Stock Analysis

The market shrugged off Synthaverse S.A.'s (WSE:SVE) weak earnings report. Despite the market responding positively, we think that there are several concerning factors that investors should be aware of.

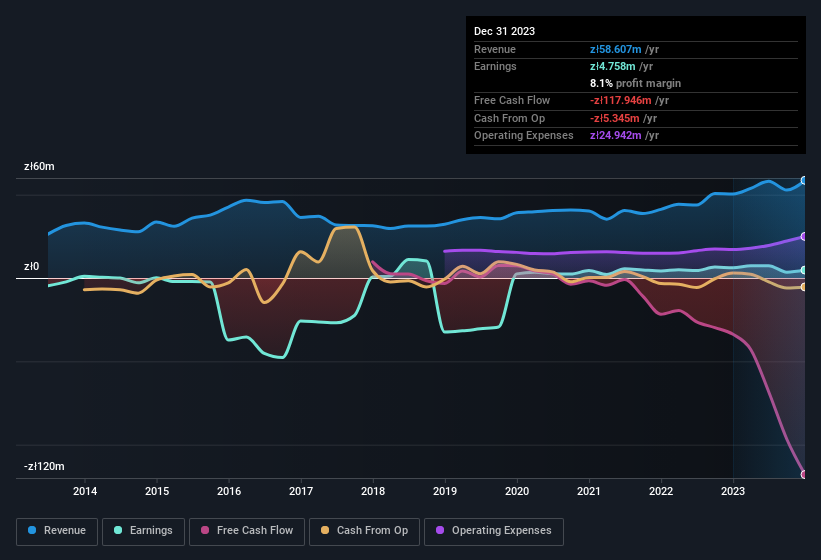

See our latest analysis for Synthaverse

Zooming In On Synthaverse's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

For the year to December 2023, Synthaverse had an accrual ratio of 0.91. Statistically speaking, that's a real negative for future earnings. And indeed, during the period the company didn't produce any free cash flow whatsoever. In the last twelve months it actually had negative free cash flow, with an outflow of zł118m despite its profit of zł4.76m, mentioned above. Coming off the back of negative free cash flow last year, we imagine some shareholders might wonder if its cash burn of zł118m, this year, indicates high risk. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Synthaverse.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. As it happens, Synthaverse issued 8.1% more new shares over the last year. That means its earnings are split among a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Synthaverse's historical EPS growth by clicking on this link.

A Look At The Impact Of Synthaverse's Dilution On Its Earnings Per Share (EPS)

As you can see above, Synthaverse has been growing its net income over the last few years, with an annualized gain of 7.2% over three years. In contrast, earnings per share were actually down by 1.8% per year, in the exact same period. Net income was down 22% over the last twelve months. But the EPS result was even worse, with the company recording a decline of 25%. Therefore, the dilution is having a noteworthy influence on shareholder returns.

In the long term, if Synthaverse's earnings per share can increase, then the share price should too. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On Synthaverse's Profit Performance

In conclusion, Synthaverse has weak cashflow relative to earnings, which indicates lower quality earnings, and the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). For the reasons mentioned above, we think that a perfunctory glance at Synthaverse's statutory profits might make it look better than it really is on an underlying level. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. Be aware that Synthaverse is showing 5 warning signs in our investment analysis and 2 of those are a bit concerning...

Our examination of Synthaverse has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Valuation is complex, but we're helping make it simple.

Find out whether Synthaverse is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About WSE:SVE

Synthaverse

Synthaverse S.A., a pharmaceutical company, manufactures and sells medicinal products, medical devices, and laboratory reagents in Poland.

Imperfect balance sheet with poor track record.