Advertisement

- Canada

- /

- Metals and Mining

- /

- TSXV:LMG

Easy Come, Easy Go: How Lincoln Mining (CVE:LMG) Shareholders Got Unlucky And Saw 95% Of Their Cash Evaporate

Some stocks are best avoided. We don't wish catastrophic capital loss on anyone. Anyone who held Lincoln Mining Corporation (CVE:LMG) for five years would be nursing their metaphorical wounds since the share price dropped 95% in that time. We also note that the stock has performed poorly over the last year, with the share price down 50%.

We really feel for shareholders in this scenario. It's a good reminder of the importance of diversification, and it's worth keeping in mind there's more to life than money, anyway.

View our latest analysis for Lincoln Mining

Lincoln Mining hasn't yet reported any revenue yet, so it's as much a business idea as an actual business. This state of affairs suggests that venture capitalists won't provide funds on attractive terms. So it seems that the investors more focused on would could be, than paying attention to the current revenues (or lack thereof). For example, investors may be hoping that Lincoln Mining finds some valuable resources, before it runs out of money.

Companies that lack both meaningful revenue and profits are usually considered high risk. There is almost always a chance they will need to raise more capital, and their progress - and share price - will dictate how dilutive that is to current holders. While some companies like this go on to deliver on their plan, making good money for shareholders, many end in painful losses and eventual de-listing. It certainly is a dangerous place to invest, as Lincoln Mining investors might realise.

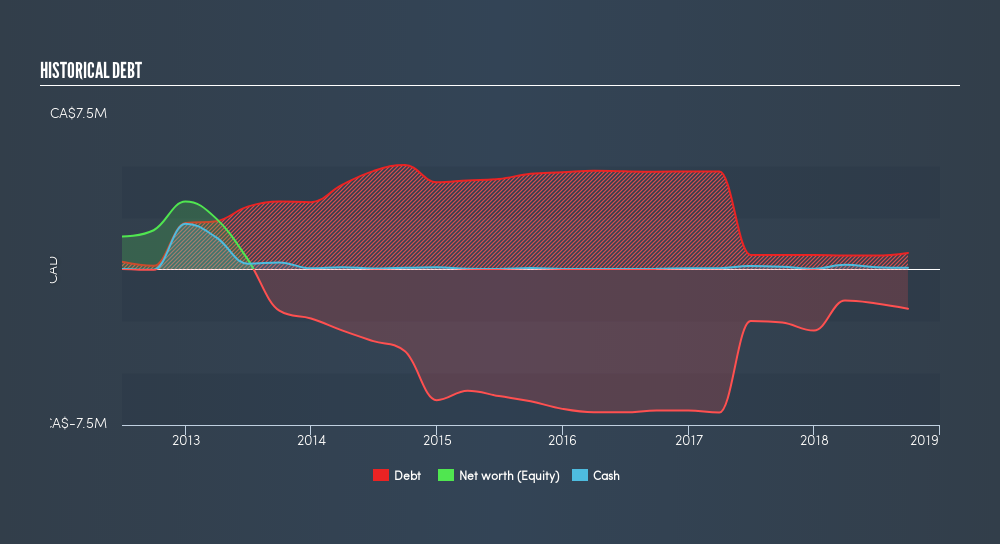

Our data indicates that Lincoln Mining had net debt of CA$2,050,441 when it last reported in September 2018. That puts it in the highest risk category, according to our analysis. But since the share price has dived -45% per year, over 5 years, it looks like some investors think it's time to abandon ship, so to speak. The image below shows how Lincoln Mining's balance sheet has changed over time; if you want to see the precise values, simply click on the image.

In reality it's hard to have much certainty when valuing a business that has neither revenue or profit. Given that situation, would you be concerned if it turned out insiders were relentlessly selling stock? It would bother me, that's for sure. It costs nothing but a moment of your time to see if we are picking up on any insider selling.

A Different Perspective

Investors in Lincoln Mining had a tough year, with a total loss of 50%, against a market gain of about 7.2%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 45% per year over five years. We realise that Buffett has said investors should 'buy when there is blood on the streets', but we caution that investors should first be sure they are buying a high quality businesses. Shareholders might want to examine this detailed historical graph of past earnings, revenue and cash flow.

If you are like me, then you will not want to miss this freelist of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on CA exchanges.We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSXV:LMG

Lincoln Gold Mining

Engages in the exploration and development of precious metals in the United States.

Medium-low risk with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor