Stock Analysis

These 4 Measures Indicate That Andritz (VIE:ANDR) Is Using Debt Safely

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Andritz AG (VIE:ANDR) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Andritz

How Much Debt Does Andritz Carry?

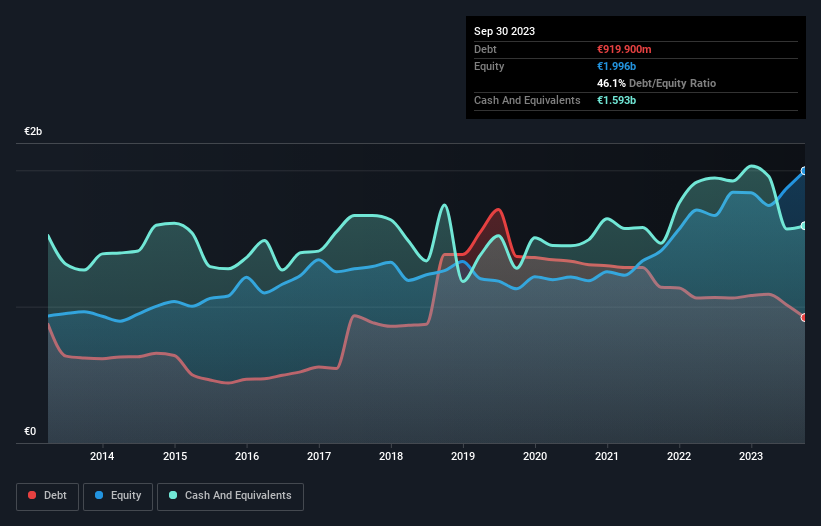

You can click the graphic below for the historical numbers, but it shows that Andritz had €919.9m of debt in September 2023, down from €1.06b, one year before. However, it does have €1.59b in cash offsetting this, leading to net cash of €673.4m.

A Look At Andritz's Liabilities

According to the last reported balance sheet, Andritz had liabilities of €5.06b due within 12 months, and liabilities of €1.35b due beyond 12 months. Offsetting these obligations, it had cash of €1.59b as well as receivables valued at €2.73b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by €2.09b.

Andritz has a market capitalization of €5.69b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, Andritz also has more cash than debt, so we're pretty confident it can manage its debt safely.

On top of that, Andritz grew its EBIT by 36% over the last twelve months, and that growth will make it easier to handle its debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Andritz's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Andritz has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, Andritz recorded free cash flow worth 74% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

While Andritz does have more liabilities than liquid assets, it also has net cash of €673.4m. And it impressed us with its EBIT growth of 36% over the last year. So is Andritz's debt a risk? It doesn't seem so to us. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for Andritz (1 makes us a bit uncomfortable) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're helping make it simple.

Find out whether Andritz is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WBAG:ANDR

Andritz

Andritz AG provides plants, equipment, and services for pulp and paper industry, metalworking and steel industries, hydropower stations, and solid/liquid separation in the municipal and industrial sectors in Europe, North America, South America, China, Asia, and internationally.

Very undervalued with flawless balance sheet and pays a dividend.