- Canada

- /

- Metals and Mining

- /

- TSXV:SLI

Undiscovered Gems in Canada for October 2024

Reviewed by Simply Wall St

As the Canadian market continues to ride a wave of optimism fueled by recent rate cuts from the U.S. Federal Reserve and enthusiasm around AI, the TSX has reached all-time highs, mirroring gains seen in U.S. indices like the S&P 500. Despite potential volatility from upcoming U.S. elections, investors remain focused on fundamental economic indicators and corporate earnings growth. In this favorable environment, identifying undiscovered gems in Canada's stock market can offer significant opportunities for those looking to capitalize on robust economic conditions and promising sectors.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| TWC Enterprises | 6.74% | 10.99% | 25.68% | ★★★★★★ |

| Mandalay Resources | 11.86% | 9.48% | 37.58% | ★★★★★★ |

| Reconnaissance Energy Africa | NA | 15.28% | 7.58% | ★★★★★★ |

| Taiga Building Products | NA | 6.05% | 10.50% | ★★★★★★ |

| Westshore Terminals Investment | NA | -2.67% | -9.77% | ★★★★★☆ |

| Grown Rogue International | 24.92% | 43.35% | 67.95% | ★★★★★☆ |

| Mako Mining | 22.90% | 38.12% | 54.79% | ★★★★★☆ |

| Queen's Road Capital Investment | 7.20% | 22.14% | 22.20% | ★★★★☆☆ |

| Genesis Land Development | 53.32% | 25.58% | 47.05% | ★★★★☆☆ |

| Dundee | 5.93% | -38.65% | 39.44% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

Extendicare (TSX:EXE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Extendicare Inc., with a market cap of CA$791.27 million, operates through its subsidiaries to provide care and services for seniors in Canada.

Operations: Extendicare generates revenue primarily from Long-Term Care (CA$798.80 million), Home Health Care (CA$525.16 million), and Managed Services (CA$64.32 million).

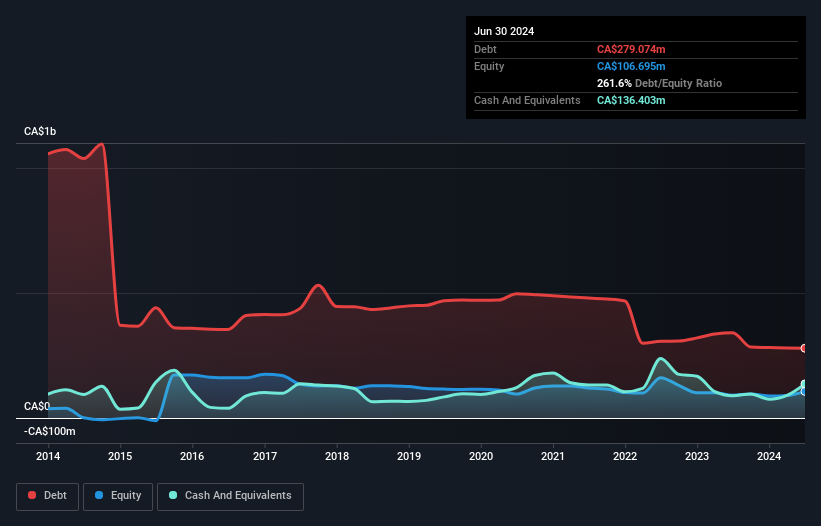

Extendicare's recent performance showcases impressive growth, with earnings surging 3957.1% over the past year, significantly outpacing the Healthcare industry's 8%. The company's net debt to equity ratio stands at a high 133.7%, although it has improved from 405.7% five years ago to 261.6%. With a price-to-earnings ratio of 13.3x, Extendicare trades below the Canadian market average of 15.4x, reflecting good value despite its high debt levels and robust interest coverage (5.9x EBIT).

- Navigate through the intricacies of Extendicare with our comprehensive health report here.

Examine Extendicare's past performance report to understand how it has performed in the past.

North West (TSX:NWC)

Simply Wall St Value Rating: ★★★★★★

Overview: The North West Company Inc., through its subsidiaries, engages in the retail of food and everyday products and services to rural communities and urban neighborhood markets in northern Canada, rural Alaska, the South Pacific, and the Caribbean with a market cap of CA$2.48 billion.

Operations: The North West Company Inc. generated CA$2.52 billion in revenue from retailing food and everyday products and services. The company has a market cap of CA$2.48 billion.

North West's debt to equity ratio has impressively reduced from 96.7% to 43.2% over the past five years, demonstrating improved financial stability. The company's earnings growth of 9.5% in the last year outpaced the Consumer Retailing industry's -11.7%. Trading at 44.8% below its estimated fair value, North West offers significant potential for investors seeking undervalued opportunities. Additionally, with a net debt to equity ratio of 31.4%, it is considered satisfactory and well-covered interest payments by EBIT (10.9x).

- Unlock comprehensive insights into our analysis of North West stock in this health report.

Review our historical performance report to gain insights into North West's's past performance.

