Stock Analysis

- Hong Kong

- /

- Basic Materials

- /

- SEHK:2233

West China Cement (HKG:2233) Will Pay A Smaller Dividend Than Last Year

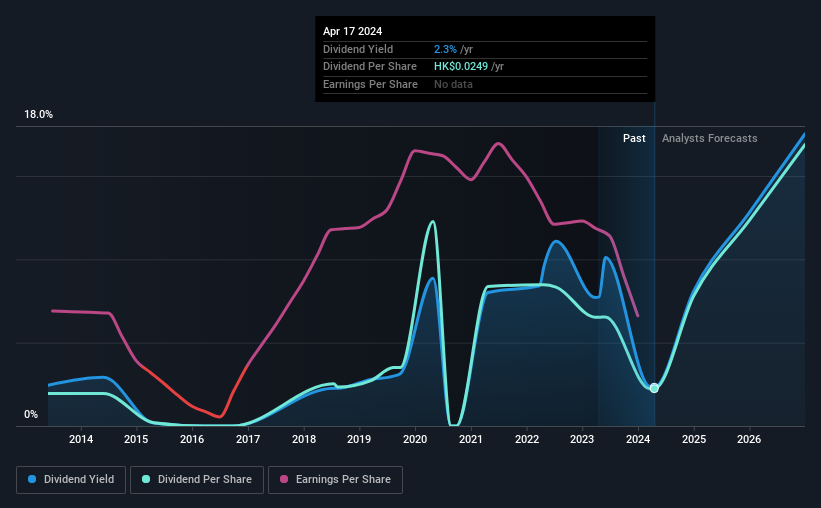

West China Cement Limited (HKG:2233) has announced that on 31st of July, it will be paying a dividend ofCN¥0.023, which a reduction from last year's comparable dividend. This payment takes the dividend yield to 2.3%, which only provides a modest boost to overall returns.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that West China Cement's stock price has increased by 78% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

View our latest analysis for West China Cement

West China Cement's Payment Has Solid Earnings Coverage

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. However, West China Cement's earnings easily cover the dividend. This means that most of what the business earns is being used to help it grow.

Analysts expect a massive rise in earnings per share in the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 5.1%, so there isn't too much pressure on the dividend.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The annual payment during the last 10 years was CN¥0.02 in 2014, and the most recent fiscal year payment was CN¥0.023. This works out to be a compound annual growth rate (CAGR) of approximately 1.4% a year over that time. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. West China Cement's EPS has fallen by approximately 18% per year during the past five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

In Summary

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've identified 4 warning signs for West China Cement (1 is potentially serious!) that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're helping make it simple.

Find out whether West China Cement is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About SEHK:2233

West China Cement

West China Cement Limited, an investment holding company, manufactures and sells cement and cement products in the People’s Republic of China.

Good value with reasonable growth potential.