Stock Analysis

- Australia

- /

- Construction

- /

- ASX:LYL

Exploring Lycopodium And Two More Undiscovered Australian Gems

Reviewed by Simply Wall St

Over the past year, the Australian market has shown a robust increase of 9.1%, despite remaining flat over the last seven days. In this context, stocks like Lycopodium and two others stand out not only for their potential in earnings growth, which is anticipated to be around 14% per annum, but also for their relatively low profile in the investment community.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Fiducian Group | NA | 9.94% | 6.00% | ★★★★★★ |

| Lycopodium | NA | 15.62% | 29.55% | ★★★★★★ |

| K&S | 15.24% | -1.53% | 26.68% | ★★★★★★ |

| Sugar Terminals | NA | 2.34% | 2.64% | ★★★★★★ |

| Plato Income Maximiser | NA | 11.43% | 14.26% | ★★★★★★ |

| SKS Technologies Group | NA | 31.29% | 43.27% | ★★★★★★ |

| Hearts and Minds Investments | NA | 18.39% | -3.93% | ★★★★★★ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Paragon Care | 340.88% | 28.05% | 68.37% | ★★★★☆☆ |

| Boart Longyear Group | 71.20% | 9.71% | 39.19% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

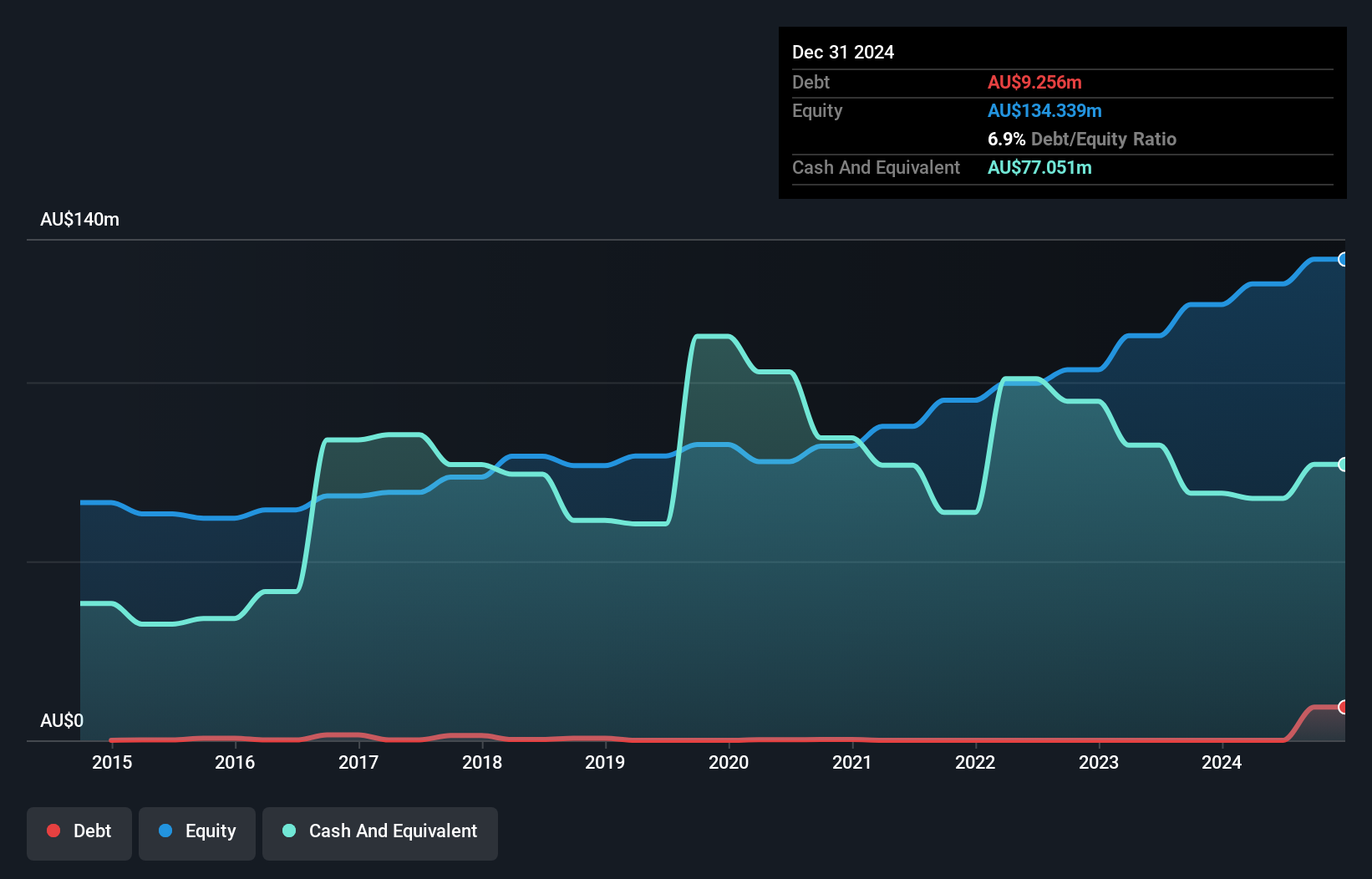

Lycopodium (ASX:LYL)

Simply Wall St Value Rating: ★★★★★★

Overview: Lycopodium Limited is an engineering and project management company specializing in the resources, infrastructure, and industrial processes sectors, with a market capitalization of A$544.44 million.

Operations: Lycopodium operates primarily in the engineering and construction sector, generating revenue through project execution in process industries, which contributed A$11.85 million to its total revenue. The company's business model involves managing costs related to goods sold and operating expenses while achieving a net income margin of 16.73% as of the latest report, reflecting an upward trend over recent years.

Lycopodium, an engineering and project management consultancy, stands out with a 79.9% earnings growth over the past year, surpassing the construction industry's 17.2%. Trading at a 10.3% discount to its estimated fair value, this debt-free company has transitioned from a debt-to-equity ratio of 0.8% five years ago to no debt today, highlighting robust financial health and strategic management. Its strong performance is underpinned by high-quality non-cash earnings, making it a compelling consideration for those looking into lesser-known yet promising Australian stocks.

- Click to explore a detailed breakdown of our findings in Lycopodium's health report.

Examine Lycopodium's past performance report to understand how it has performed in the past.

