- China

- /

- Electronic Equipment and Components

- /

- SZSE:002436

3 Chinese Growth Stocks With High Insider Ownership And Earnings Growth Up To 45%

Reviewed by Simply Wall St

As Chinese equities rise amid a holiday-shortened week and the Fed's decision to cut interest rates, investors are increasingly looking for opportunities in growth stocks with strong fundamentals. In this context, companies with high insider ownership and significant earnings growth stand out as particularly attractive options.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 18% | 28.7% |

| Jiayou International LogisticsLtd (SHSE:603871) | 22.6% | 24.6% |

| Arctech Solar Holding (SHSE:688408) | 38.6% | 29.9% |

| Western Regions Tourism DevelopmentLtd (SZSE:300859) | 13.9% | 39.2% |

| Quick Intelligent EquipmentLtd (SHSE:603203) | 34.4% | 33.1% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 67.5% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 41.7% |

| UTour Group (SZSE:002707) | 23% | 25.2% |

| BIWIN Storage Technology (SHSE:688525) | 18.8% | 116.8% |

| Offcn Education Technology (SZSE:002607) | 25.1% | 75.7% |

Let's uncover some gems from our specialized screener.

Befar GroupLtd (SHSE:601678)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Befar Group Co., Ltd engages in the production, processing, and sale of organic and inorganic chemical products, primarily caustic soda, both in China and internationally, with a market cap of CN¥6.82 billion.

Operations: The company's revenue from the chemical industry segment amounts to CN¥8.44 billion.

Insider Ownership: 13.3%

Earnings Growth Forecast: 41% p.a.

Befar Group Ltd. demonstrates strong growth potential with forecasted annual earnings growth of 41%, outpacing the Chinese market's average. Despite lower profit margins this year (4% vs. 8.2%), its price-to-earnings ratio (20.9x) remains attractive compared to the market (27.3x). Recent buyback transactions, including a CNY 150 million repurchase program, reflect insider confidence and aim to align stock price with intrinsic value, enhancing shareholder returns despite limited free cash flow coverage for dividends at 1.42%.

- Click here to discover the nuances of Befar GroupLtd with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Befar GroupLtd is priced lower than what may be justified by its financials.

