Stock Analysis

- Poland

- /

- Consumer Durables

- /

- WSE:1AT

We Think That There Are More Issues For Atal (WSE:1AT) Than Just Sluggish Earnings

Despite Atal S.A.'s (WSE:1AT) recent earnings report having lackluster headline numbers, the market responded positively. Sometimes, shareholders are willing to ignore soft numbers with the hope that they will improve, but our analysis suggests this is unlikely for Atal.

Check out our latest analysis for Atal

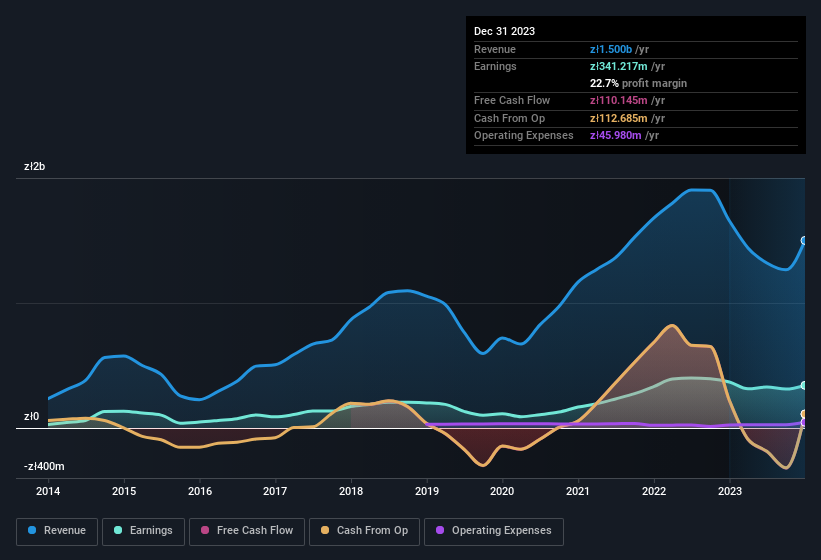

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, Atal increased the number of shares on issue by 12% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Atal's historical EPS growth by clicking on this link.

A Look At The Impact Of Atal's Dilution On Its Earnings Per Share (EPS)

As you can see above, Atal has been growing its net income over the last few years, with an annualized gain of 104% over three years. Net profit actually dropped by 7.3% in the last year. Unfortunately for shareholders, though, the earnings per share result was even worse, declining 11%. And so, you can see quite clearly that dilution is influencing shareholder earnings.

If Atal's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Atal's Profit Performance

Over the last year Atal issued new shares and so, there's a noteworthy divergence between EPS and net income growth. Therefore, it seems possible to us that Atal's true underlying earnings power is actually less than its statutory profit. But the good news is that its EPS growth over the last three years has been very impressive. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. You'd be interested to know, that we found 2 warning signs for Atal and you'll want to know about them.

Today we've zoomed in on a single data point to better understand the nature of Atal's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Valuation is complex, but we're helping make it simple.

Find out whether Atal is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:1AT

Atal

Atal S.A. engages in the development and sale of residential buildings in Poland.

Excellent balance sheet and good value.