Stock Analysis

- China

- /

- Entertainment

- /

- SZSE:300133

Examining 3 Growth Companies With High Insider Ownership And 38% Revenue Growth

Reviewed by Simply Wall St

As global markets navigate through a mixed landscape with ongoing trade tensions and shifting investor focus towards value and small-cap stocks, it's crucial to consider the unique attributes of growth companies with high insider ownership. These firms not only demonstrate confidence from those closest to the core operations but also align well in an environment where discerning investment strategies are paramount for navigating market volatilities and capitalizing on economic recoveries.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Medley (TSE:4480) | 34% | 28.7% |

| Gaming Innovation Group (OB:GIG) | 26.7% | 37.4% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 36.4% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 13.6% | 26.8% |

| KebNi (OM:KEBNI B) | 37.8% | 90.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.5% | 60.9% |

| Calliditas Therapeutics (OM:CALTX) | 11.6% | 52.9% |

| Adocia (ENXTPA:ADOC) | 11.9% | 63% |

| Vow (OB:VOW) | 31.7% | 97.7% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 74.3% |

Below we spotlight a couple of our favorites from our exclusive screener.

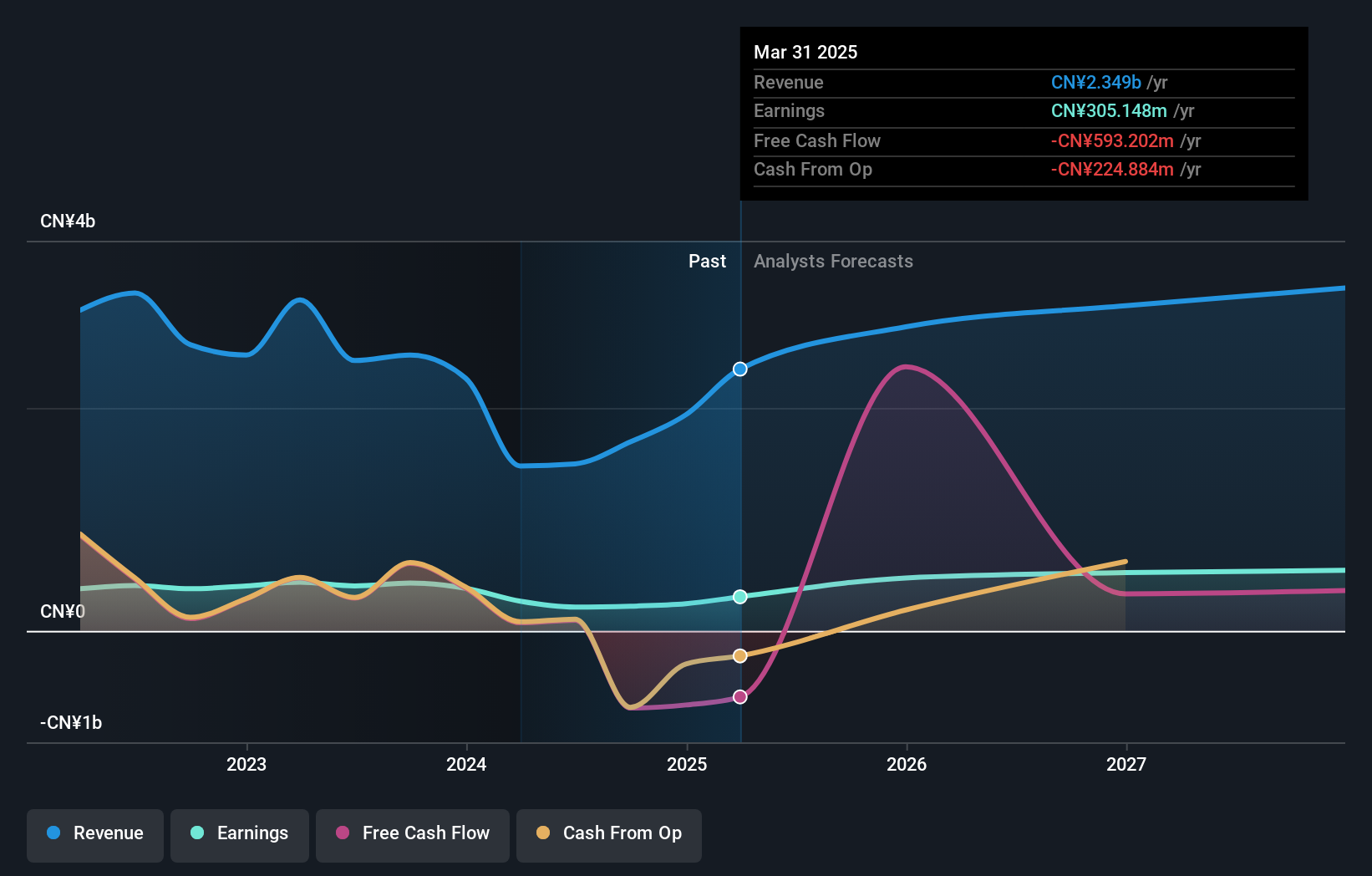

Zhejiang Huace Film & TV (SZSE:300133)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zhejiang Huace Film & TV Co., Ltd. is a company based in China that specializes in the production and distribution of film and television dramas, both domestically and internationally, with a market capitalization of CN¥11.54 billion.

Operations: The company generates revenue primarily through the production and distribution of film and television dramas.

Insider Ownership: 23.2%

Revenue Growth Forecast: 24.5% p.a.

Zhejiang Huace Film & TV is poised for robust growth with earnings and revenue forecasted to outpace the Chinese market significantly, growing at 25.7% and 24.5% per year respectively. Despite this, the company's share price has been highly volatile recently, and its Return on Equity is expected to remain low at 7.3%. Additionally, recent dividend increases indicate a potential commitment to returning value to shareholders amidst this growth phase.

- Click here to discover the nuances of Zhejiang Huace Film & TV with our detailed analytical future growth report.

- Our valuation report here indicates Zhejiang Huace Film & TV may be overvalued.

Jiangsu TongLin ElectricLtd (SZSE:301168)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu TongLin Electric Co., Ltd. specializes in the development and manufacturing of photovoltaic connection systems, power stations, electrical equipment, and industrial automation solutions in China, with a market capitalization of approximately CN¥3.24 billion.