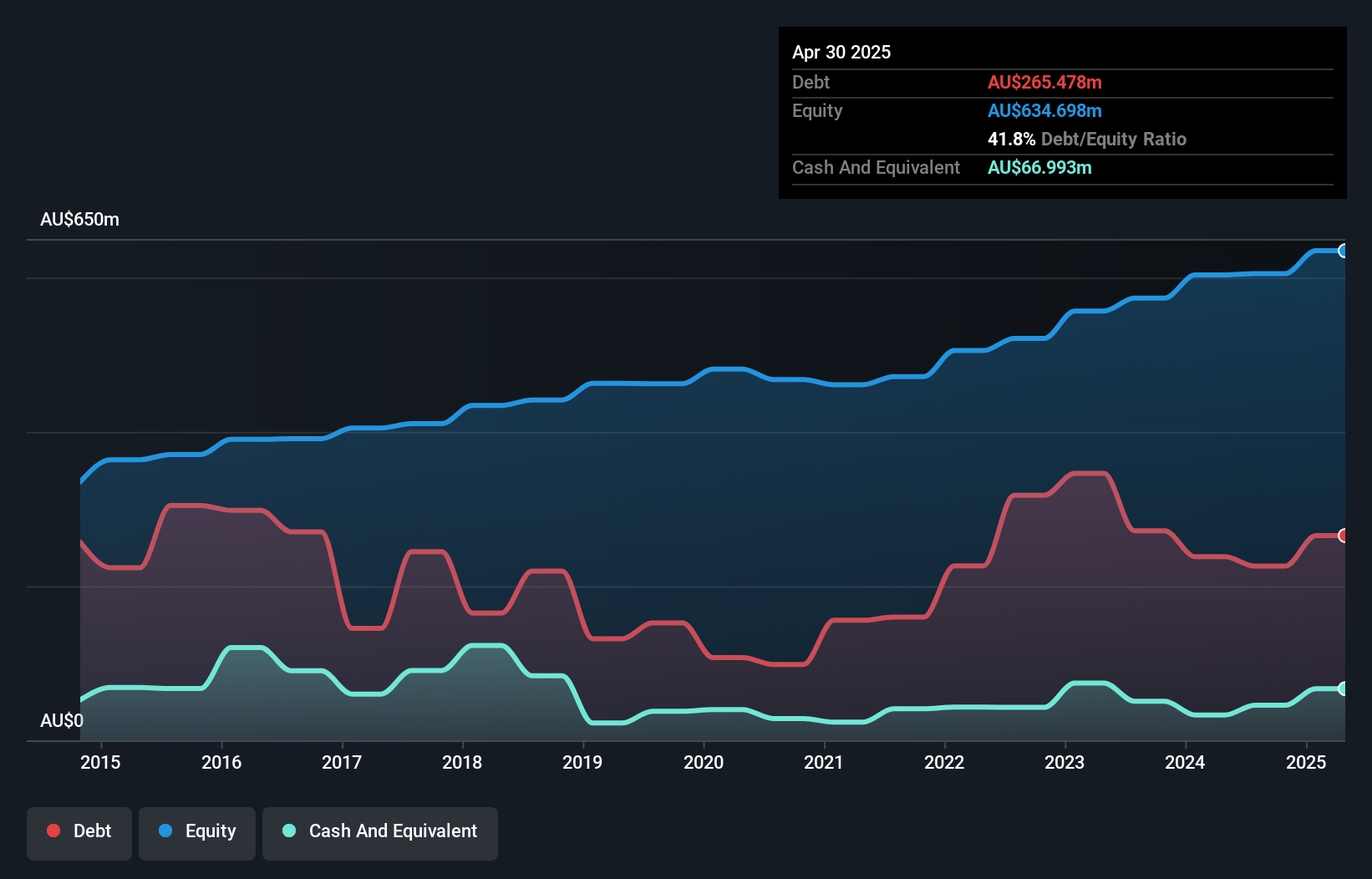

Ricegrowers (ASX:SGLLV)

Simply Wall St Value Rating: ★★★★★☆

Overview: Ricegrowers Limited, trading as SunRice, is a global food business specializing in rice products, with operations spanning Australia, New Zealand, the Pacific Islands, the Middle East, and the United States; it has a market capitalization of A$501.32 million.

Operations: Ricegrowers operates in diverse segments, with International Rice being its largest at A$894.03 million, followed by Rice Pool at A$498.11 million. The company's revenue model benefits significantly from these segments, contributing to a total revenue of A$1.88 billion as of the latest report, showcasing its expansive reach in the global rice market.

Ricegrowers, trading significantly below its estimated fair value, presents an intriguing opportunity. With a robust 20.5% annual profit growth over the past five years and expectations of a 9.78% increase per year moving forward, this entity stands out. Its net debt to equity ratio has risen from 28.5% to 34%, remaining within acceptable bounds. Recently, Ricegrowers reported a notable year with sales reaching A$1.87 billion and net income at A$63 million, up from the previous year’s A$52 million, reflecting strong operational execution and strategic acquisitions focus.

- Click here and access our complete health analysis report to understand the dynamics of Ricegrowers.

Explore historical data to track Ricegrowers' performance over time in our Past section.

