Stock Analysis

- Belgium

- /

- Metals and Mining

- /

- ENXTBR:VIO

Viohalco (EBR:VIO) Has No Shortage Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Viohalco S.A. (EBR:VIO) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Viohalco

What Is Viohalco's Net Debt?

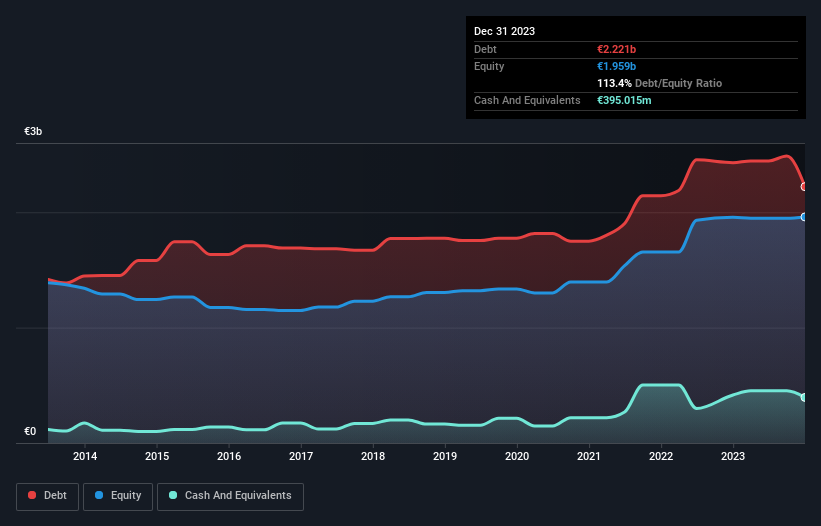

As you can see below, Viohalco had €2.22b of debt at December 2023, down from €2.43b a year prior. However, it also had €395.0m in cash, and so its net debt is €1.83b.

How Strong Is Viohalco's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Viohalco had liabilities of €2.30b due within 12 months and liabilities of €1.66b due beyond that. On the other hand, it had cash of €395.0m and €969.8m worth of receivables due within a year. So it has liabilities totalling €2.60b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the €1.32b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, Viohalco would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Viohalco's debt to EBITDA ratio (4.2) suggests that it uses some debt, its interest cover is very weak, at 1.5, suggesting high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Even worse, Viohalco saw its EBIT tank 44% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Viohalco's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Viohalco saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

On the face of it, Viohalco's EBIT growth rate left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. And furthermore, its interest cover also fails to instill confidence. It looks to us like Viohalco carries a significant balance sheet burden. If you harvest honey without a bee suit, you risk getting stung, so we'd probably stay away from this particular stock. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Viohalco you should be aware of, and 1 of them doesn't sit too well with us.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're helping make it simple.

Find out whether Viohalco is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About ENXTBR:VIO

Viohalco

Viohalco S.A., through its subsidiaries, manufactures, and sells aluminium, copper, cables, and steel and steel pipe products worldwide.

Adequate balance sheet second-rate dividend payer.