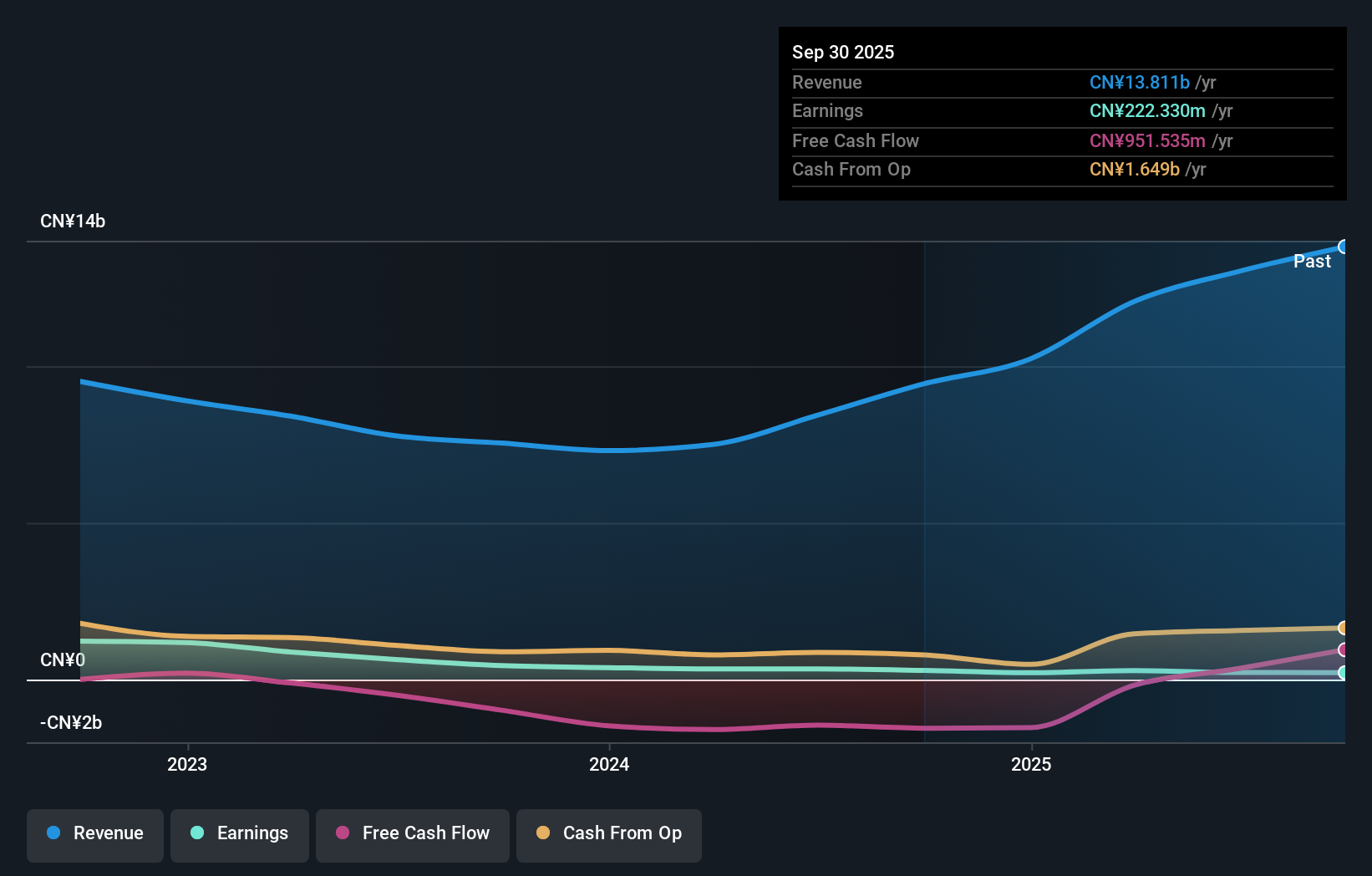

Shenzhen Fastprint Circuit TechLtd (SZSE:002436)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Shenzhen Fastprint Circuit Tech Co., Ltd. manufactures and sells PCBs in China and internationally, with a market cap of CN¥14.43 billion.

Operations: The company's revenue segments include CN¥4.24 billion from PCB Printed Circuit Boards and CN¥1.22 billion from Semiconductor Test Boards.

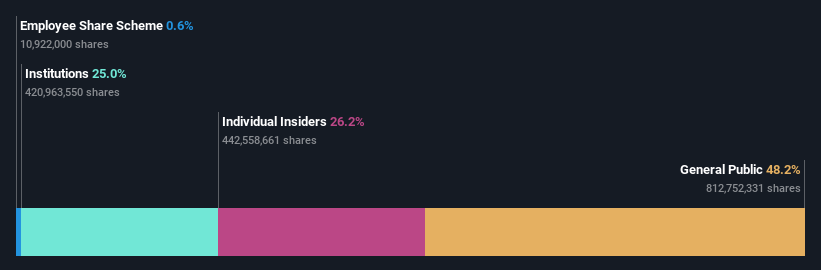

Insider Ownership: 26.2%

Earnings Growth Forecast: 45.6% p.a.

Shenzhen Fastprint Circuit Tech Ltd. shows robust growth prospects with forecasted annual earnings growth of 45.6%, significantly outpacing the Chinese market's 22.9%. Recent half-year sales increased to CNY 2.88 billion, up from CNY 2.57 billion last year, although net income saw modest gains (CNY 19.5 million vs. CNY 18.06 million). While revenue is expected to grow at a slower rate of 18.8% annually, it still surpasses the market average of 13.1%.

- Click here and access our complete growth analysis report to understand the dynamics of Shenzhen Fastprint Circuit TechLtd.

- Our expertly prepared valuation report Shenzhen Fastprint Circuit TechLtd implies its share price may be too high.

Runjian (SZSE:002929)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Runjian Co., Ltd., a communication technology service company in China, focuses on communication network construction and maintenance with a market cap of CN¥7.50 billion.

Operations: Runjian's revenue segments include Computing Power Service (CN¥363.56 million), Energy Network Business (CN¥1.66 billion), Information Network Business (CN¥2.05 billion), and Communication Network Business (CN¥4.58 billion).

Insider Ownership: 32.6%

Earnings Growth Forecast: 30% p.a.

Runjian Co., Ltd. is poised for significant growth with forecasted annual earnings increase of 30%, surpassing the Chinese market's 22.9%. Its revenue is also expected to grow at a robust 20.8% annually, outpacing the market average of 13.1%. Despite recent declines in half-year sales and net income, its price-to-earnings ratio (19.2x) remains below the market average (27.3x). A recent CNY 460 million stake acquisition by Guangdong Shengyue underscores substantial insider interest.

- Click to explore a detailed breakdown of our findings in Runjian's earnings growth report.

- According our valuation report, there's an indication that Runjian's share price might be on the expensive side.

Taking Advantage

- Click here to access our complete index of 384 Fast Growing Chinese Companies With High Insider Ownership.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002436

Shenzhen Fastprint Circuit TechLtd

Manufactures and sells PCBs in China and internationally.

Reasonable growth potential with proven track record.