, funded from IPO excesses and internal resources.

- Click to explore a detailed breakdown of our findings in Changzhou Fusion New Material's earnings growth report.

- Our comprehensive valuation report raises the possibility that Changzhou Fusion New Material is priced lower than what may be justified by its financials.

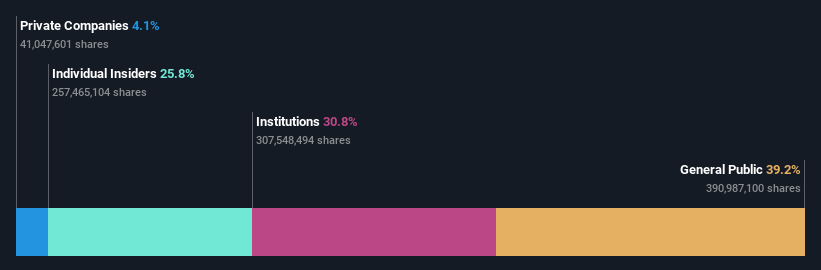

Shandong Sinocera Functional Material (SZSE:300285)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Shandong Sinocera Functional Material Co., Ltd. is a company specializing in the development, production, and sale of functional ceramic materials with a market capitalization of approximately CN¥18.54 billion.

Operations: The revenue segments for the company are not detailed in the provided text.

Insider Ownership: 25.8%

Earnings Growth Forecast: 25% p.a.

Shandong Sinocera Functional Material, trading at 27.2% below its estimated fair value, shows promise with earnings growth of 40.4% last year and an expected annual profit rise of 25% per year, outpacing the Chinese market forecast of 22.2%. However, its revenue growth projection of 17.7% lags behind the desired 20%, and a low forecasted Return on Equity at 12.9% could be concerning. Recent buybacks reflect active management engagement, with CNY10.45 million spent to repurchase shares.

- Get an in-depth perspective on Shandong Sinocera Functional Material's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential undervaluation of Shandong Sinocera Functional Material shares in the market.

Next Steps

- Unlock our comprehensive list of 366 Fast Growing Chinese Companies With High Insider Ownership by clicking here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Rigol Technologies is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688337

Rigol Technologies

Manufactures and sells test and measurement instruments worldwide.

High growth potential with excellent balance sheet.