Stock Analysis

Vertiseit AB (publ) (STO:VERT B) just reported some strong earnings, and the market reacted accordingly with a healthy uplift in the share price. We did some analysis and think that investors are missing some details hidden beneath the profit numbers.

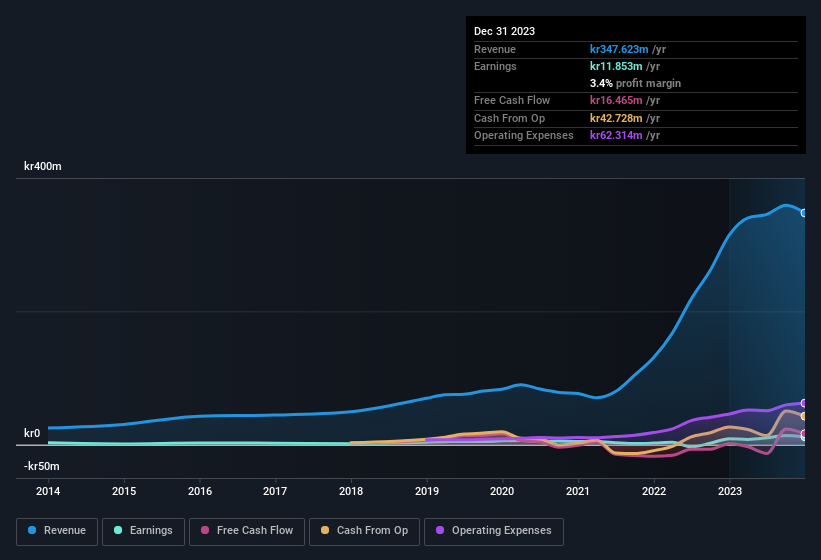

See our latest analysis for Vertiseit

The Impact Of Unusual Items On Profit

Importantly, our data indicates that Vertiseit's profit received a boost of kr5.4m in unusual items, over the last year. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And, after all, that's exactly what the accounting terminology implies. If Vertiseit doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Vertiseit's Profit Performance

We'd posit that Vertiseit's statutory earnings aren't a clean read on ongoing productivity, due to the large unusual item. Because of this, we think that it may be that Vertiseit's statutory profits are better than its underlying earnings power. But at least holders can take some solace from the 60% per annum growth in EPS for the last three. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. To help with this, we've discovered 3 warning signs (1 is concerning!) that you ought to be aware of before buying any shares in Vertiseit.

This note has only looked at a single factor that sheds light on the nature of Vertiseit's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Valuation is complex, but we're helping make it simple.

Find out whether Vertiseit is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Simply Wall St

About OM:VERT B

Vertiseit

Vertiseit AB (publ), a retail tech company, operates digital in-store platform in Sweden.

Excellent balance sheet with reasonable growth potential.