Advertisement

- Switzerland

- /

- Professional Services

- /

- SWX:SGSN

Analysts Have Made A Financial Statement On SGS SA's (VTX:SGSN) Annual Report

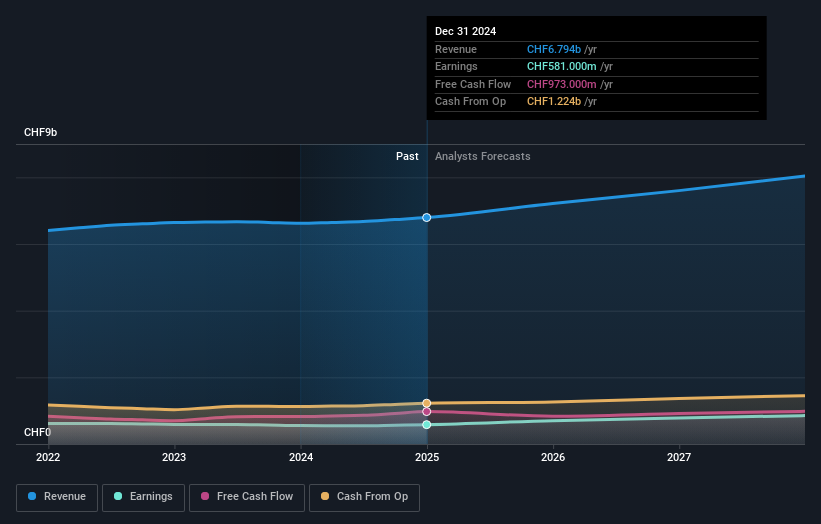

Shareholders of SGS SA (VTX:SGSN) will be pleased this week, given that the stock price is up 11% to CHF98.22 following its latest yearly results. SGS reported in line with analyst predictions, delivering revenues of CHF6.8b and statutory earnings per share of CHF3.09, suggesting the business is executing well and in line with its plan. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for SGS

Following the latest results, SGS' 14 analysts are now forecasting revenues of CHF7.22b in 2025. This would be a modest 6.2% improvement in revenue compared to the last 12 months. Per-share earnings are expected to expand 19% to CHF3.68. Yet prior to the latest earnings, the analysts had been anticipated revenues of CHF7.19b and earnings per share (EPS) of CHF3.67 in 2025. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

The analysts reconfirmed their price target of CHF95.78, showing that the business is executing well and in line with expectations. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values SGS at CHF113 per share, while the most bearish prices it at CHF79.00. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the SGS' past performance and to peers in the same industry. The analysts are definitely expecting SGS' growth to accelerate, with the forecast 6.2% annualised growth to the end of 2025 ranking favourably alongside historical growth of 2.7% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 5.9% annually. SGS is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. Happily, there were no real changes to revenue forecasts, with the business still expected to grow in line with the overall industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on SGS. Long-term earnings power is much more important than next year's profits. We have forecasts for SGS going out to 2027, and you can see them free on our platform here.

You should always think about risks though. Case in point, we've spotted 2 warning signs for SGS you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:SGSN

SGS

Provides inspection, testing, and certification services in Europe, Africa, the Middle East, Latin America, North America, and the Asia Pacific.

Solid track record with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor