Stock Analysis

- China

- /

- Metals and Mining

- /

- SHSE:600988

July 2024 Insight Into China's Growth Companies With High Insider Ownership On The SSE

Reviewed by Simply Wall St

Amidst a backdrop of modest gains on the Shanghai Composite Index and a challenging quarter for China's economic growth, investors continue to navigate the complexities of the Chinese market. High insider ownership in growth companies often signals strong confidence from those who know the business best, making such stocks potentially attractive in these uncertain times.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| Ningbo Sunrise Elc TechnologyLtd (SZSE:002937) | 24.3% | 27.7% |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 19% | 27.9% |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 24% | 22.3% |

| Anhui Huaheng Biotechnology (SHSE:688639) | 21.7% | 28.4% |

| Cubic Sensor and InstrumentLtd (SHSE:688665) | 10.1% | 34.3% |

| KEBODA TECHNOLOGY (SHSE:603786) | 12.8% | 25.1% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 25.4% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 63.4% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 39.8% |

| UTour Group (SZSE:002707) | 23% | 33.1% |

Let's dive into some prime choices out of from the screener.

Chifeng Jilong Gold MiningLtd (SHSE:600988)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Chifeng Jilong Gold Mining Co., Ltd. is a company engaged in gold and non-ferrous metal mining, with a market capitalization of approximately CN¥33.44 billion.

Operations: The company generates revenue through its engagement in gold and non-ferrous metal mining.

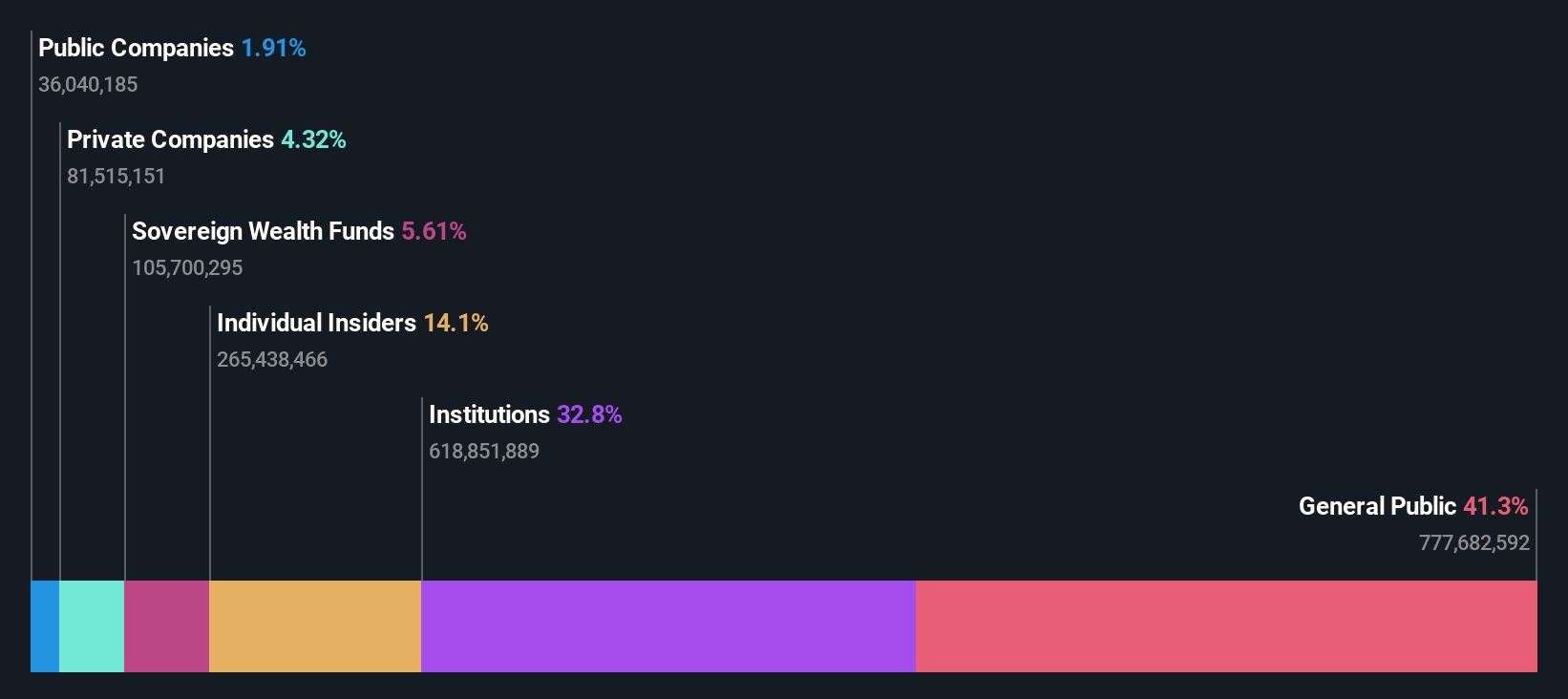

Insider Ownership: 16.1%

Chifeng Jilong Gold Mining Ltd. is experiencing robust growth with earnings up 163.8% over the past year and expected to grow by 25.17% annually. Analysts predict a significant potential price increase of 21.9%, noting the stock trades at a considerable discount, 54.7% below its fair value estimate. Despite slower revenue growth projections at 15.4% compared to some market expectations, insider ownership remains stable with no recent buying or selling reported, underscoring a steady commitment from management amidst ongoing financial improvements and strategic buyback completions totaling CNY 220 million.

- Unlock comprehensive insights into our analysis of Chifeng Jilong Gold MiningLtd stock in this growth report.

- Our valuation report here indicates Chifeng Jilong Gold MiningLtd may be undervalued.

PNC Process Systems (SHSE:603690)

Simply Wall St Growth Rating: ★★★★★☆

Overview: PNC Process Systems Co., Ltd. specializes in researching, developing, producing, and selling semiconductor process equipment, system integration and support equipment, and component materials in China, with a market capitalization of approximately CN¥8.86 billion.

Operations: The company generates its revenue primarily through the sale of semiconductor process equipment, system integration and support equipment, and component materials.

Insider Ownership: 33.9%

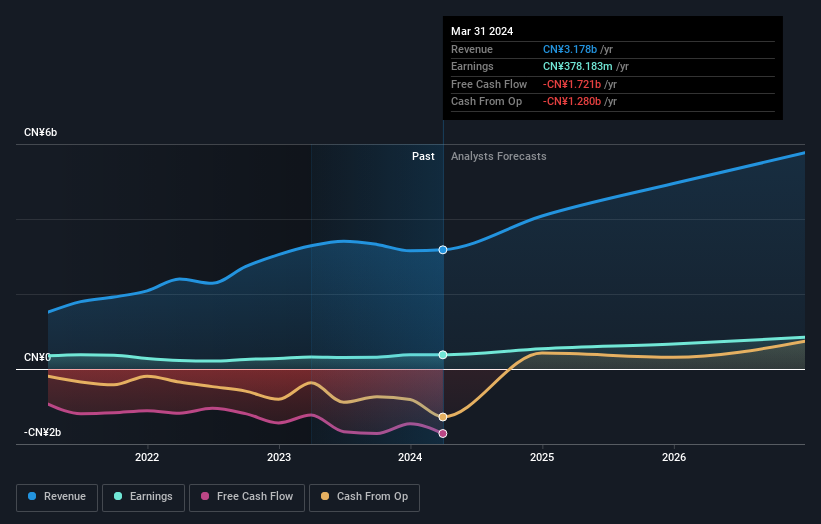

PNC Process Systems, a growth-oriented firm in China with high insider ownership, reported a steady increase in earnings with CNY 377.28 million net income for the full year ended December 31, 2023. Despite challenges in covering debt with operating cash flow and dividends not well supported by free cash flows, the company shows promising forecasts with expected annual revenue and profit growth rates of 20.6% and 27.1%, respectively—outpacing broader market projections. Upcoming shareholder meetings may address these financial dynamics further.

- Click to explore a detailed breakdown of our findings in PNC Process Systems' earnings growth report.

- Our comprehensive valuation report raises the possibility that PNC Process Systems is priced higher than what may be justified by its financials.

Semitronix (SZSE:301095)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Semitronix Corporation specializes in characterization and yield improvement solutions for the semiconductor industry, operating both in China and globally, with a market capitalization of CN¥8.21 billion.

Operations: The company generates revenue through characterization and yield improvement solutions for the semiconductor industry across domestic and international markets.

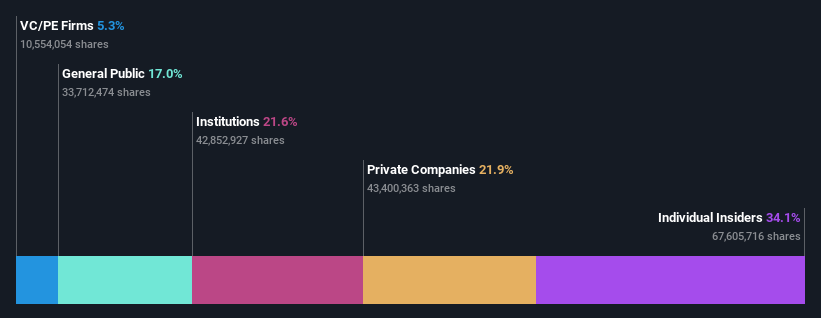

Insider Ownership: 33.8%

Semitronix, a Chinese growth company with high insider ownership, is experiencing strong financial performance with expected revenue and earnings growth of 37.7% and 46.7% per year respectively, significantly outpacing the market averages of 13.7% and 22.2%. However, its Return on Equity is projected to be low at 9.2%, and recent profit margins have declined from last year's figures. The company's dividend coverage by free cash flows remains weak despite a recent increase in dividend payouts approved at their Annual General Meeting on May 9, 2024.

- Click here and access our complete growth analysis report to understand the dynamics of Semitronix.

- According our valuation report, there's an indication that Semitronix's share price might be on the expensive side.

Next Steps

- Get an in-depth perspective on all 367 Fast Growing Chinese Companies With High Insider Ownership by using our screener here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Chifeng Jilong Gold MiningLtd is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:600988

Chifeng Jilong Gold MiningLtd

Operates as a gold and non-ferrous metal mining company.

Solid track record with excellent balance sheet.