Standard Lithium (TSXV:SLI)

Simply Wall St Value Rating: ★★★★★★

Overview: Standard Lithium Ltd. explores, develops, and processes lithium brine properties in the United States with a market cap of CA$387.62 million.

Operations: Standard Lithium Ltd. does not currently generate revenue from its operations, focusing instead on exploration and development activities in the lithium brine sector.

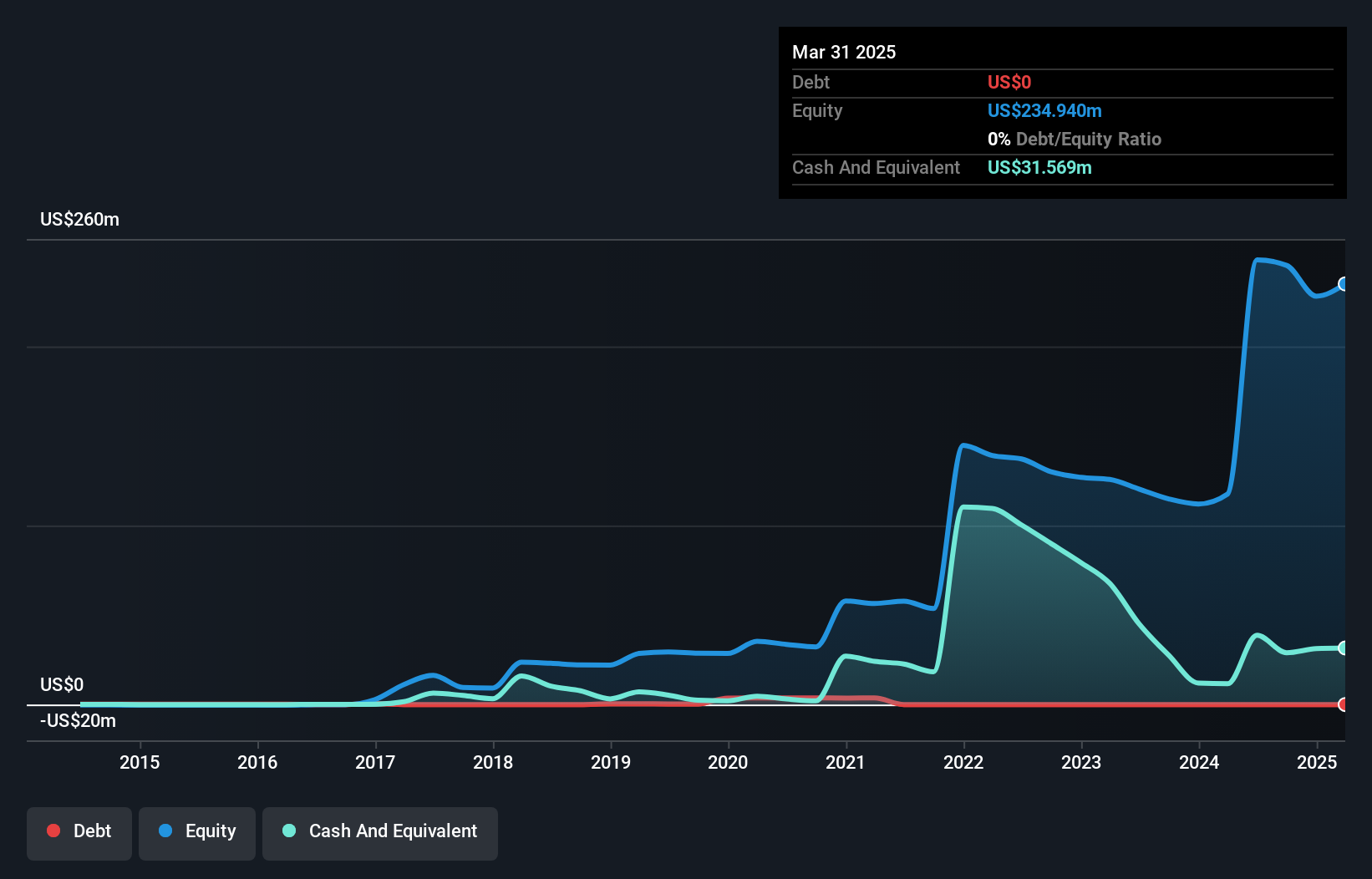

Standard Lithium (SLI) has made significant strides recently, becoming profitable with a net income of CA$147.45 million for the year ending June 30, 2024, compared to a net loss of CA$41.99 million the previous year. The company’s price-to-earnings ratio stands at an attractive 2.6x against the broader Canadian market's 15.4x. Notably, SLI is debt-free and has seen substantial insider selling over the past three months, reflecting some volatility in its share price despite achieving profitability this year.

Turning Ideas Into Actions

- Dive into all 48 of the TSX Undiscovered Gems With Strong Fundamentals we have identified here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSXV:SLI

Standard Lithium

Explores for, develops, and processes lithium brine properties in the United States.

Flawless balance sheet moderate.