Operations: The company generates revenue primarily from the development and manufacturing of photovoltaic connection systems and power stations, along with electrical equipment and industrial automation solutions.

Insider Ownership: 29.6%

Revenue Growth Forecast: 23.8% p.a.

Jiangsu TongLin Electric Ltd., with its recent executive board reshuffling and share buyback completion, shows a proactive approach in governance and shareholder value. The company's earnings are expected to grow by 30.22% annually, outpacing the Chinese market's 22.1%. Despite a low forecasted Return on Equity of 12.6%, its Price-To-Earnings ratio at 21.7x remains attractive compared to the industry average of 26.9x, indicating potential undervaluation amidst significant revenue growth projections of 23.8% per year.

- Take a closer look at Jiangsu TongLin ElectricLtd's potential here in our earnings growth report.

- Our valuation report unveils the possibility Jiangsu TongLin ElectricLtd's shares may be trading at a discount.

WinWay Technology (TWSE:6515)

Simply Wall St Growth Rating: ★★★★★☆

Overview: WinWay Technology Co., Ltd. is engaged in the design, processing, and sale of optoelectronic product test fixtures, integrated circuit test interfaces, and related components across Taiwan, the Americas, China, Asia, Europe, and Canada with a market capitalization of NT$36.16 billion.

Operations: The company generates revenue primarily through the manufacture and sales of photoelectric product testing tools, totaling NT$3.75 billion.

Insider Ownership: 22.9%

Revenue Growth Forecast: 39% p.a.

WinWay Technology is poised for substantial growth with expected revenue and earnings increases of 39% and 63.6% per year, respectively, outpacing the Taiwan market significantly. Despite this, profit margins have dipped from 21.1% to 13.9%, reflecting some operational challenges amid its rapid expansion. Recent corporate activities include a dividend decrease and amendments to company bylaws, indicating active management engagement but also potential shifts in financial strategy amidst high share price volatility.

- Navigate through the intricacies of WinWay Technology with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that WinWay Technology's share price might be on the expensive side.

Make It Happen

- Access the full spectrum of 1450 Fast Growing Companies With High Insider Ownership by clicking on this link.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Huace Film & TV might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300133

Zhejiang Huace Film & TV

Engages in the production, distribution, and derivative of film and television dramas in China and internationally.

High growth potential with excellent balance sheet.