Huapont Life Sciences Co.,Ltd.'s (SZSE:002004) Has Been On A Rise But Financial Prospects Look Weak: Is The Stock Overpriced?

Huapont Life SciencesLtd (SZSE:002004) has had a great run on the share market with its stock up by a significant 16% over the last three months. We, however wanted to have a closer look at its key financial indicators as the markets usually pay for long-term fundamentals, and in this case, they don't look very promising. Specifically, we decided to study Huapont Life SciencesLtd's ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

See our latest analysis for Huapont Life SciencesLtd

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Huapont Life SciencesLtd is:

2.8% = CN¥455m ÷ CN¥16b (Based on the trailing twelve months to June 2024).

The 'return' is the amount earned after tax over the last twelve months. Another way to think of that is that for every CN¥1 worth of equity, the company was able to earn CN¥0.03 in profit.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

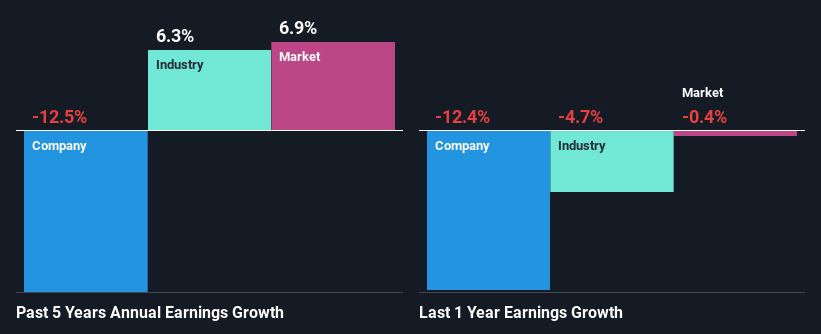

A Side By Side comparison of Huapont Life SciencesLtd's Earnings Growth And 2.8% ROE

As you can see, Huapont Life SciencesLtd's ROE looks pretty weak. Even compared to the average industry ROE of 6.4%, the company's ROE is quite dismal. Therefore, it might not be wrong to say that the five year net income decline of 13% seen by Huapont Life SciencesLtd was possibly a result of it having a lower ROE. We reckon that there could also be other factors at play here. Such as - low earnings retention or poor allocation of capital.

So, as a next step, we compared Huapont Life SciencesLtd's performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 6.3% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Huapont Life SciencesLtd is trading on a high P/E or a low P/E, relative to its industry.

Is Huapont Life SciencesLtd Efficiently Re-investing Its Profits?

Huapont Life SciencesLtd's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 99% (or a retention ratio of 1.4%). With only very little left to reinvest into the business, growth in earnings is far from likely. You can see the 3 risks we have identified for Huapont Life SciencesLtd by visiting our risks dashboard for free on our platform here.

Moreover, Huapont Life SciencesLtd has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth.

Summary

On the whole, Huapont Life SciencesLtd's performance is quite a big let-down. Particularly, its ROE is a huge disappointment, not to mention its lack of proper reinvestment into the business. As a result its earnings growth has also been quite disappointing. So far, we've only made a quick discussion around the company's earnings growth. You can do your own research on Huapont Life SciencesLtd and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

Valuation is complex, but we're here to simplify it.

Discover if Huapont Life SciencesLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002004

Huapont Life SciencesLtd

Engages in the medicine, medical care, agrochemicals, new materials, tourism, and other businesses in China and internationally.

Excellent balance sheet low.