Stock Analysis

- Australia

- /

- Professional Services

- /

- ASX:C79

ASX Growth Companies With High Insider Ownership

Reviewed by Simply Wall St

The ASX200 is set to start the week with a rally, adding about half a percent after Federal Reserve chief Jerome Powell confirmed there’d be interest rate cuts and the threat of war in the Middle East subsided. With US markets responding positively to this news, Australian investors are keenly watching growth companies with high insider ownership as potential opportunities. In such an environment, stocks that demonstrate strong growth potential and significant insider ownership can be particularly appealing. These attributes often signal confidence from those who know the company best, making them worth considering in today’s fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 102.6% |

| Cettire (ASX:CTT) | 28.7% | 26.7% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 13.6% | 27% |

| Acrux (ASX:ACR) | 14.6% | 115.6% |

| Liontown Resources (ASX:LTR) | 16.4% | 69.7% |

| Catalyst Metals (ASX:CYL) | 17.5% | 75.7% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 49.4% |

| Adveritas (ASX:AV1) | 21.1% | 103.9% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| Change Financial (ASX:CCA) | 26.6% | 77.9% |

Let's dive into some prime choices out of the screener.

Accent Group (ASX:AX1)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Accent Group Limited (ASX:AX1) operates in the retail, distribution, and franchise sectors for lifestyle footwear, apparel, and accessories across Australia and New Zealand with a market cap of A$1.15 billion.

Operations: Accent Group's revenue segments include retail, distribution, and franchise operations for lifestyle footwear, apparel, and accessories across Australia and New Zealand.

Insider Ownership: 32.8%

Earnings Growth Forecast: 15.1% p.a.

Accent Group, a growth company with high insider ownership in Australia, is forecast to grow its revenue at 6.4% per year and earnings at 15.1% per year, outpacing the broader Australian market. However, recent financial results show a decline in net income from A$88.65 million to A$59.53 million and reduced profit margins from 6.2% to 4.1%. Despite trading significantly below its estimated fair value, its dividend of 6.34% is not well covered by earnings.

- Dive into the specifics of Accent Group here with our thorough growth forecast report.

- Our valuation report unveils the possibility Accent Group's shares may be trading at a discount.

