- Canada

- /

- Hospitality

- /

- TSX:TWC

Discovering Undiscovered Gems in Canada August 2024

Reviewed by Simply Wall St

Over the last 7 days, the Canadian market has dropped 2.8%, with Financials down 3.1% and Materials down 6.7%. However, over the past year, the market has risen by 8.1%, with earnings expected to grow by 15% per annum over the next few years. In this fluctuating environment, identifying promising yet underappreciated stocks can provide unique opportunities for investors looking to capitalize on future growth potential.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Alvopetro Energy | NA | 52.76% | 59.10% | ★★★★★★ |

| TWC Enterprises | 6.74% | 10.99% | 25.68% | ★★★★★★ |

| Taiga Building Products | NA | 7.62% | 15.46% | ★★★★★★ |

| Pizza Pizza Royalty | 15.61% | 2.83% | 3.04% | ★★★★★☆ |

| Frontera Energy | 28.78% | -0.59% | 34.36% | ★★★★★☆ |

| Reconnaissance Energy Africa | NA | 31.73% | -6.92% | ★★★★★☆ |

| Mako Mining | 28.08% | 39.01% | 48.79% | ★★★★★☆ |

| Firan Technology Group | 17.91% | 3.75% | 23.32% | ★★★★★☆ |

| Queen's Road Capital Investment | 7.20% | 22.14% | 22.20% | ★★★★☆☆ |

| Genesis Land Development | 53.32% | 25.58% | 47.05% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

Frontera Energy (TSX:FEC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Frontera Energy Corporation is involved in the exploration, development, production, transportation, storage, and sale of crude oil and natural gas across South America with a market cap of CA$608.53 million.

Operations: Frontera Energy generates revenue primarily from its Exploration and Production Onshore - Colombia segment ($1.11 billion) and also from Infrastructure Colombia ($46.33 million) and Exploration and Production Onshore - Ecuador ($16.95 million).

Frontera Energy, a small-cap oil and gas player, has seen its debt to equity ratio improve from 29.2% to 28.8% over five years while maintaining a net debt to equity ratio of 20.3%. The company’s EBIT covers interest payments 4.9 times over, indicating robust financial health. Despite reporting a net loss of US$2.85 million in Q2 2024, Frontera's earnings grew by 13.4% last year, outpacing the industry average of -35.5%.

- Navigate through the intricacies of Frontera Energy with our comprehensive health report here.

Examine Frontera Energy's past performance report to understand how it has performed in the past.

Lassonde Industries (TSX:LAS.A)

Simply Wall St Value Rating: ★★★★★★

Overview: Lassonde Industries Inc., with a market cap of CA$1.04 billion, develops, manufactures, and markets a range of ready-to-drink beverages, fruit-based snacks, and frozen juice concentrates in Canada, the United States, and internationally.

Operations: Revenue from non-alcoholic beverages for Lassonde Industries Inc. is CA$2.34 billion. The company's net profit margin stands at 5.23%.

Lassonde Industries has shown impressive growth, with earnings surging by 67.7% over the past year, far outpacing the food industry’s 16.7%. The company's debt to equity ratio improved significantly from 48.3% to 16.9% over five years, and its EBIT covers interest payments 9.1 times over, indicating strong financial health. Recent expansions include a $53 million investment in a North Carolina facility, adding new production lines and a distribution center to enhance operational capacity and sustainability.

- Dive into the specifics of Lassonde Industries here with our thorough health report.

Evaluate Lassonde Industries' historical performance by accessing our past performance report.

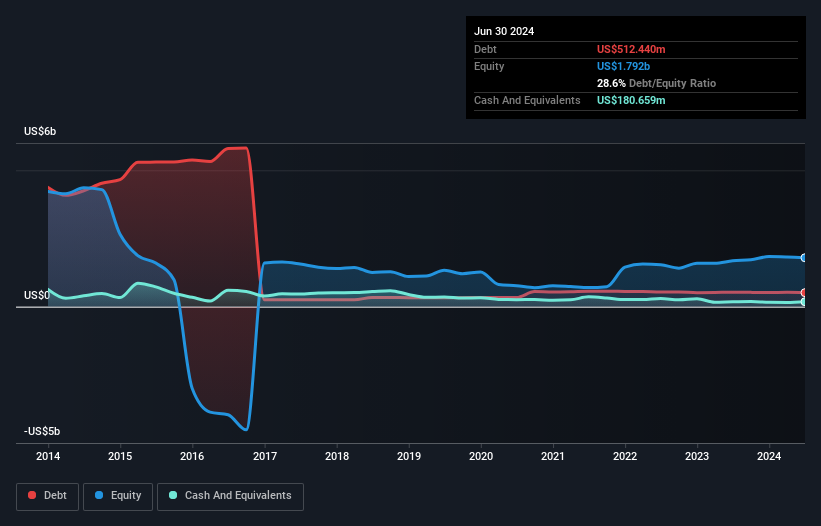

TWC Enterprises (TSX:TWC)

Simply Wall St Value Rating: ★★★★★★

Overview: TWC Enterprises Limited owns, operates, and manages golf clubs under the ClubLink One Membership More Golf brand in Canada and the United States with a market cap of CA$432.99 million.

Operations: TWC Enterprises generates revenue primarily from its Canadian Golf Club Operations (CA$153.17 million) and US Golf Club Operations (CA$23.68 million), with additional income from corporate activities (CA$89.95 million).

TWC Enterprises, a Canadian hospitality player, has seen its earnings grow by 56.1% over the past year, outpacing the industry’s 10.2%. The company trades at a significant discount—75.8% below fair value estimates—and boasts high-quality earnings. Over the last five years, TWC's debt-to-equity ratio improved from 31.3% to 6.7%. Recent results show second-quarter sales of CAD 62.18 million and net income of CAD 3.16 million compared to CAD 8.11 million last year.

- Get an in-depth perspective on TWC Enterprises' performance by reading our health report here.

Review our historical performance report to gain insights into TWC Enterprises''s past performance.

Next Steps

- Navigate through the entire inventory of 43 TSX Undiscovered Gems With Strong Fundamentals here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TWC Enterprises might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TWC

TWC Enterprises

Owns, operates, and manages golf clubs under the ClubLink One Membership More Golf brand in Canada and the United States.

Flawless balance sheet with solid track record.