- China

- /

- Metals and Mining

- /

- SZSE:002182

Top Growth Companies With High Insider Ownership For October 2024

Reviewed by Simply Wall St

As October 2024 unfolds, global markets display a mixed landscape with the S&P 500 and Nasdaq Composite showing notable gains, driven by sectors like utilities and real estate, while European indices benefit from the European Central Bank's rate cuts. In this context of shifting economic indicators and investor sentiment, companies with high insider ownership often attract attention for their potential alignment between management interests and shareholder value.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 41.9% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 30.1% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 27.4% |

| Laopu Gold (SEHK:6181) | 36.4% | 33.2% |

| KebNi (OM:KEBNI B) | 36.3% | 86.1% |

| Findi (ASX:FND) | 35.8% | 64.8% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Let's explore several standout options from the results in the screener.

JiangSu Zhenjiang New Energy Equipment (SHSE:603507)

Simply Wall St Growth Rating: ★★★★★☆

Overview: JiangSu Zhenjiang New Energy Equipment Co., Ltd. operates in the renewable energy sector and has a market cap of CN¥4.66 billion.

Operations: JiangSu Zhenjiang New Energy Equipment Co., Ltd. generates its revenue from various segments within the renewable energy sector.

Insider Ownership: 29.1%

JiangSu Zhenjiang New Energy Equipment demonstrates robust growth potential with earnings forecasted to grow significantly, surpassing the CN market's average. Recent earnings show a substantial increase in net income from CNY 78.18 million to CNY 123.46 million year-over-year, highlighting strong performance. Despite trading at a favorable price-to-earnings ratio of 21.6x compared to the market's 33.5x, its dividend coverage remains weak due to insufficient free cash flow support.

- Get an in-depth perspective on JiangSu Zhenjiang New Energy Equipment's performance by reading our analyst estimates report here.

- The valuation report we've compiled suggests that JiangSu Zhenjiang New Energy Equipment's current price could be quite moderate.

