Advertisement

Can Methanex's (TSX:MX) Production Surge Offset Lower Methanol Prices in Its Long-Term Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- Methanex Corporation recently reported third quarter 2025 results, highlighting a sharp increase in production to 2,679,000 tonnes and sales volume of 5,544,000 tonnes for the nine months ended September 30, due to integration of the Beaumont and Natgasoline facilities.

- An interesting insight is that despite producing more and generating US$184 million in operating cash flow, Methanex recorded a quarterly net loss and slightly lower sales revenue, reflecting the impact of lower methanol prices and acquisition integration costs.

- We'll explore how this surge in production capacity and management's upbeat EBITDA outlook could influence Methanex's longer-term investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 27 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Methanex Investment Narrative Recap

To own Methanex stock, an investor generally needs to believe in global methanol demand growth, successful integration of recent acquisitions, and management’s ability to unlock cost and operational synergies. The recent surge in production, while impressive, has not materially diminished the company’s primary short-term catalyst, a sustainable rebound in methanol prices. The biggest immediate risk remains cost pressure and execution risk around asset integration rather than any significant shift in market fundamentals due to this news.

The most relevant announcement is the company’s production guidance for 2025, projecting output of roughly 8.0 million tonnes due to the newly integrated assets. This is closely tied to the catalyst of achieving economies of scale and increased operational efficiency, both of which are crucial to offsetting lower methanol prices and buttressing profitability as integration progresses. Such operational milestones feed directly into the near-term investment thesis.

However, despite the positive outlook on production capacity, investors should be aware of persistent risks related to...

Read the full narrative on Methanex (it's free!)

Methanex's narrative projects $4.6 billion in revenue and $421.9 million in earnings by 2028. This requires 6.9% yearly revenue growth and a $257.9 million earnings increase from the current earnings of $164.0 million.

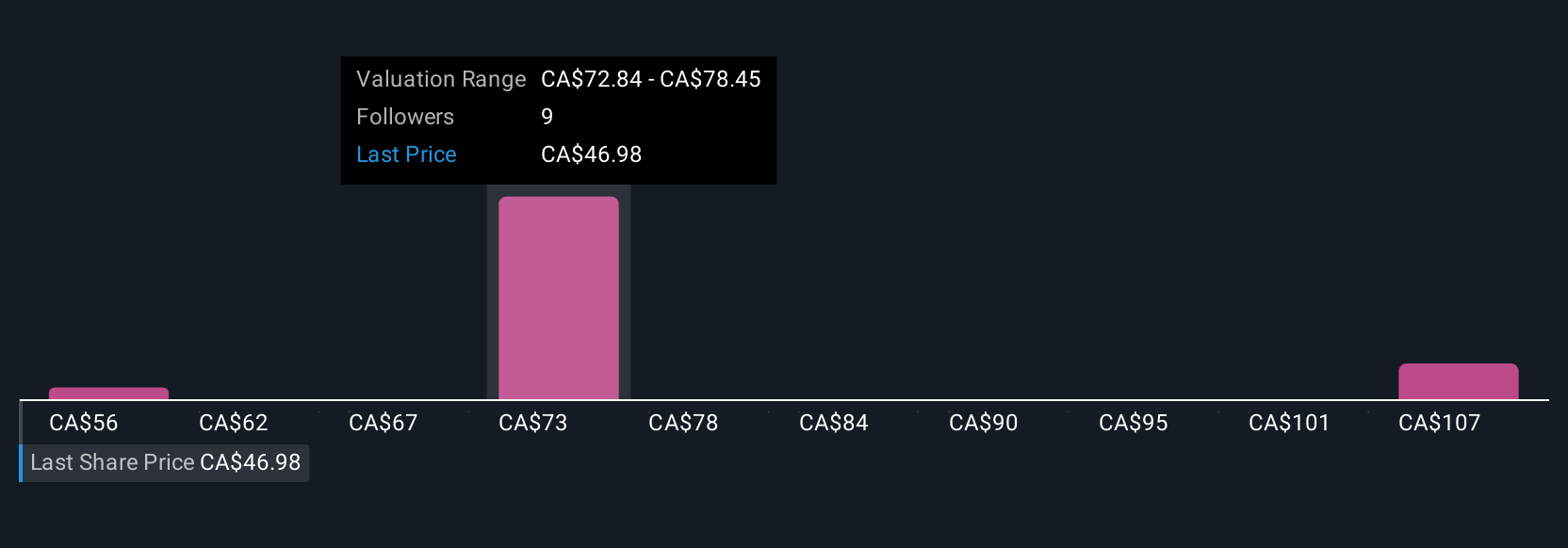

Uncover how Methanex's forecasts yield a CA$75.66 fair value, a 37% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members have posted three fair value estimates for Methanex, ranging from CA$56 to CA$107 per share. With asset integration still presenting key execution risks, you can see how opinions within the market can widely differ depending on individual outlooks and risk tolerance.

Explore 3 other fair value estimates on Methanex - why the stock might be worth as much as 94% more than the current price!

Build Your Own Methanex Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Methanex research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Methanex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Methanex's overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:MX

Methanex

Produces and supplies methanol in Asia Pacific, North America, Europe, and South America.

Undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$26.69|18.6% undervalued

BE

Community Contributor