The board of Bird Construction Inc. (TSE:BDT) has announced that it will pay a dividend of CA$0.033 per share on the 20th of September. The dividend yield will be 4.2% based on this payment which is still above the industry average.

View our latest analysis for Bird Construction

Bird Construction's Payment Has Solid Earnings Coverage

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. However, prior to this announcement, Bird Construction's dividend was comfortably covered by both cash flow and earnings. This means that most of its earnings are being retained to grow the business.

EPS is set to fall by 6.4% over the next 12 months. If the dividend continues along the path it has been on recently, we estimate the payout ratio could be 36%, which is comfortable for the company to continue in the future.

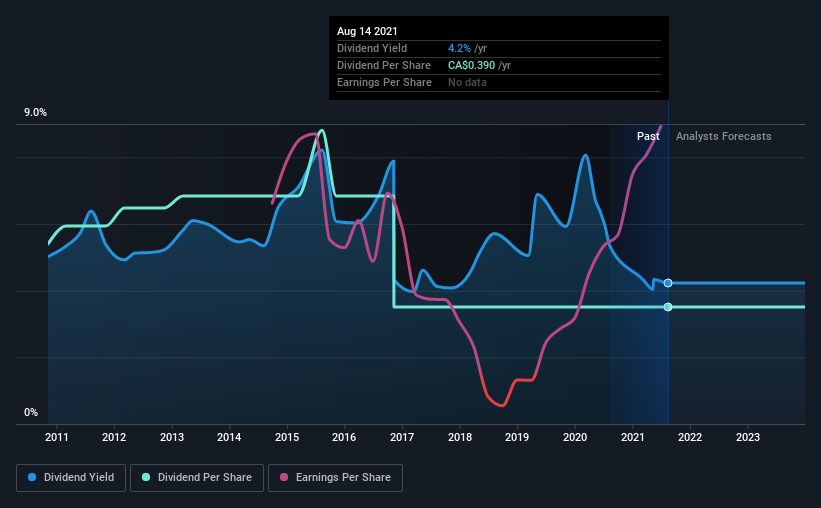

Bird Construction's Track Record Isn't Great

While the company's dividend hasn't been very volatile, it has been decreasing over time, which isn't ideal. Since 2011, the dividend has gone from CA$0.60 to CA$0.39. This works out to be a decline of approximately 4.2% per year over that time. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

The Dividend Looks Likely To Grow

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Bird Construction has seen EPS rising for the last five years, at 17% per annum. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

The company has also been raising capital by issuing stock equal to 25% of shares outstanding in the last 12 months. Regularly doing this can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

We Really Like Bird Construction's Dividend

Overall, we like to see the dividend staying consistent, and we think Bird Construction might even raise payments in the future. The earnings easily cover the company's distributions, and the company is generating plenty of cash. We should point out that the earnings are expected to fall over the next 12 months, which won't be a problem if this doesn't become a trend, but could cause some turbulence in the next year. All in all, this checks a lot of the boxes we look for when choosing an income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we've identified 2 warning signs for Bird Construction that investors need to be conscious of moving forward. We have also put together a list of global stocks with a solid dividend.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bird Construction might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:BDT

Outstanding track record with flawless balance sheet.