Stock Analysis

- Poland

- /

- Consumer Durables

- /

- WSE:WIK

Wikana S.A. (WSE:WIK) Shares Fly 31% But Investors Aren't Buying For Growth

The Wikana S.A. (WSE:WIK) share price has done very well over the last month, posting an excellent gain of 31%. The last month tops off a massive increase of 109% in the last year.

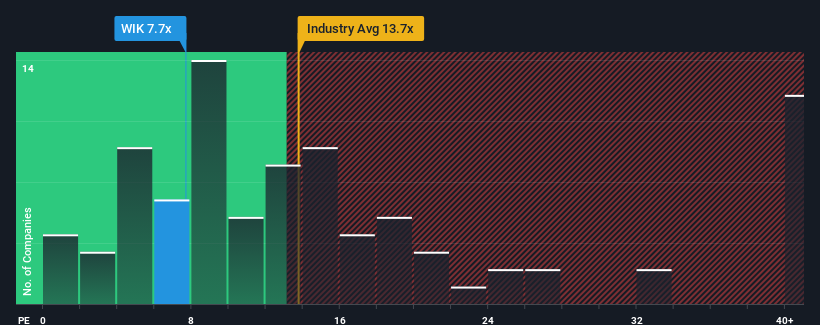

Even after such a large jump in price, Wikana may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 7.7x, since almost half of all companies in Poland have P/E ratios greater than 13x and even P/E's higher than 28x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Recent times have been quite advantageous for Wikana as its earnings have been rising very briskly. One possibility is that the P/E is low because investors think this strong earnings growth might actually underperform the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Wikana

How Is Wikana's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as low as Wikana's is when the company's growth is on track to lag the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 68% last year. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Comparing that to the market, which is predicted to deliver 6.4% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

With this information, we can see why Wikana is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Final Word

Despite Wikana's shares building up a head of steam, its P/E still lags most other companies. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Wikana revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. If recent medium-term earnings trends continue, it's hard to see the share price rising strongly in the near future under these circumstances.

There are also other vital risk factors to consider before investing and we've discovered 3 warning signs for Wikana that you should be aware of.

You might be able to find a better investment than Wikana. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're helping make it simple.

Find out whether Wikana is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:WIK

Wikana

Wikana S.A. engages in the real estate development business in Poland.

Flawless balance sheet with solid track record.