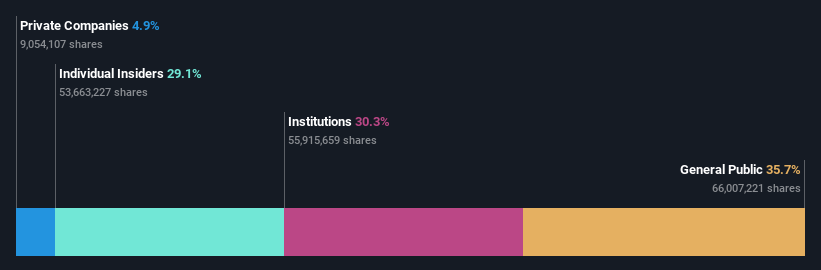

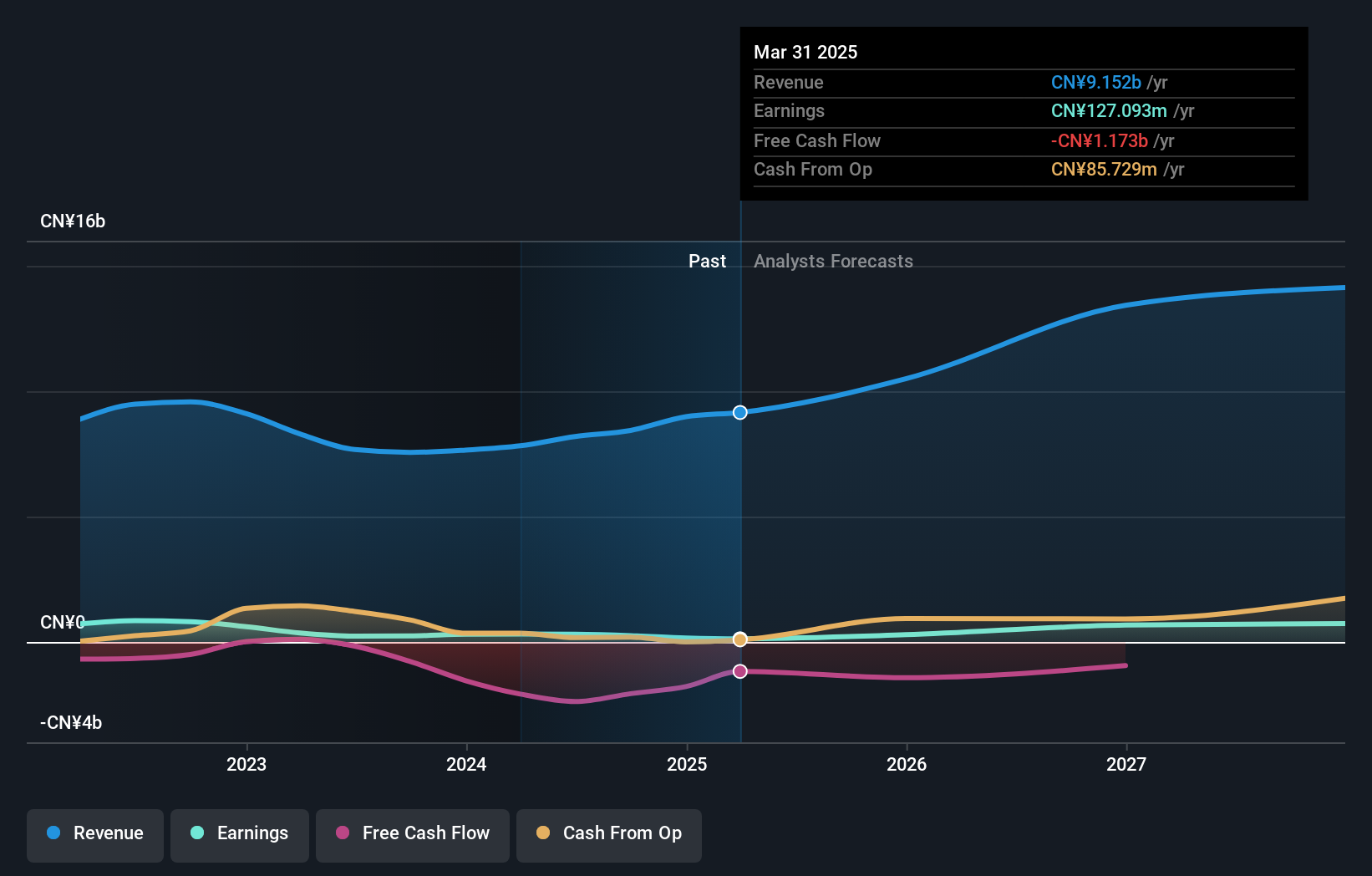

Baowu Magnesium Technology (SZSE:002182)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Baowu Magnesium Technology Co., Ltd. is involved in mining and non-ferrous metal smelting and processing both in China and internationally, with a market cap of CN¥10.96 billion.

Operations: The company's revenue primarily comes from its non-ferrous metal smelting and rolling processing segment, which generated CN¥7.93 billion.

Insider Ownership: 17%

Baowu Magnesium Technology is set for robust growth, with earnings projected to increase significantly, outpacing the CN market's average. Despite a recent dip in net income to CNY 119.79 million from CNY 121.34 million year-over-year, revenue climbed to CNY 4.08 billion. However, its dividend coverage is weak due to inadequate free cash flow support and debt not being well-covered by operating cash flow. Recent company bylaws amendments and private placements indicate strategic shifts underway.

- Click to explore a detailed breakdown of our findings in Baowu Magnesium Technology's earnings growth report.

- Our valuation report here indicates Baowu Magnesium Technology may be overvalued.

Hunan Zhongke Electric (SZSE:300035)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hunan Zhongke Electric Co., Ltd. manufactures electromagnetic metallurgy products in China and has a market cap of CN¥7.26 billion.

Operations: Hunan Zhongke Electric Co., Ltd. generates its revenue through the production and sale of electromagnetic metallurgy products in China.

Insider Ownership: 20.1%

Hunan Zhongke Electric's earnings are expected to grow significantly, surpassing the CN market average. The company recently reported a turnaround in profitability, with net income reaching CNY 69.26 million compared to a loss last year. Revenue growth is projected at 19.6% annually, higher than the market but below 20%. Trading at good value relative to peers and industry, it offers potential despite an unstable dividend history and low future return on equity forecast of 9.3%.

- Navigate through the intricacies of Hunan Zhongke Electric with our comprehensive analyst estimates report here.

- The analysis detailed in our Hunan Zhongke Electric valuation report hints at an deflated share price compared to its estimated value.

Seize The Opportunity

- Dive into all 1486 of the Fast Growing Companies With High Insider Ownership we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Baowu Magnesium Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002182

Baowu Magnesium Technology

Engages in mining and non-ferrous metal smelting, and processing in China and internationally.

High growth potential with adequate balance sheet.