Stock Analysis

- Brazil

- /

- Consumer Durables

- /

- BOVESPA:VIVR3

Some Viver Incorporadora e Construtora S.A. (BVMF:VIVR3) Shareholders Look For Exit As Shares Take 30% Pounding

Viver Incorporadora e Construtora S.A. (BVMF:VIVR3) shares have retraced a considerable 30% in the last month, reversing a fair amount of their solid recent performance. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 12% in that time.

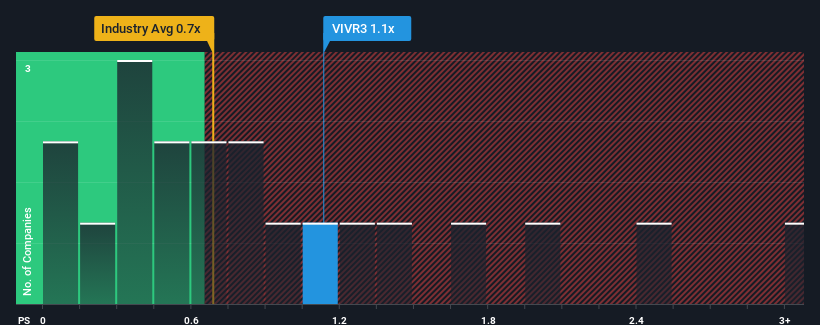

In spite of the heavy fall in price, you could still be forgiven for thinking Viver Incorporadora e Construtora is a stock not worth researching with a price-to-sales ratios (or "P/S") of 1.1x, considering almost half the companies in Brazil's Consumer Durables industry have P/S ratios below 0.6x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Viver Incorporadora e Construtora

How Viver Incorporadora e Construtora Has Been Performing

For example, consider that Viver Incorporadora e Construtora's financial performance has been poor lately as its revenue has been in decline. Perhaps the market believes the company can do enough to outperform the rest of the industry in the near future, which is keeping the P/S ratio high. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Viver Incorporadora e Construtora's earnings, revenue and cash flow.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Viver Incorporadora e Construtora's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 11% decrease to the company's top line. This has erased any of its gains during the last three years, with practically no change in revenue being achieved in total. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Comparing that to the industry, which is predicted to deliver 21% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

In light of this, it's alarming that Viver Incorporadora e Construtora's P/S sits above the majority of other companies. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

What We Can Learn From Viver Incorporadora e Construtora's P/S?

Viver Incorporadora e Construtora's P/S remain high even after its stock plunged. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

The fact that Viver Incorporadora e Construtora currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we see slower than industry revenue growth but an elevated P/S, there's considerable risk of the share price declining, sending the P/S lower. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

You should always think about risks. Case in point, we've spotted 3 warning signs for Viver Incorporadora e Construtora you should be aware of.

If you're unsure about the strength of Viver Incorporadora e Construtora's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're helping make it simple.

Find out whether Viver Incorporadora e Construtora is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:VIVR3

Viver Incorporadora e Construtora

Viver Incorporadora e Construtora S.A. operates as a real estate development company in Brazil.

Worrying balance sheet with weak fundamentals.