While some investors are already well versed in financial metrics (hat tip), this article is for those who would like to learn about Return On Equity (ROE) and why it is important. To keep the lesson grounded in practicality, we'll use ROE to better understand Algonquin Power & Utilities Corp. (TSE:AQN).

Over the last twelve months Algonquin Power & Utilities has recorded a ROE of 8.5%. One way to conceptualize this, is that for each CA$1 of shareholders' equity it has, the company made CA$0.09 in profit.

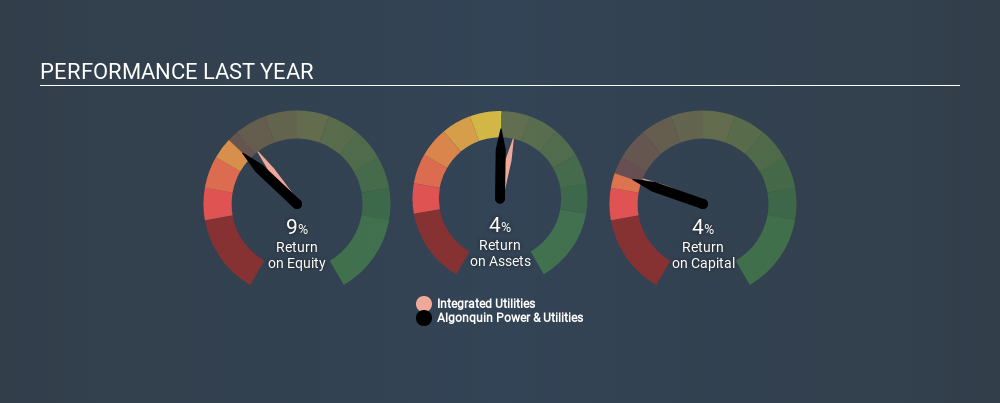

See our latest analysis for Algonquin Power & Utilities

How Do You Calculate ROE?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

Or for Algonquin Power & Utilities:

8.5% = US$366m ÷ US$4.3b (Based on the trailing twelve months to September 2019.)

It's easy to understand the 'net profit' part of that equation, but 'shareholders' equity' requires further explanation. It is the capital paid in by shareholders, plus any retained earnings. You can calculate shareholders' equity by subtracting the company's total liabilities from its total assets.

What Does Return On Equity Signify?

ROE measures a company's profitability against the profit it retains, and any outside investments. The 'return' is the yearly profit. A higher profit will lead to a higher ROE. So, as a general rule, a high ROE is a good thing. That means it can be interesting to compare the ROE of different companies.

Does Algonquin Power & Utilities Have A Good ROE?

By comparing a company's ROE with its industry average, we can get a quick measure of how good it is. Importantly, this is far from a perfect measure, because companies differ significantly within the same industry classification. If you look at the image below, you can see Algonquin Power & Utilities has a similar ROE to the average in the Integrated Utilities industry classification (10%).

That isn't amazing, but it is respectable. ROE doesn't tell us if the share price is low, but it can inform us to the nature of the business. For those looking for a bargain, other factors may be more important. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

The Importance Of Debt To Return On Equity

Companies usually need to invest money to grow their profits. The cash for investment can come from prior year profits (retained earnings), issuing new shares, or borrowing. In the first two cases, the ROE will capture this use of capital to grow. In the latter case, the debt used for growth will improve returns, but won't affect the total equity. Thus the use of debt can improve ROE, albeit along with extra risk in the case of stormy weather, metaphorically speaking.

Combining Algonquin Power & Utilities's Debt And Its 8.5% Return On Equity

It's worth noting the significant use of debt by Algonquin Power & Utilities, leading to its debt to equity ratio of 1.01. The company doesn't have a bad ROE, but it is less than ideal tht it has had to use debt to achieve its returns. Debt increases risk and reduces options for the company in the future, so you generally want to see some good returns from using it.

But It's Just One Metric

Return on equity is one way we can compare the business quality of different companies. In my book the highest quality companies have high return on equity, despite low debt. If two companies have around the same level of debt to equity, and one has a higher ROE, I'd generally prefer the one with higher ROE.

But ROE is just one piece of a bigger puzzle, since high quality businesses often trade on high multiples of earnings. It is important to consider other factors, such as future profit growth -- and how much investment is required going forward. So I think it may be worth checking this free report on analyst forecasts for the company.

If you would prefer check out another company -- one with potentially superior financials -- then do not miss thisfree list of interesting companies, that have HIGH return on equity and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:AQN

Algonquin Power & Utilities

Operates in the power and utility industries in the United States, Canada, and other regions.

Slight with moderate growth potential.