Stock Analysis

- France

- /

- Healthcare Services

- /

- ENXTPA:BLC

Benign Growth For Bastide Le Confort Médical SA (EPA:BLC) Underpins Stock's 26% Plummet

Unfortunately for some shareholders, the Bastide Le Confort Médical SA (EPA:BLC) share price has dived 26% in the last thirty days, prolonging recent pain. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 51% loss during that time.

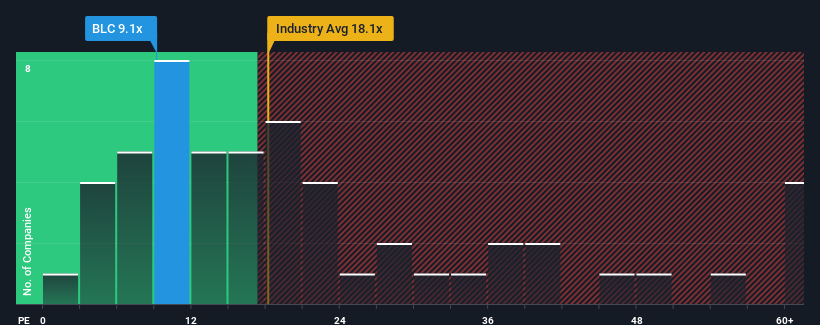

In spite of the heavy fall in price, Bastide Le Confort Médical may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 9.1x, since almost half of all companies in France have P/E ratios greater than 16x and even P/E's higher than 27x are not unusual. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Earnings have risen firmly for Bastide Le Confort Médical recently, which is pleasing to see. One possibility is that the P/E is low because investors think this respectable earnings growth might actually underperform the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Bastide Le Confort Médical

How Is Bastide Le Confort Médical's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as low as Bastide Le Confort Médical's is when the company's growth is on track to lag the market.

If we review the last year of earnings growth, the company posted a worthy increase of 9.7%. Although, the latest three year period in total hasn't been as good as it didn't manage to provide any growth at all. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 15% shows it's noticeably less attractive on an annualised basis.

In light of this, it's understandable that Bastide Le Confort Médical's P/E sits below the majority of other companies. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

The Bottom Line On Bastide Le Confort Médical's P/E

The softening of Bastide Le Confort Médical's shares means its P/E is now sitting at a pretty low level. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Bastide Le Confort Médical revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. If recent medium-term earnings trends continue, it's hard to see the share price rising strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Bastide Le Confort Médical (1 is significant) you should be aware of.

You might be able to find a better investment than Bastide Le Confort Médical. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're helping make it simple.

Find out whether Bastide Le Confort Médical is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:BLC

Bastide Le Confort Médical

Bastide Le Confort Médical SA engages in the sale and rental of medical equipment for individuals and health professionals in France and internationally.

Good value with moderate growth potential.