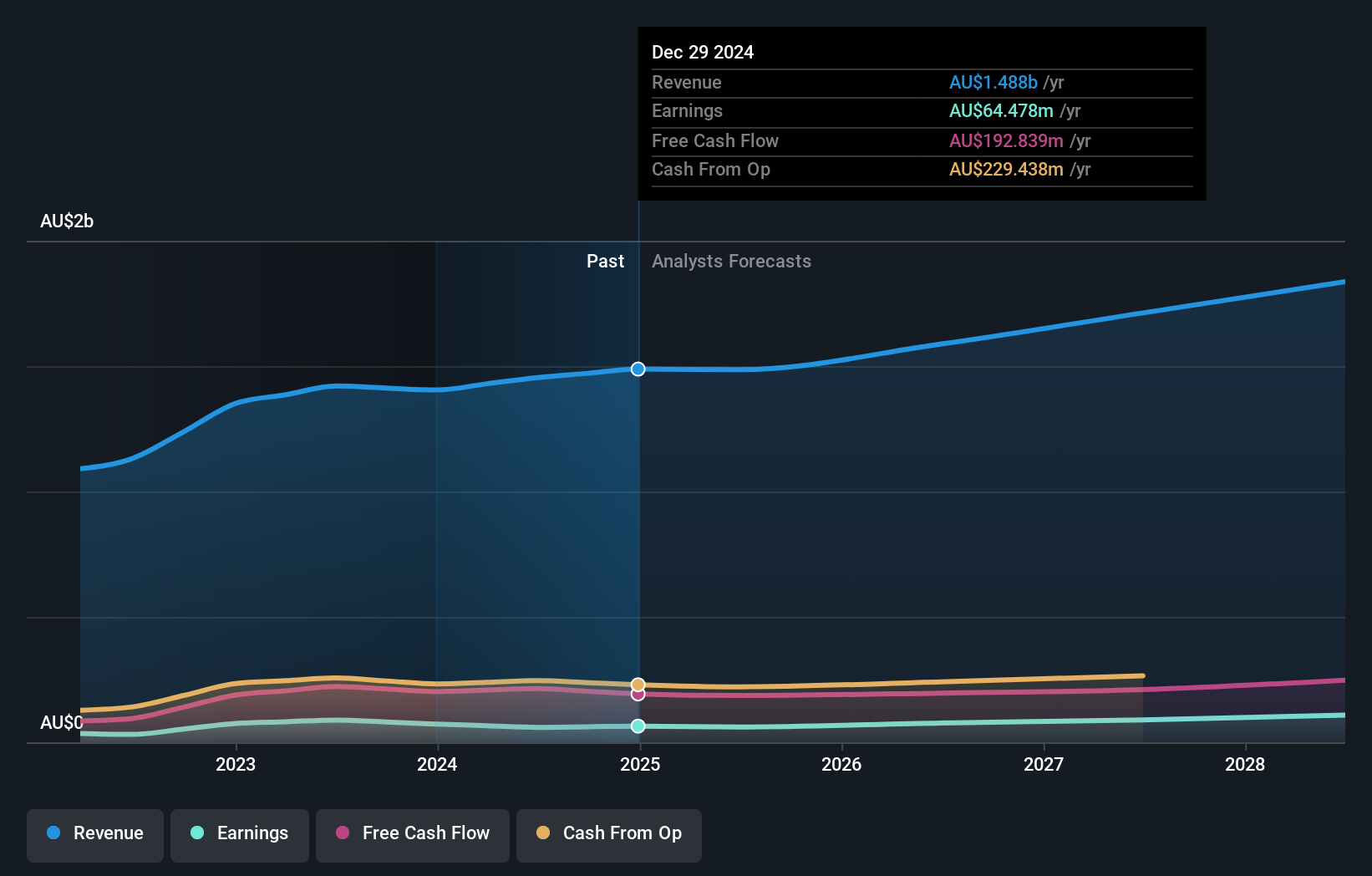

Chrysos (ASX:C79)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Chrysos Corporation Limited, with a market cap of A$607.22 million, develops and supplies mining technology.

Operations: Chrysos generates revenue of A$34.24 million from its mining services segment.

Insider Ownership: 17.5%

Earnings Growth Forecast: 62.4% p.a.

Chrysos Corporation, with substantial insider ownership, is forecast to grow its revenue at 33.1% per year and become profitable within the next three years. Despite recent shareholder dilution, insiders have bought more shares than sold in the past three months. The company's Return on Equity is expected to be low at 5.9% in three years. For fiscal year 2025, Chrysos anticipates total revenue between A$60 million and A$70 million.

- Click here and access our complete growth analysis report to understand the dynamics of Chrysos.

- In light of our recent valuation report, it seems possible that Chrysos is trading beyond its estimated value.

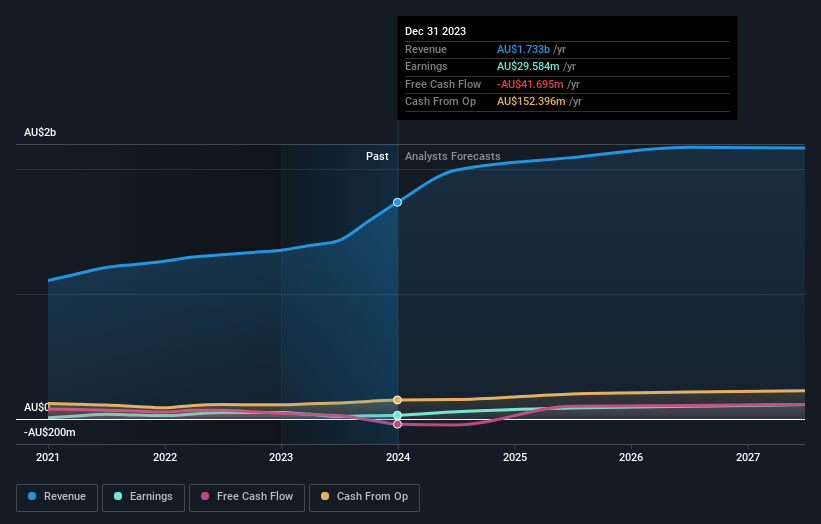

Kelsian Group (ASX:KLS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kelsian Group Limited (ASX:KLS) operates land and marine transport and tourism services in Australia, the United States, Singapore, and the United Kingdom, with a market cap of A$1.35 billion.

Operations: The company's revenue segments include Australian Bus at A$934.76 million, International Bus at A$448.87 million, and Marine and Tourism at A$337.90 million.

Insider Ownership: 20.9%

Earnings Growth Forecast: 25.5% p.a.

Kelsian Group's revenue is forecast to grow at 5.6% per year, slightly above the Australian market average of 5.3%. Analysts predict a 40.5% rise in stock price, but profit margins have declined from 3.8% to 1.7%. Earnings are expected to grow significantly at 25.53% annually, outpacing the market's growth rate of 13.6%. Insider buying has occurred recently, although not in substantial volumes, and the company trades at nearly 30% below its estimated fair value.

- Click here to discover the nuances of Kelsian Group with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Kelsian Group is priced lower than what may be justified by its financials.

Turning Ideas Into Actions

- Dive into all 91 of the Fast Growing ASX Companies With High Insider Ownership we have identified here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:C79

Chrysos

Engages in the development and supply of mining technology.