- China

- /

- Oil and Gas

- /

- SHSE:601975

Nanjing Tanker (SHSE:601975) sheds 3.3% this week, as yearly returns fall more in line with earnings growth

By buying an index fund, you can roughly match the market return with ease. But many of us dare to dream of bigger returns, and build a portfolio ourselves. For example, the Nanjing Tanker Corporation (SHSE:601975) share price is up 73% in the last three years, clearly besting the market decline of around 24% (not including dividends). On the other hand, the returns haven't been quite so good recently, with shareholders up just 27%.

While this past week has detracted from the company's three-year return, let's look at the recent trends of the underlying business and see if the gains have been in alignment.

View our latest analysis for Nanjing Tanker

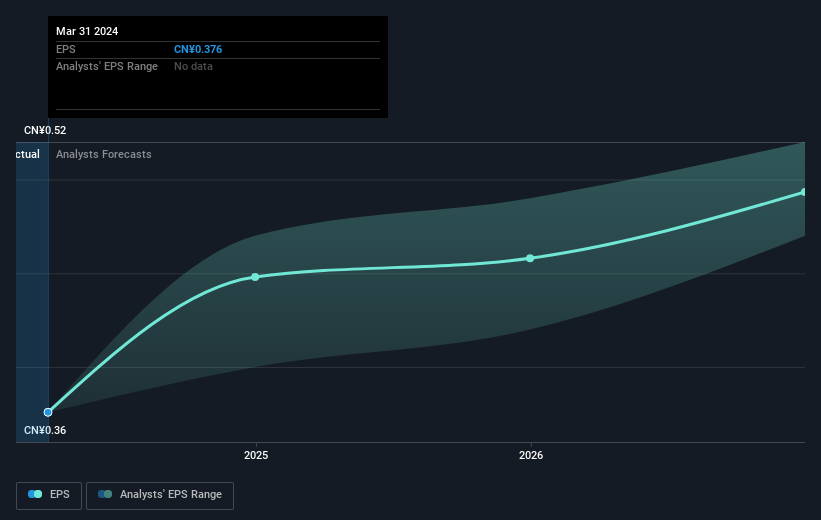

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

Nanjing Tanker was able to grow its EPS at 37% per year over three years, sending the share price higher. This EPS growth is higher than the 20% average annual increase in the share price. So one could reasonably conclude that the market has cooled on the stock. This cautious sentiment is reflected in its (fairly low) P/E ratio of 10.09.

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

It is of course excellent to see how Nanjing Tanker has grown profits over the years, but the future is more important for shareholders. Take a more thorough look at Nanjing Tanker's financial health with this free report on its balance sheet.

A Different Perspective

It's nice to see that Nanjing Tanker shareholders have received a total shareholder return of 27% over the last year. That certainly beats the loss of about 0.7% per year over the last half decade. This makes us a little wary, but the business might have turned around its fortunes. Is Nanjing Tanker cheap compared to other companies? These 3 valuation measures might help you decide.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Nanjing Tanker might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:601975

Nanjing Tanker

Provides oil tanker transportation services in China and internationally.

Flawless balance sheet and undervalued.