Stock Analysis

- New Zealand

- /

- Hospitality

- /

- NZSE:SVR

Does Savor (NZSE:SVR) Have A Healthy Balance Sheet?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Savor Limited (NZSE:SVR) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Savor

How Much Debt Does Savor Carry?

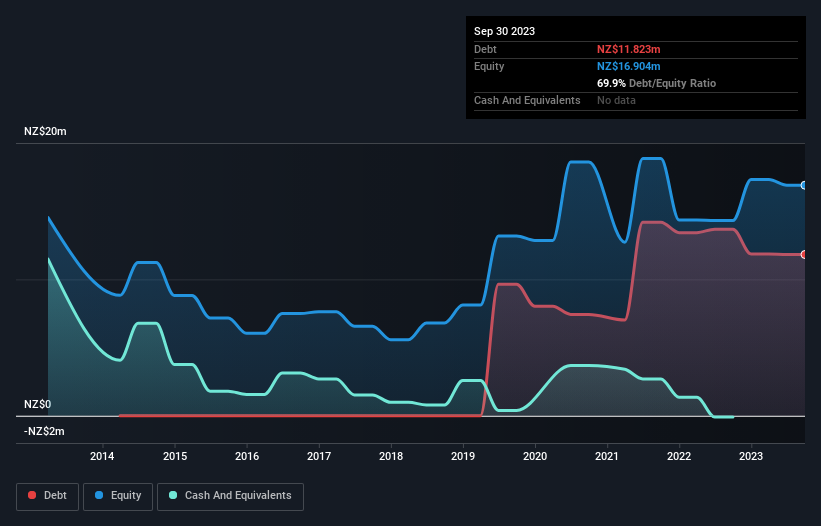

You can click the graphic below for the historical numbers, but it shows that Savor had NZ$11.8m of debt in September 2023, down from NZ$13.7m, one year before. And it doesn't have much cash, so its net debt is about the same.

A Look At Savor's Liabilities

The latest balance sheet data shows that Savor had liabilities of NZ$19.8m due within a year, and liabilities of NZ$20.0m falling due after that. Offsetting this, it had -NZ$94.0k in cash and NZ$991.0k in receivables that were due within 12 months. So it has liabilities totalling NZ$38.9m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the NZ$20.2m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Savor would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Savor's net debt is sitting at a very reasonable 1.8 times its EBITDA, while its EBIT covered its interest expense just 3.0 times last year. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. Pleasingly, Savor is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 1,422% gain in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Savor will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, Savor produced sturdy free cash flow equating to 70% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Neither Savor's ability to handle its total liabilities nor its interest cover gave us confidence in its ability to take on more debt. But the good news is it seems to be able to grow its EBIT with ease. Taking the abovementioned factors together we do think Savor's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 4 warning signs we've spotted with Savor (including 2 which are potentially serious) .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're helping make it simple.

Find out whether Savor is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:SVR

Savor

Savor Limited operates in the hospitality sector with 20 venues in Auckland.

Good value with imperfect balance sheet.