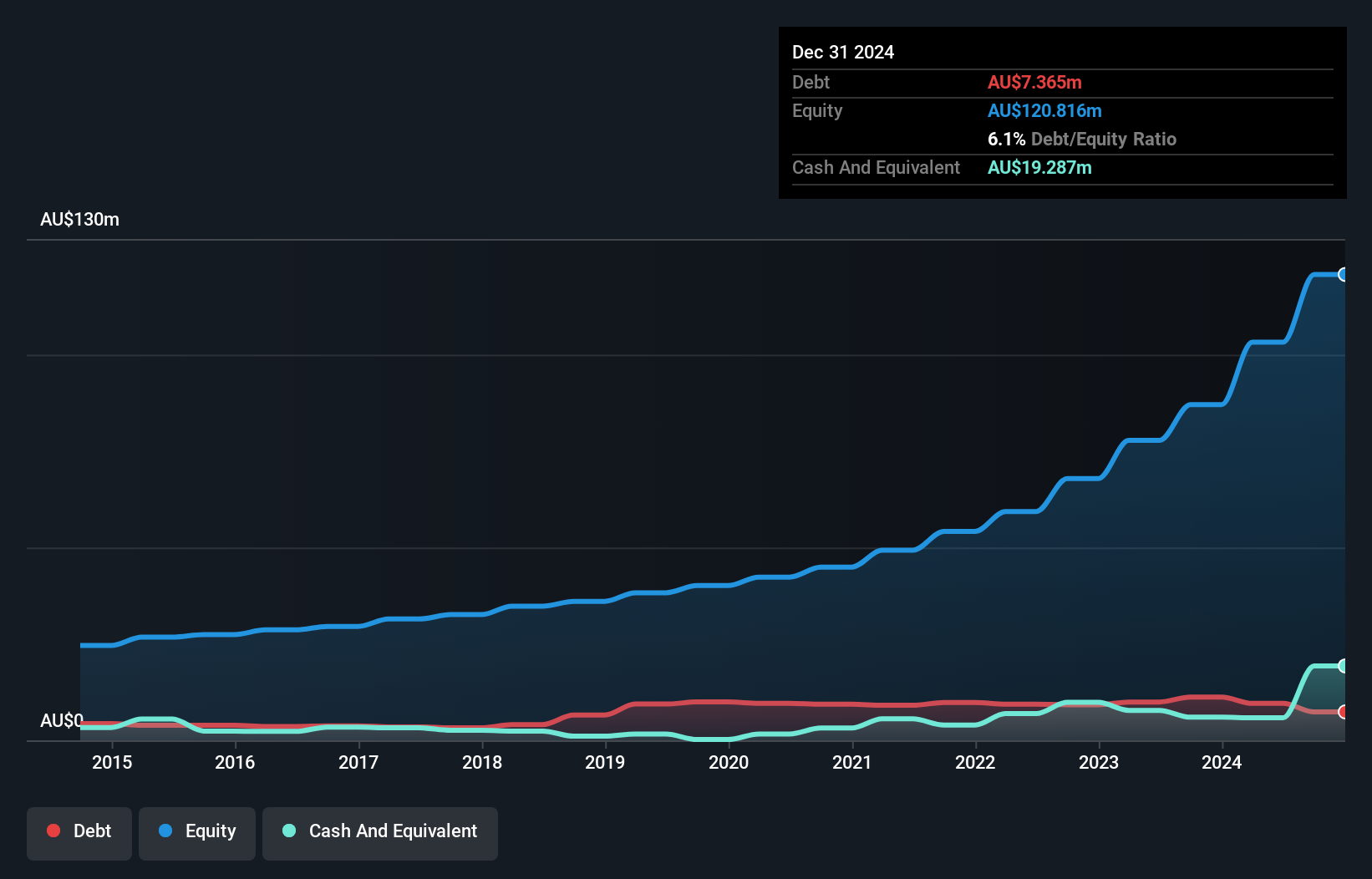

Supply Network (ASX:SNL)

Simply Wall St Value Rating: ★★★★★★

Overview: Supply Network Limited operates in Australia and New Zealand, specializing in the distribution of aftermarket parts for the commercial vehicle industry, with a market capitalization of A$971.27 million.

Operations: This company specializes in providing aftermarket parts for the commercial vehicle market, generating revenue of A$278.41 million as of the latest report. It sustains a gross profit margin around 42%, reflecting its cost management in relation to revenue generated from sales.

Supply Network, an emerging player in the distribution sector, showcases robust growth potential with a 27.9% earnings increase last year, surpassing the industry's modest 2.8%. The company's debt to equity ratio improved significantly from 18.1% to 12.9% over five years, reflecting stronger financial health. With a net debt to equity ratio at a satisfactory 6%, and interest payments well-covered by EBIT (23x), Supply Network is positioned for sustained growth, forecasted at nearly 14% annually.

- Dive into the specifics of Supply Network here with our thorough health report.

Evaluate Supply Network's historical performance by accessing our past performance report.

Make It Happen

- Click through to start exploring the rest of the 47 ASX Undiscovered Gems With Strong Fundamentals now.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Lycopodium is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:LYL

Lycopodium

Provides engineering and project delivery services in the resources, infrastructure, and industrial processes sectors.

Flawless balance sheet with solid track record.