Stock Analysis

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Advance Synergy Berhad (KLSE:ASB) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Advance Synergy Berhad

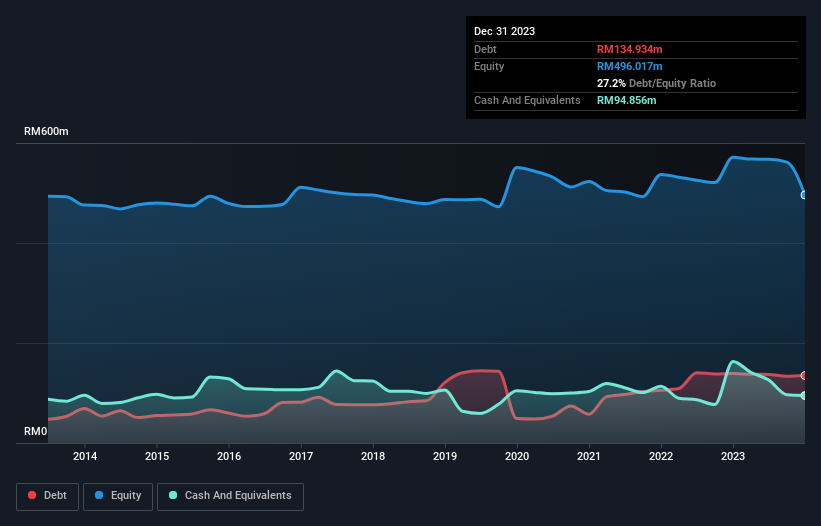

What Is Advance Synergy Berhad's Net Debt?

As you can see below, Advance Synergy Berhad had RM134.9m of debt, at December 2023, which is about the same as the year before. You can click the chart for greater detail. However, it also had RM94.9m in cash, and so its net debt is RM40.1m.

How Healthy Is Advance Synergy Berhad's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Advance Synergy Berhad had liabilities of RM135.4m due within 12 months and liabilities of RM123.3m due beyond that. On the other hand, it had cash of RM94.9m and RM164.3m worth of receivables due within a year. So these liquid assets roughly match the total liabilities.

This state of affairs indicates that Advance Synergy Berhad's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the RM265.6m company is short on cash, but still worth keeping an eye on the balance sheet. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Advance Synergy Berhad will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Advance Synergy Berhad reported revenue of RM288m, which is a gain of 18%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, Advance Synergy Berhad had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping RM65m. On a more positive note, the company does have liquid assets, so it has a bit of time to improve its operations before the debt becomes an acute problem. Still, we'd be more encouraged to study the business in depth if it already had some free cash flow. So it seems too risky for our taste. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 3 warning signs for Advance Synergy Berhad (2 shouldn't be ignored!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're helping make it simple.

Find out whether Advance Synergy Berhad is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:ASB

Advance Synergy Berhad

Advance Synergy Berhad, an investment holding company, operates in the property development and investment services in Malaysia.

Excellent balance sheet and overvalued.