Advertisement

- China

- /

- Auto Components

- /

- SHSE:603197

3 Elite Growth Companies With Strong Insider Ownership

Simply Wall St

Reviewed by Simply Wall St

In a week marked by volatility, global markets have been influenced by competitive pressures in the AI sector and fluctuating corporate earnings, leading to mixed performances across major indices. As investors navigate these uncertain waters, companies with strong insider ownership often stand out due to their alignment of interests between management and shareholders, which can be particularly attractive during turbulent market conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Duc Giang Chemicals Group (HOSE:DGC) | 31.4% | 25.7% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.2% |

| Laopu Gold (SEHK:6181) | 36.4% | 36.4% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 119.4% |

| Brightstar Resources (ASX:BTR) | 16.2% | 86% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Findi (ASX:FND) | 35.8% | 110.7% |

Let's take a closer look at a couple of our picks from the screened companies.

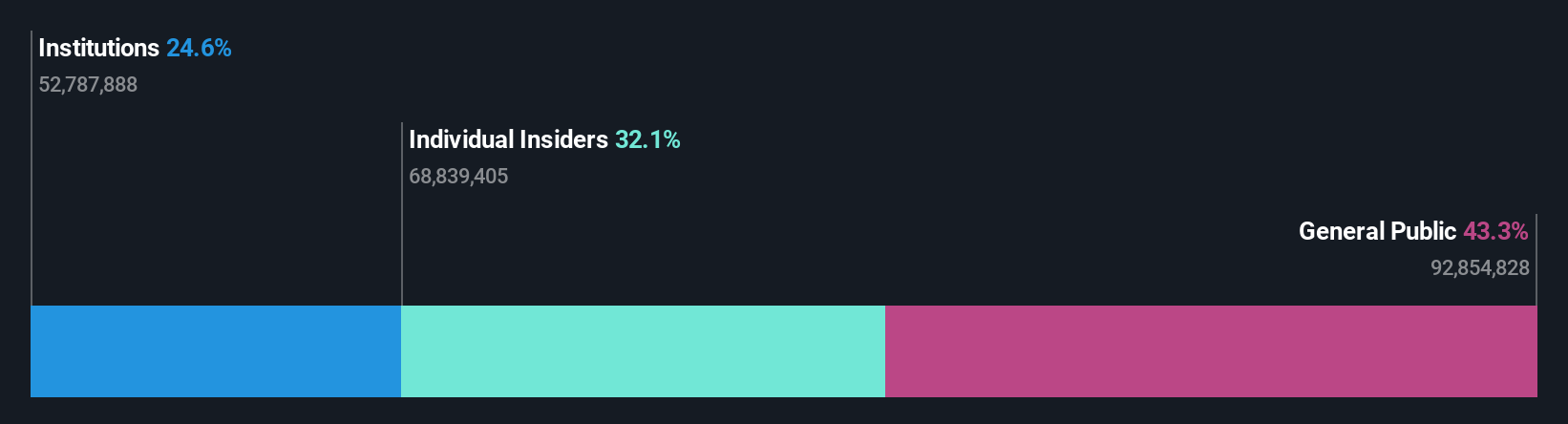

Shenghe Resources Holding (SHSE:600392)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenghe Resources Holding Co., Ltd is involved in the research, development, production, and supply of rare earth products both in China and internationally, with a market capitalization of CN¥18.69 billion.

Operations: Shenghe Resources Holding Co., Ltd generates its revenue through the research, development, production, and supply of rare earth and related products across domestic and international markets.

Insider Ownership: 13.5%

Earnings Growth Forecast: 53.5% p.a.

Shenghe Resources Holding demonstrates promising growth potential, with earnings expected to grow significantly at 53.5% annually, outpacing the CN market's 25.1%. Revenue is also forecasted to rise by 26% per year. Despite high-quality earnings, recent results were impacted by one-off items. Although there is no substantial insider trading activity in the past three months, insider ownership remains a positive indicator for long-term alignment with shareholder interests.

- Delve into the full analysis future growth report here for a deeper understanding of Shenghe Resources Holding.

- According our valuation report, there's an indication that Shenghe Resources Holding's share price might be on the expensive side.

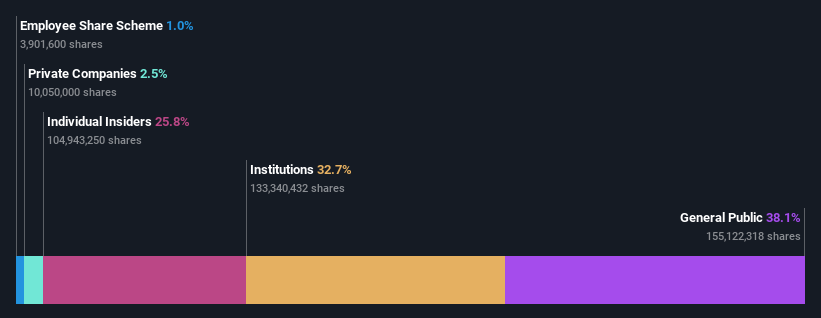

Shanghai Baolong Automotive (SHSE:603197)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai Baolong Automotive Corporation manufactures and sells automotive parts and components, with a market cap of CN¥7.51 billion.

Operations: Revenue Segments (in millions of CN¥):

Insider Ownership: 32.5%

Earnings Growth Forecast: 36.7% p.a.

Shanghai Baolong Automotive is positioned for robust growth, with earnings projected to increase by 36.7% annually, surpassing the CN market's average. Revenue growth is also strong at 23.1% per year. The stock trades at a significant discount to its estimated fair value and is expected to rise by 30.9%. However, profit margins have declined from last year, and operating cash flow does not adequately cover debt obligations, presenting potential financial challenges.

- Click here to discover the nuances of Shanghai Baolong Automotive with our detailed analytical future growth report.

- The analysis detailed in our Shanghai Baolong Automotive valuation report hints at an deflated share price compared to its estimated value.

Xinzhi Group (SZSE:002664)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Xinzhi Group Co., Ltd. is involved in the research, development, manufacturing, and sale of various motors and their core parts both in China and internationally, with a market cap of CN¥5.80 billion.

Operations: The company's revenue primarily comes from its manufacturing segment, which generated CN¥5.81 billion.

Insider Ownership: 25.8%

Earnings Growth Forecast: 65.5% p.a.

Xinzhi Group is poised for substantial growth, with earnings projected to surge by 65.5% annually, well above the CN market average. Revenue is expected to increase at 24.7% per year, outpacing market growth rates. Despite this, return on equity remains low at a forecasted 12.5%, and profit margins have decreased from last year's figures of 5.7% to 2.8%. There has been no significant insider trading activity in recent months.

- Take a closer look at Xinzhi Group's potential here in our earnings growth report.

- Our comprehensive valuation report raises the possibility that Xinzhi Group is priced higher than what may be justified by its financials.

Next Steps

- Get an in-depth perspective on all 1478 Fast Growing Companies With High Insider Ownership by using our screener here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603197

Shanghai Baolong Automotive

Manufactures and sells automotive parts and components.

High growth potential and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor